Last Update17 Sep 25Fair value Decreased 0.63%

Despite long-term optimism driven by Diamondback Energy's strategic positioning in the evolving energy sector and robust operational execution, analysts have made a slight downward revision to the consensus price target—from $182.00 to $180.86—due to short-term overhangs from significant share registration events.

Analyst Commentary

- Bullish analysts cite the accelerating impact of AI adoption, describing an early-stage "Power revolution" shifting energy sector leadership to new winners, including Diamondback Energy.

- Price target increases from major institutions reflect updated valuations for U.S. Integrated Oil, Refining, and large cap E&Ps, with Diamondback Energy benefiting from sector-wide re-ratings.

- Incremental upward price target revisions suggest continued confidence in Diamondback's operational execution and exposure to structurally favorable energy market conditions.

- Near-term overhangs exist due to significant share registration events linked to affiliated entities, which may cause temporary negative stock reactions versus peers.

- Structural positioning in the evolving energy landscape and broader industry optimism underpin analysts' positive long-term outlooks for Diamondback shares.

What's in the News

- The owners of the EPIC Crude pipeline, including Diamondback Energy, are exploring a sale of the pipeline, potentially valuing the asset at approximately $3B including debt; Diamondback Energy holds an equal stake with Kinetik and Ares Management controls 45% (Reuters).

- Diamondback Energy revised its Q3 2025 production guidance upward to 494–504 MBO/d for oil (previously 485–495 MBO/d) and net production guidance to 908–938 MBOE/d (previously 890–920 MBOE/d).

- The company reported significant year-over-year production growth in Q2 2025: oil production increased to 45,108 MBbls (from 25,129 MBbls), natural gas to 110,119 MMcf (from 51,310 MMcf), and natural gas liquids to 20,248 MBbls (from 9,514 MBbls); daily combined volumes nearly doubled.

- Diamondback completed repurchase of 4.66 million shares (1.62%) for $636 million in the most recent tranche, totaling 32.9 million shares (16.15%) and $4.1 billion under the buyback since September 2021.

- The company increased its buyback authorization by $2 billion to a total of $8 billion and narrowed its full-year 2025 oil production guidance to 485–492 MBO/d, with annual BOE guidance raised by 2% to 890–910 MBOE/d.

Valuation Changes

Summary of Valuation Changes for Diamondback Energy

- The Consensus Analyst Price Target remained effectively unchanged, moving only marginally from $182.00 to $180.86.

- The Consensus Revenue Growth forecasts for Diamondback Energy has significantly risen from 5.2% per annum to 8.5% per annum.

- The Net Profit Margin for Diamondback Energy has fallen from 28.53% to 26.90%.

Key Takeaways

- Successful Permian Basin consolidation and operational efficiency drive sustainable cost reductions, higher margins, and resilient cash flow amid oil market volatility.

- Strategic asset sales and disciplined capital allocation strengthen the balance sheet, reduce risk, and set the stage for enhanced shareholder returns and production growth.

- Rising operating costs, lower quality drilling inventory, oil price volatility, diminishing efficiency gains, and limited quality acquisitions threaten long-term profitability and revenue growth.

Catalysts

About Diamondback Energy- An independent oil and natural gas company, acquires, develops, explores, and exploits unconventional, onshore oil and natural gas reserves in the Permian Basin in West Texas.

- Ongoing consolidation in the Permian Basin, with Diamondback positioned as the "consolidator of choice" due to its industry-best integration, low cost structure, and ability to deliver synergies from recent large acquisitions (e.g., Double Eagle, Endeavor), supports future growth in scale, cost savings, and higher EBITDA margins.

- Consistent operational efficiency improvements (record drilling times, workover programs, optimization of older wells, and improved gas capture) point to sustainable cost reductions and productivity enhancements, supporting resilient net margins and robust free cash flow even in a volatile oil price environment.

- Anticipated noncore asset sales (targeting $1.5 billion), debt paydown, and enhanced balance sheet flexibility will lower interest expenses, reduce financial risk, and ultimately enable increased shareholder returns via buybacks/dividends, directly impacting future EPS and total returns.

- The company's ability to exploit emerging zones within its existing acreage (such as Wolfcamp B/D and others) without performance degradation, combined with the long-term, favorable trend of underinvestment and growing global oil demand, supports stable or growing production volumes and revenue over the next several years.

- Diamondback's focus on domestic energy security and operational discipline aligns with growing policy support and infrastructure investment, helping maintain or expand market share, and positioning the company to benefit disproportionately from secular demand for reliable U.S. oil supply-positively impacting long-term revenue and earnings resilience.

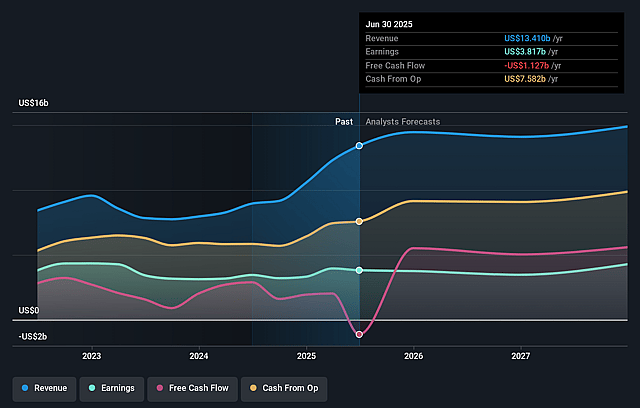

Diamondback Energy Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Diamondback Energy's revenue will grow by 5.2% annually over the next 3 years.

- Analysts are assuming Diamondback Energy's profit margins will remain the same at 28.5% over the next 3 years.

- Analysts expect earnings to reach $4.5 billion (and earnings per share of $16.47) by about September 2028, up from $3.8 billion today. However, there is a considerable amount of disagreement amongst the analysts with the most bullish expecting $5.8 billion in earnings, and the most bearish expecting $2.9 billion.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 14.3x on those 2028 earnings, up from 10.3x today. This future PE is greater than the current PE for the US Oil and Gas industry at 12.6x.

- Analysts expect the number of shares outstanding to decline by 0.86% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 7.44%, as per the Simply Wall St company report.

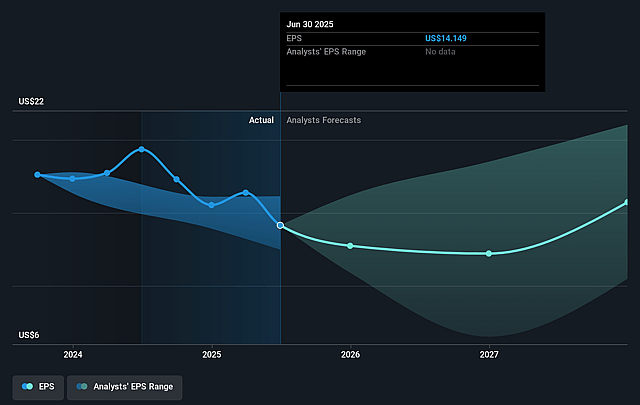

Diamondback Energy Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- Increasing water management and disposal costs, coupled with electricity and power inflation in the Permian Basin, could significantly raise Diamondback's long-term operating expenses (LOE), thereby pressuring net margins and EBITDA.

- The company's development mix is increasingly shifting toward secondary and non-core zones as top-tier acreage becomes scarcer, risking declining well productivity and higher per-barrel costs in the future, which may erode long-term earnings resilience.

- Persistent uncertainty around oil price volatility and macroeconomic headwinds-combined with significant exposure to commodity price swings due to a less robust hedge position for 2026 and beyond-could impair future revenues, free cash flow, and the sustainability of shareholder returns if prices fall.

- Industry-wide efficiency gains and cost reductions are showing signs of plateauing, while supply chain risks (such as casing tariffs and steel cost inflation) could limit further margin improvements, challenging Diamondback's ability to maintain its cost leadership and robust capital efficiency over the long term.

- Limited inventory of high-quality, accretive acquisition targets in the Permian and growing competition among consolidators heighten the risk that future M&A will be either value-dilutive or unattainable, leading to slower production growth, less scale advantage, and increased reliance on organic opportunities which may yield lower returns and impact long-term revenue growth.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $182.0 for Diamondback Energy based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $222.0, and the most bearish reporting a price target of just $143.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be $15.6 billion, earnings will come to $4.5 billion, and it would be trading on a PE ratio of 14.3x, assuming you use a discount rate of 7.4%.

- Given the current share price of $136.29, the analyst price target of $182.0 is 25.1% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.