Last Update 30 Apr 25

Fair value Decreased 1.69%Key Takeaways

- Strategic acquisitions and lower breakeven costs improve revenue growth while enhancing free cash flow and earnings.

- Share repurchases indicate management's confidence in increasing shareholder value and superior future earnings.

- Heavy reliance on scale efficiencies and share repurchases may limit growth, while capital and operational challenges could impact margins and earnings.

Catalysts

About Diamondback Energy- An independent oil and natural gas company, acquires, develops, explores, and exploits unconventional, onshore oil and natural gas reserves in the Permian Basin in West Texas.

- Diamondback Energy's ability to maintain capital efficiency by lowering its breakeven oil price to $67 per barrel from last year's $76 is expected to enhance its free cash flow generation, positively influencing the company's earnings.

- The ongoing drawdown of drilled but uncompleted wells and increasing efficiencies in their SimulFRAC operations are anticipated to lead to reduced future capital expenditure requirements, thereby improving net margins.

- The company's strategic acquisition and integration of quality assets and inventory from Endeavor and Double Eagle are likely expected to boost production operationally without excessive additional costs, positively impacting revenue growth prospects.

- The push towards share repurchases, due to perceived undervaluation of the stock and a supportive shareholder base, including the Stephens family, suggests management confidence in superior future earnings and shareholder value.

- Though capital tied up in midstream infrastructure investment is set to reduce with potential sales and integration into joint ventures like Deep Blue, it creates an opportunity for lowering future operational expenses, thereby enhancing net profit margins.

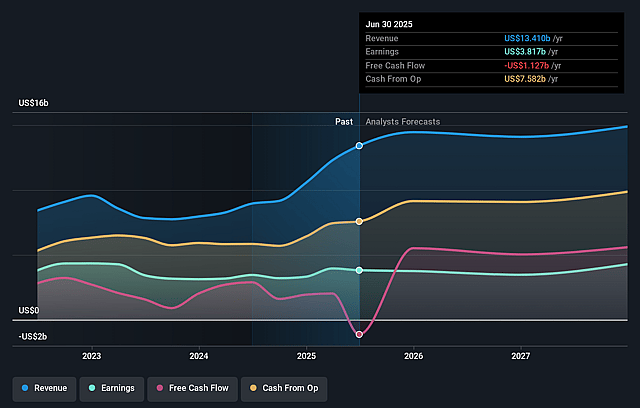

Diamondback Energy Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- This narrative explores a more pessimistic perspective on Diamondback Energy compared to the consensus, based on a Fair Value that aligns with the bearish cohort of analysts.

- The bearish analysts are assuming Diamondback Energy's revenue will grow by 4.0% annually over the next 3 years.

- The bearish analysts assume that profit margins will shrink from 31.4% today to 19.1% in 3 years time.

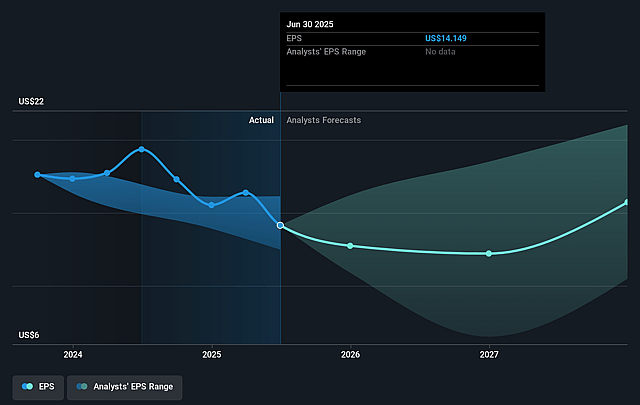

- The bearish analysts expect earnings to reach $2.3 billion (and earnings per share of $7.94) by about April 2028, down from $3.3 billion today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the price target of the more bearish analyst cohort, the company would need to trade at a PE ratio of 32.0x on those 2028 earnings, up from 11.6x today. This future PE is greater than the current PE for the US Oil and Gas industry at 11.8x.

- Analysts expect the number of shares outstanding to grow by 7.0% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 7.11%, as per the Simply Wall St company report.

Diamondback Energy Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The company is heavily reliant on achieving economies of scale through acquisitions and efficiencies, making it challenging to continually reduce free cash flow breakeven points, which can impact net margins if these efficiencies cannot be sustained or replicated.

- There is a significant emphasis on share repurchases as a use of capital, suggesting a limited scope for further M&A growth which could potentially restrict future revenue growth opportunities if market conditions or share prices do not support buybacks at anticipated levels.

- Concerns around capital spending efficiency are raised with regard to maintaining high levels of well productivity while managing DUC drawdowns and balancing the CapEx input relative to the free cash flow output, directly affecting earnings if efficiencies are not optimized.

- The substantial $1.5 billion commitment on asset sales to reduce net debt could possibly pressure immediate financial flexibility and impact overall enterprise value if those assets do not sell for expected values or in the anticipated timeframe, thereby affecting earnings.

- There is exposure to potential volatility in power supply and related costs in the Permian basin, with ongoing investments to secure electrical needs; this could increase operating expenses and thus, affect net margins if power scarcity persists or costs are underestimated.

Valuation

How have all the factors above been brought together to estimate a fair value?- The assumed bearish price target for Diamondback Energy is $164.7, which represents one standard deviation below the consensus price target of $186.36. This valuation is based on what can be assumed as the expectations of Diamondback Energy's future earnings growth, profit margins and other risk factors from analysts on the more bearish end of the spectrum.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $234.0, and the most bearish reporting a price target of just $145.0.

- In order for you to agree with the bearish analysts, you'd need to believe that by 2028, revenues will be $11.9 billion, earnings will come to $2.3 billion, and it would be trading on a PE ratio of 32.0x, assuming you use a discount rate of 7.1%.

- Given the current share price of $131.98, the bearish analyst price target of $164.7 is 19.9% higher. Despite analysts expecting the underlying buisness to decline, they seem to believe it's more valuable than what the market thinks.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Diamondback Energy?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystLowTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystLowTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystLowTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.