Narratives are currently in beta

Key Takeaways

- High-quality portfolio and higher interest rates boost investment income, suggesting potential revenue and earnings growth.

- Long-term housing demand and strategic reinsurance enhance capital efficiency, indicating strong future mortgage insurance revenue growth.

- Higher mortgage rates and macroeconomic uncertainties could reduce revenues, while natural disasters and aging portfolios may increase defaults, impacting net margins and earnings.

Catalysts

About Essent Group- Through its subsidiaries, provides private mortgage insurance and reinsurance for mortgages secured by residential properties located in the United States.

- Essent Group is benefiting from a high-quality portfolio and higher interest rates, which improve persistency and investment income, suggesting potential for increased future revenues and earnings.

- The constructive long-term outlook for housing, supported by supply/demand imbalances and favorable demographic trends, indicates potential growth in revenue from mortgage insurance in force.

- The execution of the 10th Radnor Re ILN transaction and commitment to a programmatic reinsurance strategy may enhance capital efficiency and net margins by diversifying capital resources and seeding mezzanine credit risk.

- An increase in investment returns due to higher yields on a growing investment portfolio implies potential for higher future earnings.

- Continuous financial discipline and strategic growth opportunities, alongside capital management through buybacks and dividends, may improve earnings per share (EPS) over time.

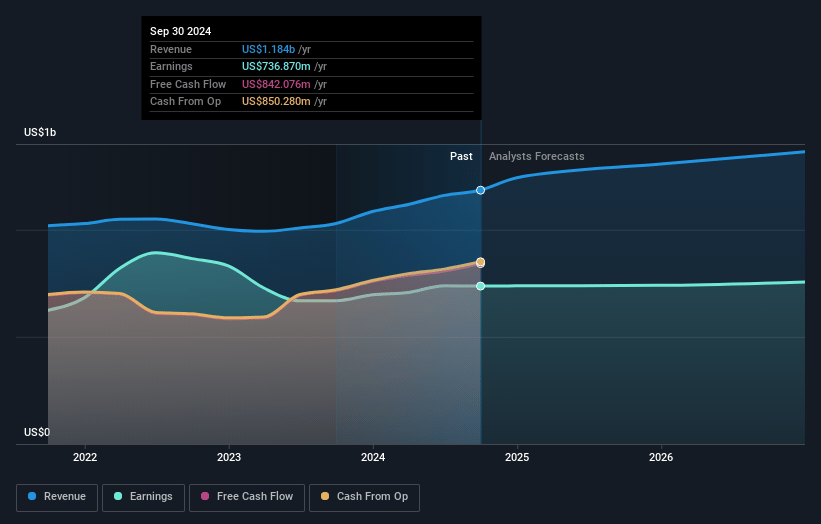

Essent Group Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Essent Group's revenue will grow by 6.4% annually over the next 3 years.

- Analysts assume that profit margins will shrink from 62.2% today to 53.3% in 3 years time.

- Analysts expect earnings to reach $760.9 million (and earnings per share of $7.54) by about January 2028, up from $736.9 million today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 10.2x on those 2028 earnings, up from 8.3x today. This future PE is lower than the current PE for the US Diversified Financial industry at 19.2x.

- Analysts expect the number of shares outstanding to decline by 1.67% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 6.84%, as per the Simply Wall St company report.

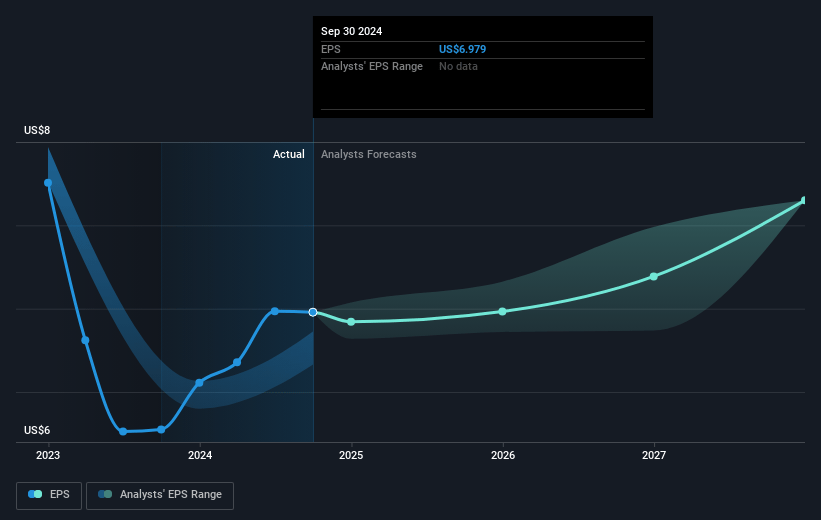

Essent Group Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- Higher mortgage and interest rates have led to reduced overall mortgage originations, potentially impacting future revenues and net margins.

- The impact of natural disasters, like Hurricanes Helene and Milton, might lead to an uptick in delinquencies, although insurance policy exclusions can partially mitigate financial effects, potentially impacting net earnings.

- The normalization of the default rate and potential increase in defaults due to the aging portfolio could raise provisioning costs, affecting net margins and earnings.

- Incremental revenues from investments might face limitations as the investment environment changes, impacting future earnings growth.

- Uncertainty regarding the trajectory of the housing market and macroeconomic conditions, such as labor market changes, could affect credit quality and subsequently impact revenue and profit margins.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $63.88 for Essent Group based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $72.0, and the most bearish reporting a price target of just $58.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be $1.4 billion, earnings will come to $760.9 million, and it would be trading on a PE ratio of 10.2x, assuming you use a discount rate of 6.8%.

- Given the current share price of $57.53, the analyst's price target of $63.88 is 9.9% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Read more narratives

There are no other narratives for this company.

View all narratives