Narratives are currently in beta

Key Takeaways

- Enhanced product offerings targeting millennials and Gen-Z should drive revenue via high new account acquisitions and retention rates.

- Strong international market growth, especially in Japan and Mexico, is crucial for expanding Amex's geographical revenue base.

- Economic pressures, competitive dining space risks, and heavy reliance on affluent consumers pose challenges to American Express's revenue and growth prospects.

Catalysts

About American Express- Operates as integrated payments company in the United States, Europe, the Middle East and Africa, the Asia Pacific, Australia, New Zealand, Latin America, Canada, the Caribbean, and Internationally.

- American Express has been continuously refreshing and enhancing its products to attract millennials and Gen-Z customers, particularly with the Gold Card. This is expected to drive revenue growth through strong new account acquisitions and high retention rates, ultimately increasing net card fees and spending.

- The growing emphasis on dining, with investments in companies like Resy, Tock, and Rooam, should differentiate Amex's offerings and boost transaction volumes. This strategy is likely to enhance revenue by tapping into the $1 trillion U.S. dining market.

- International markets, particularly Japan and Mexico, are experiencing double-digit spend growth, which is expected to contribute significantly to overall revenue growth. Amex's strategy to deepen engagement with international customers is critical for expanding its geographical revenue base.

- The company is benefiting from its premium customer base, noted for stable spend growth and strong credit performance. This affinity for premium services should bolster both net interest income and fee-based revenue over time.

- American Express continues its share repurchase program, which helps drive EPS growth, allowing the company to return excess capital to shareholders even in the face of moderated revenue growth.

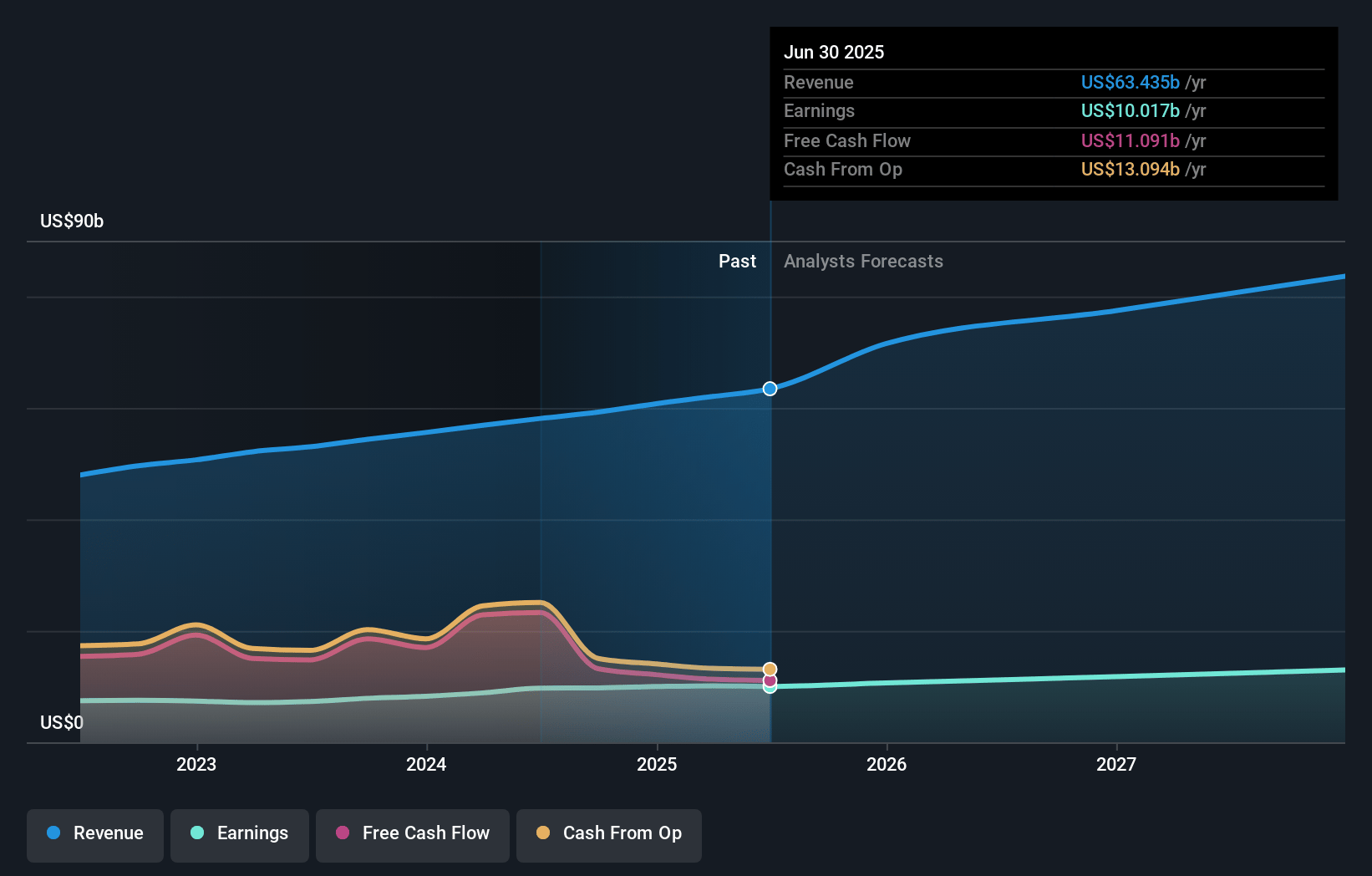

American Express Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming American Express's revenue will grow by 11.1% annually over the next 3 years.

- Analysts assume that profit margins will shrink from 16.5% today to 15.1% in 3 years time.

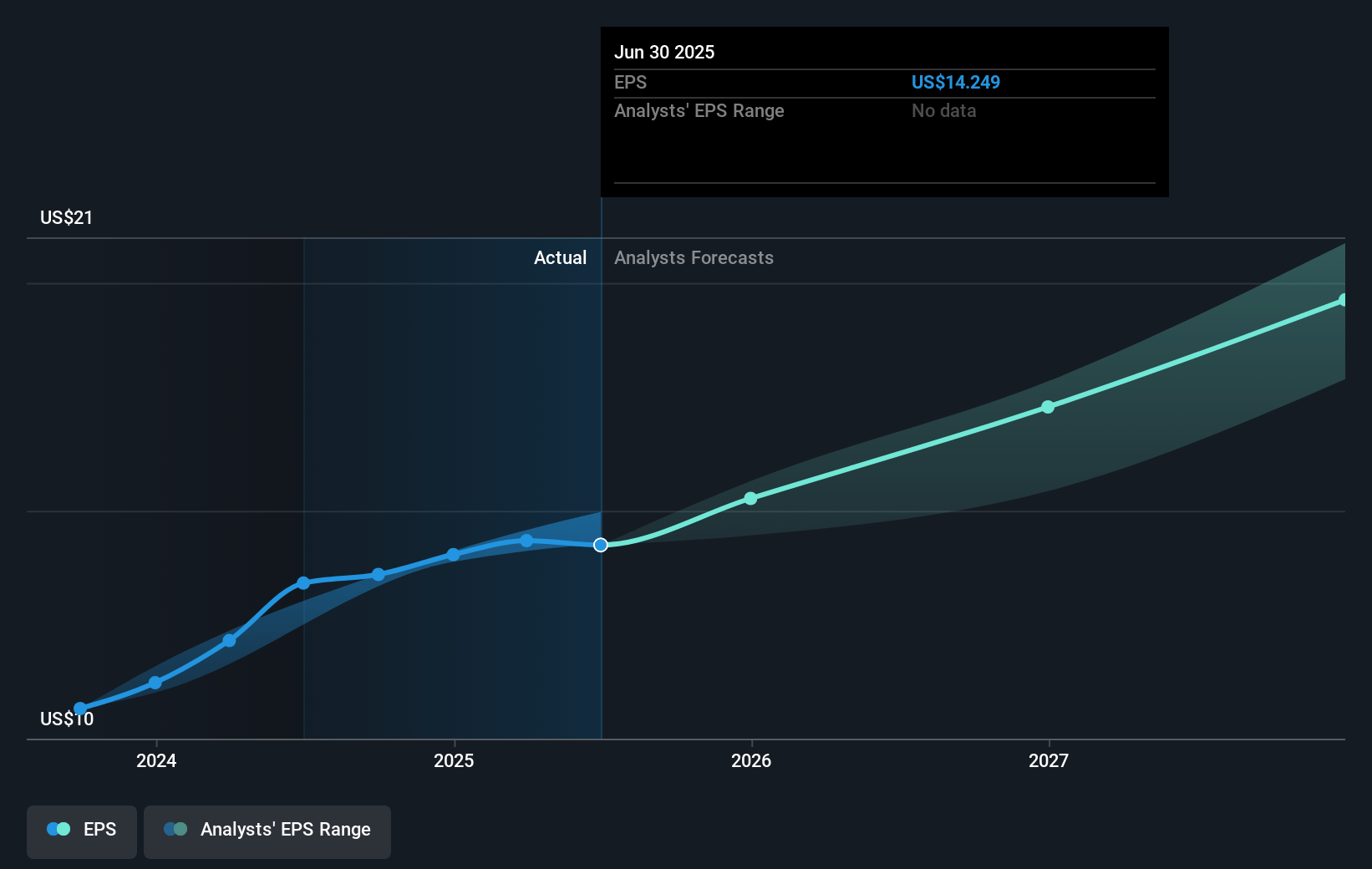

- Analysts expect earnings to reach $12.2 billion (and earnings per share of $17.68) by about December 2027, up from $9.8 billion today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 20.2x on those 2027 earnings, down from 21.9x today. This future PE is greater than the current PE for the US Consumer Finance industry at 11.5x.

- Analysts expect the number of shares outstanding to decline by 0.59% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 7.34%, as per the Simply Wall St company report.

American Express Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The softness in organic spend growth, especially in the small business sector, could indicate underlying economic pressures that might affect future revenue growth if the trend continues. This could lead to weaker billing and discount revenue overall.

- Competition in the dining space, despite Amex's initiatives, poses a risk. If competitors effectively capitalize on this market, it could impact American Express’s ability to grow and differentiate its membership model, which may affect revenue growth.

- Economic conditions, such as consumer confidence and spending behavior, particularly in a possible recessionary environment, can introduce uncertainty in billings growth. This could exert pressure on revenue and net margins if organic spend doesn't recover or if acquisition rates slow down.

- The company's heavy reliance on the affluent consumer market means economic or political instability, such as an election cycle, could impact this demographic's spending habits, potentially affecting billed business and revenue growth.

- The necessity for significant ongoing investments in marketing and technology implies that any reduction in the perceived return on these investments could lead to a re-evaluation of spending priorities, potentially impacting future earnings growth.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $288.44 for American Express based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $350.0, and the most bearish reporting a price target of just $230.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2027, revenues will be $81.2 billion, earnings will come to $12.2 billion, and it would be trading on a PE ratio of 20.2x, assuming you use a discount rate of 7.3%.

- Given the current share price of $303.46, the analyst's price target of $288.44 is 5.2% lower. The relatively low difference between the current share price and the analyst consensus price target indicates that they believe on average, the company is fairly priced.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Read more narratives

WA

WallStreetWontons

Community Contributor

AXP: Key Acquisitions and Enhanced Membership Models Sustains an Incredible Moat

Catalysts New Products or Services Impacting Sales or Earnings American Express has been actively enhancing its product offerings and making strategic acquisitions to drive sales and earnings growth. Here are some key points from recent earnings calls and reports: Product Innovations and Refreshes : American Express is on track to refresh approximately 40 products globally by the end of the year, including a refreshed US consumer gold card [source].

View narrativeUS$308.19

FV

1.5% undervalued intrinsic discount10.81%

Revenue growth p.a.

6users have liked this narrative

0users have commented on this narrative

3users have followed this narrative

3 months ago author updated this narrative