Key Takeaways

- Increased focus on alternatives and liquid strategies exposes the company to risks from market shifts, regulatory changes, and intense competition for quality affiliates.

- Ongoing migration toward low-cost passive investing and generational wealth transfer threaten client retention, fee sustainability, and profit margins.

- Accelerating growth in alternative investments, strong affiliate performance, and strategic capital allocation are strengthening AMG's earnings resilience, profitability, and long-term growth prospects.

Catalysts

About Affiliated Managers Group- Through its affiliates, operates as an investment management company providing investment management services to mutual funds, institutional clients,retails and high net worth individuals in the United States.

- Rapid growth in alternatives and liquid strategies may result in over-exposure to areas vulnerable to cycles of illiquidity, valuation resets, or regulatory change. Should investors rotate back to passive or index funds or if alternatives fall out of favor, AMG's revenue and organic growth rate could stagnate or sharply decline.

- As the industry continues its long-term migration toward low-cost passive investments and ETFs, AMG faces structural asset outflows from traditional active strategies. This could reduce overall AUM, fee revenue and erode net margins, especially if alternative inflows prove less sustainable than anticipated.

- Increasing reliance on higher-margin private market and liquid alternative products may attract greater regulatory scrutiny and associated compliance costs, which could compress profitability and offset expected operating leverage improvements.

- Generational wealth transfer to fee-conscious investors threatens client retention, as younger investors increasingly demand transparency and lower-cost index solutions rather than boutique active management. This shift could significantly weaken AMG's ability to sustain premium fee rates and future earnings per share.

- The fierce competition for high-performing alternative affiliates is likely to intensify, driving up acquisition costs, reducing the quality of future partnerships, and potentially resulting in a mix of underperforming affiliates. This would threaten both top-line revenue growth and the stability of EBITDA and economic EPS going forward.

Affiliated Managers Group Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- This narrative explores a more pessimistic perspective on Affiliated Managers Group compared to the consensus, based on a Fair Value that aligns with the bearish cohort of analysts.

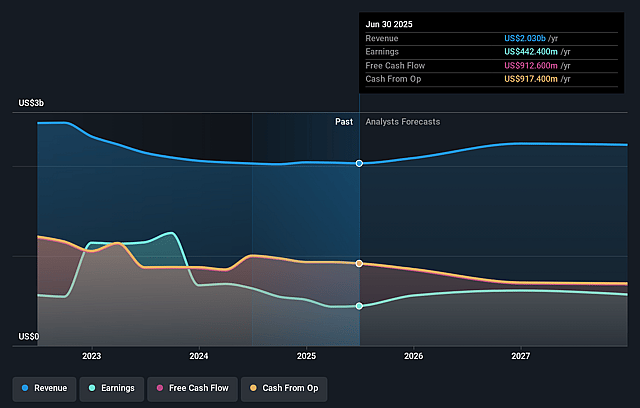

- The bearish analysts are assuming Affiliated Managers Group's revenue will grow by 1.7% annually over the next 3 years.

- The bearish analysts assume that profit margins will increase from 21.8% today to 27.8% in 3 years time.

- The bearish analysts expect earnings to reach $594.0 million (and earnings per share of $24.47) by about September 2028, up from $442.4 million today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the price target of the more bearish analyst cohort, the company would need to trade at a PE ratio of 9.8x on those 2028 earnings, down from 14.9x today. This future PE is lower than the current PE for the US Capital Markets industry at 26.7x.

- Analysts expect the number of shares outstanding to decline by 6.0% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 9.17%, as per the Simply Wall St company report.

Affiliated Managers Group Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- Strong organic growth in alternatives, particularly in private markets and liquid alternatives, is accelerating, as evidenced by record inflows and new partnerships, which are expected to continue boosting assets under management and increase both management fee and performance fee revenue streams.

- Major affiliates such as Pantheon and AQR are delivering double-digit earnings contributions, supported by their leadership in high-growth areas like private equity secondaries and tax-aware liquid alternatives, which positions AMG for robust revenue and profit expansion.

- AMG's diversified and scalable business model, with a growing focus on alternatives now comprising over 55% of EBITDA and targeting two-thirds in the near future, is enhancing long-term earnings resilience and improving net margins.

- Significant capital allocation activity, including nearly $1.2 billion in new investments and substantial share repurchases, is driving per-share earnings growth and strengthening shareholder returns.

- The proven ability to consistently innovate and form new successful partnerships, alongside ongoing investments in product development, technology, and distribution, underpins AMG's capacity to capture secular asset management demand trends and sustain long-term growth in both top-line revenue and bottom-line earnings.

Valuation

How have all the factors above been brought together to estimate a fair value?- The assumed bearish price target for Affiliated Managers Group is $195.0, which represents the lowest price target estimate amongst analysts. This valuation is based on what can be assumed as the expectations of Affiliated Managers Group's future earnings growth, profit margins and other risk factors from analysts on the more bearish end of the spectrum.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $331.0, and the most bearish reporting a price target of just $195.0.

- In order for you to agree with the bearish analysts, you'd need to believe that by 2028, revenues will be $2.1 billion, earnings will come to $594.0 million, and it would be trading on a PE ratio of 9.8x, assuming you use a discount rate of 9.2%.

- Given the current share price of $232.44, the bearish analyst price target of $195.0 is 19.2% lower. Despite analysts expecting the underlying buisness to improve, they seem to believe the market's expectations are too high.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

AnalystLowTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystLowTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystLowTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.