Key Takeaways

- Strength in NerdWallet's Insurance segment and vertical integration could boost revenue growth, net margins, and earnings through market expansion and deeper consumer relationships.

- Expanding into new categories and enhancing consumer engagement could diversify income and improve retention, thus positively impacting financial sustainability and net earnings.

- Challenges such as evolving trade policies, declining credit card revenue, and reliance on performance marketing may hinder NerdWallet's long-term profitability and earnings growth.

Catalysts

About NerdWallet- Operates a digital platform that provides financial guidance to consumers and small and mid-sized businesses (SMB) in the United States, the United Kingdom, Australia, and Canada.

- The continued strength in NerdWallet's Insurance business, driven by improvements in shopping experiences and market normalization, could lead to sustained revenue growth as the market continues to expand and premiums grow faster than GDP.

- Vertical integration, such as the integration of Next Door Lending, enhances NerdWallet's ability to capture more value by improving unit economics and driving deeper consumer relationships, potentially boosting net margins and earnings.

- The expansion into new categories and audiences, including travel rewards and growing organic channels, could lead to increased revenue by tapping into new markets and diversifying income streams.

- The focus on creating more direct, engaged relationships with consumers through enhanced user experiences and data-driven engagement strategies is likely to improve customer retention and lifetime value, positively impacting revenue and net margins.

- Investments in performance marketing capabilities and a focus on capital efficiency are expected to drive free cash flow generation, contributing to improved financial sustainability and potentially enhancing net earnings.

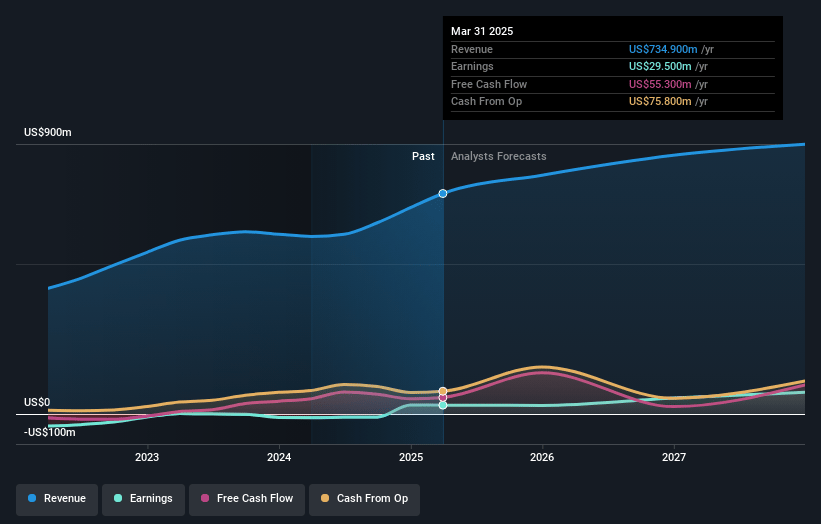

NerdWallet Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming NerdWallet's revenue will grow by 7.2% annually over the next 3 years.

- Analysts assume that profit margins will increase from 4.0% today to 8.2% in 3 years time.

- Analysts expect earnings to reach $74.5 million (and earnings per share of $0.91) by about July 2028, up from $29.5 million today.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 16.0x on those 2028 earnings, down from 26.2x today. This future PE is greater than the current PE for the US Consumer Finance industry at 9.5x.

- Analysts expect the number of shares outstanding to decline by 5.33% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 7.32%, as per the Simply Wall St company report.

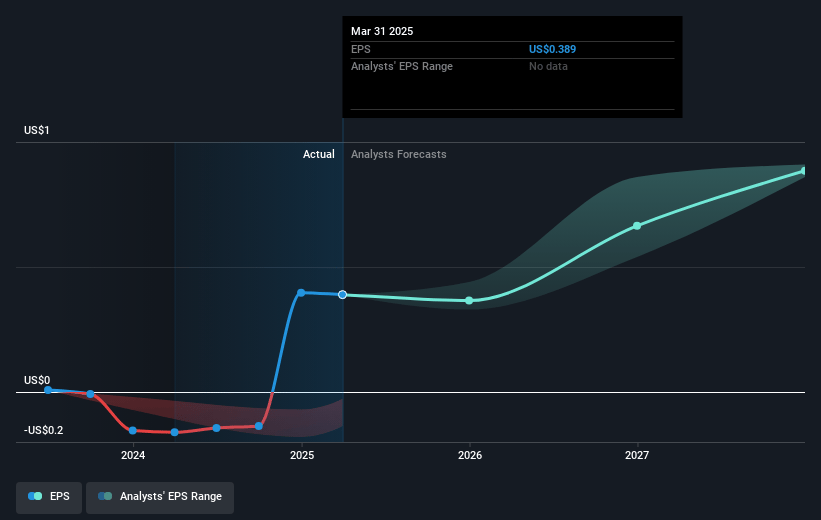

NerdWallet Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The uncertainty around evolving trade policy and potential indirect impacts, such as a material spike in unemployment or a decline in business confidence, could lead to consumers and financial institutions adopting a risk-off attitude, impacting revenue and profitability.

- The company's decision to retire the official MUU disclosure indicates that monthly unique user growth has been inversely correlated with revenue for some time, which suggests challenges in user growth metrics aligning with revenue, potentially impacting long-term earnings growth.

- Declining revenue in the credit card segment, which fell 24% year-over-year in Q1, highlights challenges within this category, possibly weakening overall revenue if the trend continues.

- Heavy reliance on performance marketing and potentially high costs relative to revenue in rapidly growing segments like Insurance could limit profit margins and may not be sustainable as these segments mature.

- The uncertain macroeconomic environment, including elevated mortgage rates and weakened demand in SMB products, poses risks to steady revenue streams in these areas, potentially impacting net margins.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $15.333 for NerdWallet based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $19.0, and the most bearish reporting a price target of just $12.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be $904.4 million, earnings will come to $74.5 million, and it would be trading on a PE ratio of 16.0x, assuming you use a discount rate of 7.3%.

- Given the current share price of $10.38, the analyst price target of $15.33 is 32.3% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.