Key Takeaways

- Optimizing processes to improve margins and fund growth, Yum China's operational efficiencies and innovation initiatives aim to enhance revenue.

- Strategic expansion in delivery, stores, and shareholder returns targets market growth, profitability, and increased stock value.

- Yum China's innovation reliance and strategy adjustments, amidst macroeconomic and competitive challenges, could pressure margins and earnings if execution and consumer demand don't meet expectations.

Catalysts

About Yum China Holdings- Owns, operates, and franchises restaurants in the People’s Republic of China.

- Yum China's focus on operational efficiency through initiatives like Project Fresh Eye and Project Red Eye aims to simplify and automate processes, which can lead to savings that improve net margins and fund further innovation and revenue growth.

- The introduction and expansion of innovative business models, such as KCOFFEE Cafes and Pizza Hut WOW, are expected to broaden the addressable market, drive incremental sales, and improve earnings through capture of new customer demands.

- The strategic adjustment of delivery fees and entry price offerings, along with increased delivery coverage, aims to enhance delivery sales growth, which is a high-margin revenue stream expected to continue contributing positively to overall revenue and net margins.

- Yum China's accelerated franchise development and new store models designed for strategic locations and lower-tier cities are projected to offer lower capital requirements and quicker profitability, potentially enhancing overall earnings and returns on invested capital.

- Continued focus on returning capital to shareholders, with stepped-up buyback and dividend plans, is likely to increase EPS and signal confidence in Yum China's cash-generating capabilities, potentially driving future stock valuation improvements.

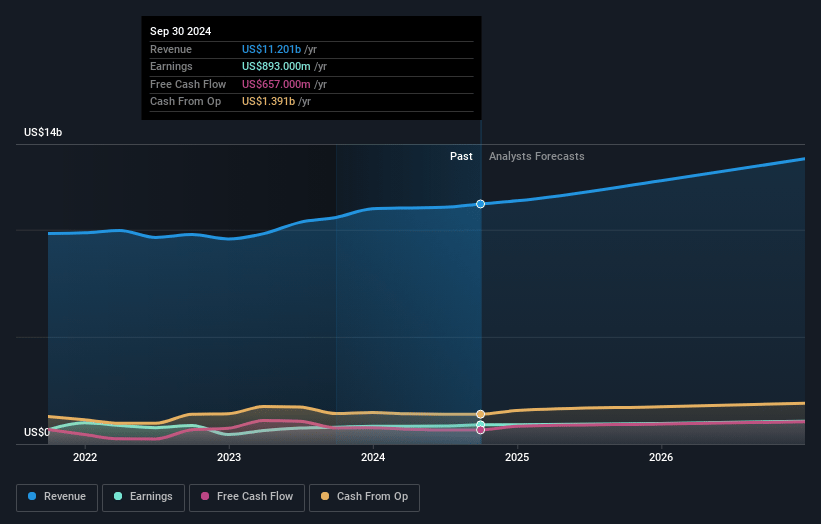

Yum China Holdings Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Yum China Holdings's revenue will grow by 8.7% annually over the next 3 years.

- Analysts assume that profit margins will increase from 8.0% today to 8.3% in 3 years time.

- Analysts expect earnings to reach $1.2 billion (and earnings per share of $3.21) by about January 2028, up from $893.0 million today. However, there is some disagreement amongst the analysts with the more bearish ones expecting earnings as low as $954 million.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 23.1x on those 2028 earnings, up from 19.3x today. This future PE is lower than the current PE for the US Hospitality industry at 24.3x.

- Analysts expect the number of shares outstanding to decline by 0.3% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 8.66%, as per the Simply Wall St company report.

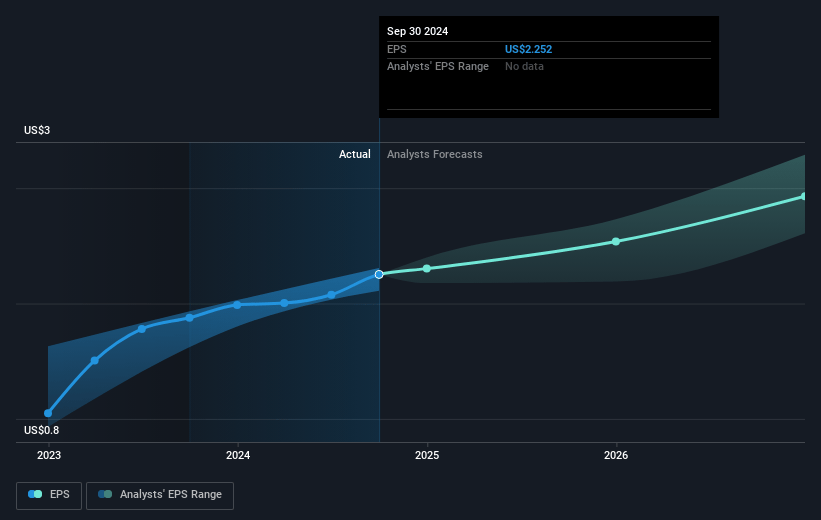

Yum China Holdings Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- Yum China's reliance on innovations such as KCOFFEE and Pizza Hut WOW may pose risks if these initiatives fail to maintain customer interest or if operational efficiencies are not achieved as projected, potentially impacting revenue growth and profit margins.

- The strategy of lowering Pizza Hut's ticket average to appeal to a mass market could pressure same-store sales while the increased competition and cautious consumer spending in China might dilute growth, affecting net margins.

- The company's increasing focus on franchising aims to optimize CapEx and enhance ROIC, but it may limit direct revenue control and quality assurance, which might impact overall earnings.

- Uncertain macroeconomic conditions and delayed impact of stimulus policies in China could pose risks to Yum China's sales growth and consumer demand, potentially stagnating revenue projections.

- While strategic, the dual focus on expanding stores and increasing franchisee openings poses execution risks; if new stores don't achieve profitability expectations, this will pressure earnings.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $57.82 for Yum China Holdings based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $76.0, and the most bearish reporting a price target of just $35.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be $14.4 billion, earnings will come to $1.2 billion, and it would be trading on a PE ratio of 23.1x, assuming you use a discount rate of 8.7%.

- Given the current share price of $45.66, the analyst's price target of $57.82 is 21.0% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Read more narratives

There are no other narratives for this company.

View all narratives