Narratives are currently in beta

Key Takeaways

- Chili's marketing campaigns and menu strategies are driving sales growth and improving operational efficiency, potentially enhancing revenue and net margins.

- Investments in technology and premium offerings are boosting productivity and average checks, likely improving long-term earnings and profitability.

- Initiatives like ERP implementation and ad investments pose risks to operational efficiency and margins, while sales strategies might affect revenue stability during downturns.

Catalysts

About Brinker International- Engages in the ownership, development, operation, and franchising of casual dining restaurants in the United States and internationally.

- Chili's is seeing impressive sales growth and increased customer traffic, driven by successful marketing campaigns such as the Big Smasher and 3 for Me promotions, indicating potential for sustained revenue growth.

- The company is focusing on menu simplification and enhancing its core offerings, which could lead to improved net margins by optimizing operational efficiency and scaling profitable items.

- The introduction of premium product offerings, like the super premium Don Julio margarita, alongside successful pricing strategies are contributing to higher average checks, which may improve earnings.

- Brinker International is investing in technology and data analytics, such as implementing a new Oracle ERP system, to boost productivity and operational stability, likely impacting long-term net margins and profitability positively.

- Strategy and leadership efforts at Maggiano's, including simplification and menu innovation, aim to revitalize the brand and improve 4-wall economics, potentially enhancing future revenue and operating margins.

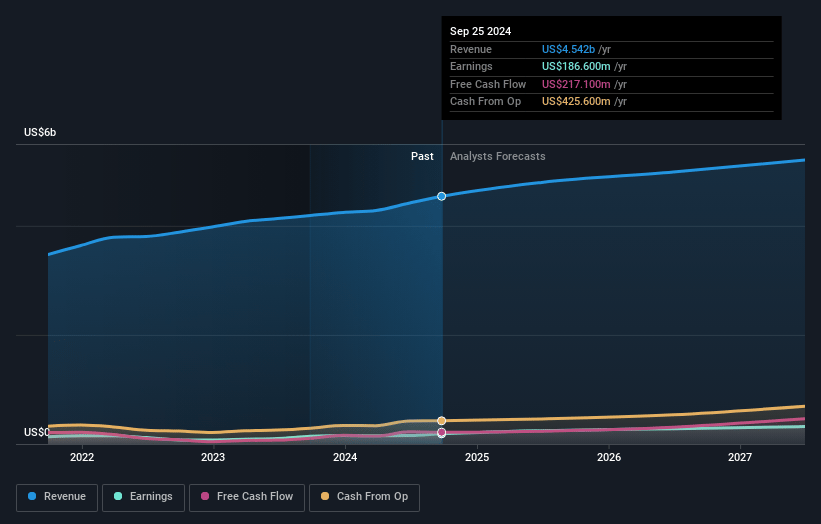

Brinker International Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Brinker International's revenue will grow by 6.2% annually over the next 3 years.

- Analysts assume that profit margins will increase from 4.1% today to 7.4% in 3 years time.

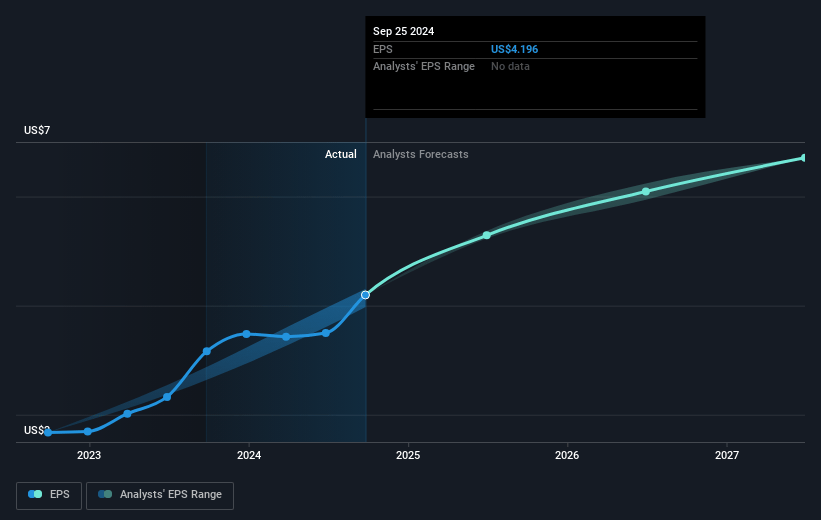

- Analysts expect earnings to reach $405.4 million (and earnings per share of $7.85) by about January 2028, up from $186.6 million today.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 22.9x on those 2028 earnings, down from 36.8x today. This future PE is lower than the current PE for the US Hospitality industry at 24.3x.

- Analysts expect the number of shares outstanding to grow by 5.13% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 8.07%, as per the Simply Wall St company report.

Brinker International Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- New initiatives like the Oracle ERP system implementation come with typical risks of large-scale technology transitions, which could potentially cause disruptions or unforeseen costs, affecting operational efficiency and margins.

- Maggiano's faces traffic declines due to initiatives like removing the $6 take-home meals, which could negatively impact sales revenue and customer counts in the short term.

- The focus on modernizing back-office systems and reallocation of labor might lead to increased capital expenditures in the near term, potentially influencing net profitability.

- The ongoing investment in advertising, which is expected to ramp up significantly compared to last fiscal year, could strain operating margins if not matched by a commensurate increase in sales growth.

- Chili's has experienced a return to emphasizing broader value bundles over previous discounting strategies, which could risk losing price-sensitive customers, potentially impacting revenue stability during economic downturns.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $144.2 for Brinker International based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $170.0, and the most bearish reporting a price target of just $97.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be $5.4 billion, earnings will come to $405.4 million, and it would be trading on a PE ratio of 22.9x, assuming you use a discount rate of 8.1%.

- Given the current share price of $154.61, the analyst's price target of $144.2 is 7.2% lower. The relatively low difference between the current share price and the analyst consensus price target indicates that they believe on average, the company is fairly priced.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Read more narratives

There are no other narratives for this company.

View all narratives