Last Update 17 Jun 26

JACK: Debt Refinancing Will Set Stage For Interim CEO EBITDA Execution

Analysts have reduced their expectations for Jack in the Box, cutting price targets across the Street, with several now clustered in the low to mid teens in dollar terms. They cite pressured same-store sales, execution missteps, franchisee profitability challenges and refinancing needs that could increase annual interest expense.

Analyst Commentary

Recent commentary on Jack in the Box underscores a cautious tone overall, but it also highlights a few areas that bullish analysts see as potential supports for the stock, particularly around management changes, guidance, and valuation reset after the latest earnings miss.

One research desk shifted Jack in the Box to a Neutral rating after calling out what it viewed as prior mistakes in category expansion, store investment and market selection, while also flagging the need to refinance about US$650m of debt within nine months. That refinancing is described as a clear swing factor for earnings, with one estimate pointing to about US$1 per share of annual EPS pressure if the debt is simply replaced at higher rates.

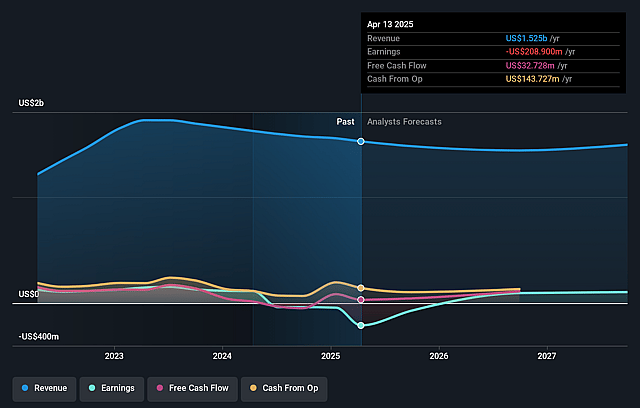

Across the rest of the Street, most of the action has come through lower price targets tied to weaker same-store sales, lower 2026 guidance and pressure on franchisee profitability. Same-store sales declining 3.8% in fiscal Q2 and reduced full year expectations have fed into more conservative models, with some analysts explicitly building in further same-store sales declines into their outer year assumptions.

At the same time, not every firm is framing Jack in the Box purely as a problem story. A few bullish analysts continue to see a path for execution improvement and some stability in the long term outlook, particularly as the company updates guidance and resets expectations.

Bullish Takeaways

- Some bullish analysts highlight the company’s updated 2026 EBITDA guidance, which they say still fully captures consensus estimates, suggesting current valuation already reflects a fair amount of operating risk if Jack in the Box can deliver on its plan.

- A group of bullish analysts has raised price targets into the low to mid teens, indicating they see recent weakness and the step down in expectations as having reset the bar to levels they view as more reasonable for the stock.

- Commentary around same-store sales trends described as moving toward “flattish” into fiscal Q3 is viewed by some bullish analysts as an early sign that the sharp Q2 shortfall may not be repeating at the same pace, which they see as supportive for stabilizing earnings expectations.

- The appointment of chairman Mark King as interim CEO is cited by certain bullish analysts as a potential execution catalyst, with the leadership change framed as an opportunity to refocus on store operations, capital allocation and franchisee health, areas that directly tie into Jack in the Box valuation and growth prospects.

What’s in the News for Jack in the Box

- The board appointed Mark King as Interim CEO of Jack in the Box, effective May 13, 2026, succeeding Lance Tucker as of May 8, 2026. King brings prior CEO experience at Xponential Fitness, Taco Bell and TaylorMade, plus leadership roles at adidas North America. (Source: Company announcement)

- Jack in the Box issued new guidance for fiscal 2026, indicating an expected low single digit same-store sales decline versus fiscal 2025. (Source: Corporate guidance update)

- The company reported completion of its US$75m share repurchase program announced on November 21, 2023, buying back 1,209,306 shares, or 6.24% of shares, with no additional repurchases between January 19 and April 12, 2026. (Source: Buyback tranche update)

- Jack in the Box launched a limited-time collaboration with Hot Ones, introducing the Hot Ones Munchie Meal and related items, including Sriracha Curly Fry Burger and Buffalo Chick-N-Tater Melt variants, Hot Ones Sauced & Loaded Fries, value meals and a paid add-on of The Last Dab: Apollo sauce, available June 1 to July 22. (Source: Product announcement)

- As part of its 75th anniversary promotions, Jack in the Box introduced the Smashed Jack Sliders Munchie Meal, featuring Smashed Jack Sliders, new collectibles and a promotion with a chance to win US$75,000. (Source: Product announcement)

Valuation Changes for Jack in the Box Stock

- Fair Value: Model fair value remains effectively unchanged at about $24.35 per share, indicating no material shift in the central valuation output.

- Discount Rate: The discount rate is unchanged at 12.46%, so the required return used in the model is consistent with prior assumptions.

- Revenue Growth: Forecast revenue growth has been marked down slightly, from a prior decline of 8.40% to a somewhat steeper decline of 8.40% on an annualized basis.

- Net Profit Margin: Expected net profit margin has risen slightly from 11.66% to about 11.98%, implying a modestly higher profitability assumption for Jack in the Box.

- Future P/E: The implied future P/E multiple eased from 5.13x to about 4.99x, reflecting a slightly lower valuation multiple being applied to expected earnings.

Key Takeaways

- Rapid digital adoption, urban expansion, and strong appeal among diverse, younger consumers position Jack in the Box for outperformance in major markets and long-term sales growth.

- Accelerated restaurant upgrades, franchisee demand, and innovative menu strategies are expected to drive sustained traffic, higher per-unit performance, and greater market share.

- High geographic concentration, rising costs, weakening key customer demand, and reliance on short-term tactics threaten Jack in the Box's sustained revenue growth and financial stability.

Catalysts

About Jack in the Box- Operates and franchises quick-service restaurants under the Jack in the Box and Del Taco brands in the United States.

- Analyst consensus expects strong revenue growth from new market openings, but current performance in Chicago shows outperformance above legacy expansion markets and suggests a higher ceiling for new market ramp, indicating long-term upside to system sales growth as urban infill accelerates and brand relevancy rises with urban, multicultural populations.

- While analysts broadly see technology modernization and digital as a positive for throughput and retention, Jack in the Box has reached a digital sales penetration threshold faster than expected, and with further enhancements (including loyalty and data-driven marketing), the brand could drive sustained step-changes in same-store sales and a structural boost to EBITDA margins by leveraging digital ordering and customer analytics more aggressively than peers.

- The company's persistent over-indexing with diverse and younger demographics, especially Hispanic guests in high-density, fast-growing US markets, positions Jack in the Box to capture incremental market share and comp outperformance as these segments recover their spending power, fueling a long-term lift in traffic and revenue resilience across cycles.

- The multiyear plan to touch and upgrade an additional 1,000+ restaurants, backed by exceptionally strong franchisee demand for modernization funding (over three times oversubscribed in prior rounds), creates a robust pipeline for accelerated asset refresh, which should drive higher average unit volumes, improved customer satisfaction, and meaningfully improved ROIC.

- Jack in the Box's aggressive menu architecture overhaul-including more value tier offerings, culturally relevant limited-time launches, leveraging 24-hour and variety strengths, and third-party facilitated delivery-will drive higher frequency and capture incremental share of wallet from consumers seeking affordable, craveable, and convenient dining, improving both transaction volumes and average check size.

Jack in the Box Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

- This narrative explores a more optimistic perspective on Jack in the Box compared to the consensus, based on a Fair Value that aligns with the bullish cohort of analysts.

- The bullish analysts are assuming Jack in the Box's revenue will decrease by 8.4% annually over the next 3 years.

- The bullish analysts assume that profit margins will increase from -7.4% today to 12.0% in 3 years time.

- The bullish analysts expect earnings to reach $131.9 million (and earnings per share of $6.69) by about June 2029, up from -$105.5 million today. However, there is some disagreement amongst the analysts with the more bearish ones expecting earnings as low as $87.5 million.

- In order for the above numbers to justify the price target of the more bullish analyst cohort, the company would need to trade at a PE ratio of 5.2x on those 2029 earnings, up from -2.3x today. This future PE is lower than the current PE for the US Hospitality industry at 22.2x.

- The bullish analysts expect the number of shares outstanding to grow by 1.01% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 12.46%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- Jack in the Box's heavy concentration in the Western and Southwestern U.S.-notably California and Texas-makes it especially exposed to regional economic downturns, demographic shifts, or competitive pressures, limiting its long-term revenue growth potential and leaving it vulnerable to ongoing sales declines as indicated by the most recent same-store sales decreases.

- Persistently rising labor costs, especially driven by minimum wage hikes and increased payroll taxes in core markets like California, are compressing restaurant-level margins and directly threaten the company's net margins despite occasional price increases.

- The company's sales and traffic softness among key customer segments, particularly the low-income and Hispanic consumer bases which Jack in the Box "significantly over-indexes" to, reveals a secular risk if these groups continue reducing spending, directly affecting top-line revenue for an extended period.

- Despite efforts to innovate with menu and technology, the company has historically faced stagnation in menu differentiation and has been reliant on short-term product promotions and price-centric value offers, which risks longer-term brand erosion and undermines sustainable gains in same-store sales or earnings growth.

- Closure of underperforming restaurants as part of the JACK on Track initiative and planned asset sales may temporarily improve franchisee portfolios, but the high number of closures and continuing costs for modernization, coupled with significant outstanding debt and discontinued dividend, may weaken free cash flow and earnings if sales and profit recovery do not materialize as planned.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The assumed bullish price target for Jack in the Box is $24.35, which represents up to two standard deviations above the consensus price target of $16.04. This valuation is based on what can be assumed as the expectations of Jack in the Box's future earnings growth, profit margins and other risk factors from analysts on the bullish end of the spectrum.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $28.0, and the most bearish reporting a price target of just $12.0.

- In order for you to agree with the more bullish analyst cohort, you'd need to believe that by 2029, revenues will be $1.1 billion, earnings will come to $131.9 million, and it would be trading on a PE ratio of 5.2x, assuming you use a discount rate of 12.5%.

- Given the current share price of $12.62, the analyst price target of $24.35 is 48.2% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Jack in the Box?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystHighTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystHighTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystHighTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.