Key Takeaways

- Investment in generative AI and automation aims to enhance product engagement and efficiency, improving net margins and driving subscription revenue growth.

- Expanding English content and regional marketing is expected to boost international market share and sustain user growth.

- Heavy reliance on AI features and word-of-mouth growth may hamper revenue scaling, as costly tiers deter conversions in lower-income regions.

Catalysts

About Duolingo- Operates as a mobile learning platform in the United States, the United Kingdom, and internationally.

- Duolingo is heavily investing in generative AI and automation to enhance product engagement and efficiency, which is expected to improve net margins over time.

- The introduction of the Duolingo Max tier, especially with the AI-powered Video Call feature, is anticipated to drive significant subscription revenue growth as it is rolled out to more users, particularly English learners who show strong demand for conversational practice.

- Duolingo is committed to expanding its intermediate and advanced English learning content, positioning itself to capture more revenue from a market where 80% of global language learning spend is focused on English.

- The expansion of regional marketing managers in various countries is expected to drive user growth and improve localized product adoption, which can enhance revenue and market share internationally.

- Ongoing product improvements, including social marketing and feature enhancements, are expected to sustain high DAU growth, contributing to higher future bookings and revenue, with an aim to significantly grow the overall subscriber base.

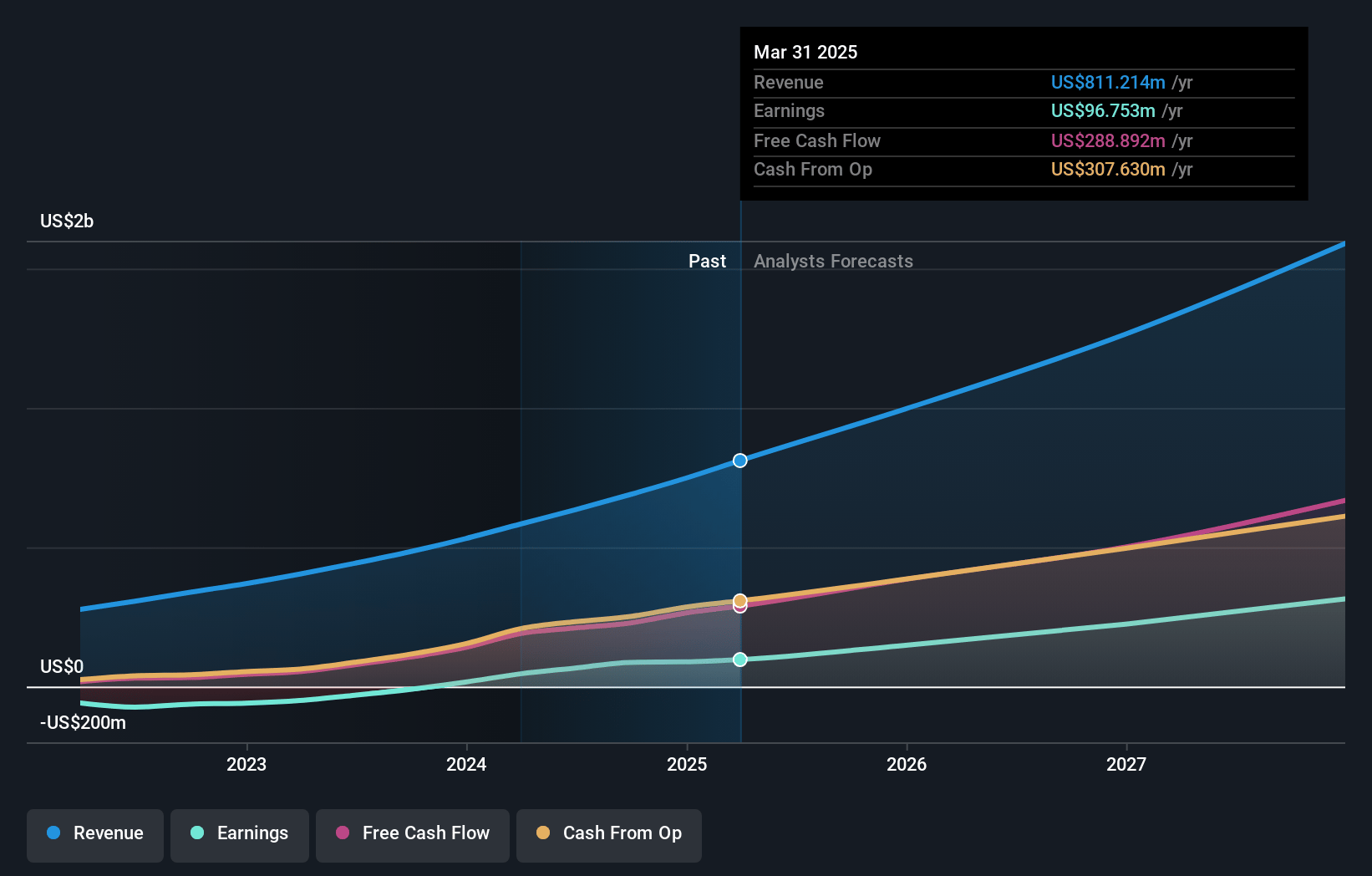

Duolingo Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Duolingo's revenue will grow by 30.0% annually over the next 3 years.

- Analysts assume that profit margins will increase from 12.6% today to 17.9% in 3 years time.

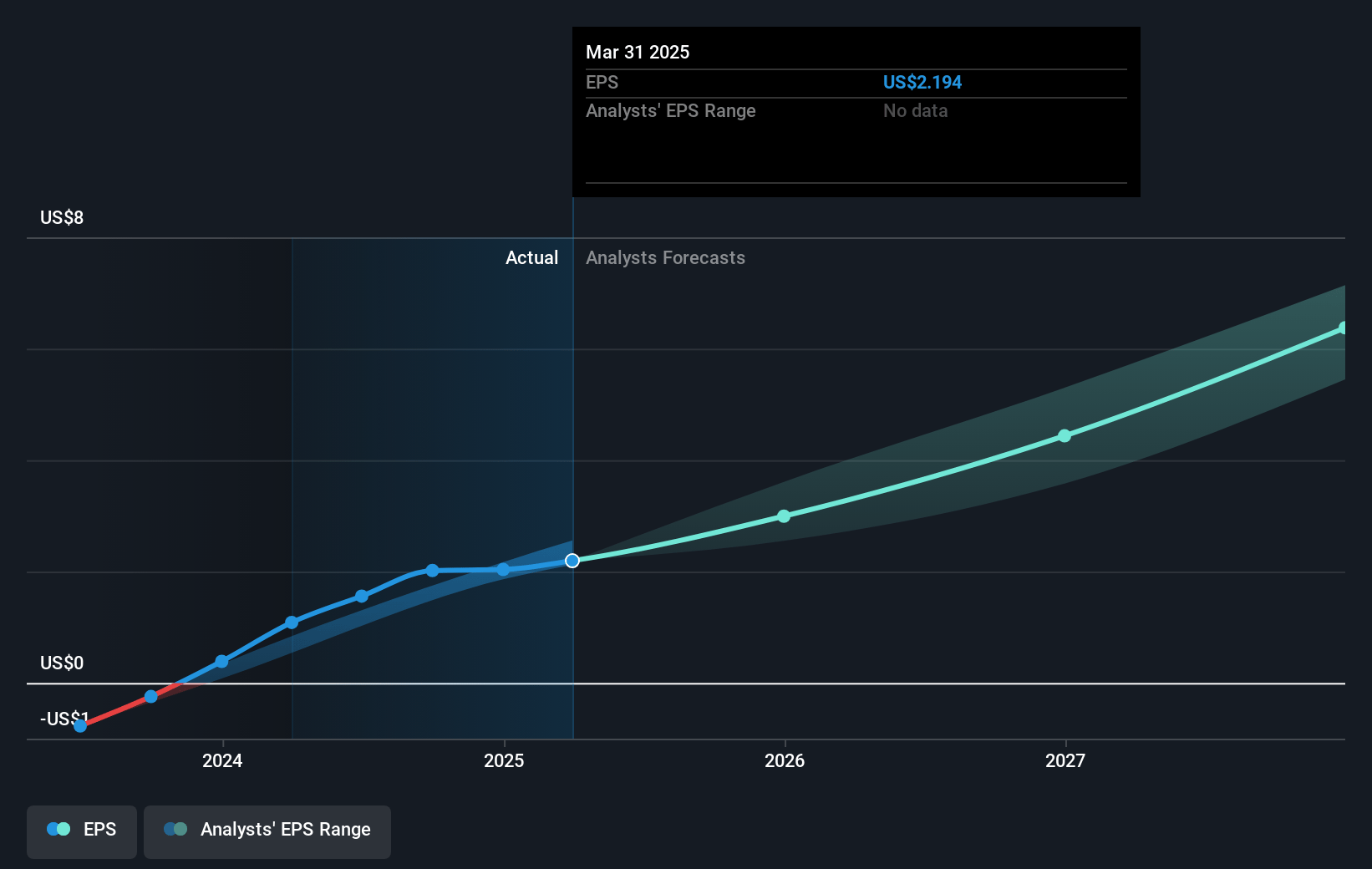

- Analysts expect earnings to reach $271.8 million (and earnings per share of $5.47) by about January 2028, up from $86.8 million today.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 76.3x on those 2028 earnings, down from 177.8x today. This future PE is greater than the current PE for the US Consumer Services industry at 20.7x.

- Analysts expect the number of shares outstanding to grow by 4.13% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 6.31%, as per the Simply Wall St company report.

Duolingo Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The announcement highlights increased costs related to generative AI and content amortization, which could pressure gross margins even if gross profit dollars rise, potentially impacting net margins.

- Despite cross-geography marketing efforts, Duolingo's growth strategy heavily relies on word of mouth, which, while cost-effective, is not the fastest method of growth, potentially affecting future revenue scaling speed.

- The rollout of Duolingo Max with AI features is significant, but there's uncertainty regarding how quickly it will stabilize and whether it will effectively convert free users to paying subscribers, impacting long-term revenue and earnings.

- The company acknowledges higher learnability and engagement for English learners with AI features, but expensive subscription tiers may limit conversion in lower-income regions, affecting revenue potential from a significant user segment.

- Dependent on the continual improvement and rollout of new features like Video Call with Lily to maintain user engagement and growth, which if unsuccessful, could affect user retention and therefore revenue streams.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $352.52 for Duolingo based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $425.0, and the most bearish reporting a price target of just $200.27.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be $1.5 billion, earnings will come to $271.8 million, and it would be trading on a PE ratio of 76.3x, assuming you use a discount rate of 6.3%.

- Given the current share price of $350.72, the analyst's price target of $352.52 is 0.5% higher. The relatively low difference between the current share price and the analyst consensus price target indicates that they believe on average, the company is fairly priced.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Read more narratives

WA

waqifalam

Community Contributor

Good growth potential under bullish market conditions

Catalysts Duolingo Max, featuring AI-enabled features, somewhat positively adopted. Steady growth continue in current market conditions.

View narrativeUS$306.52

FV

25.7% overvalued intrinsic discount24.41%

Revenue growth p.a.

0users have liked this narrative

0users have commented on this narrative

1users have followed this narrative

5 months ago author updated this narrative