Key Takeaways

- Strategic investments in new facilities and product innovation are likely to broaden market reach and enhance long-term revenue growth.

- Strong financial health and a robust order backlog suggest sustained, stable growth with potential for increased market expansion.

- Potential supply chain delays, investment risks, and reliance on defense budgets alongside election uncertainties threaten Graham Corporation's revenue and market stability.

Catalysts

About Graham- Designs and manufactures fluid, power, heat transfer, and vacuum technologies for chemical and petrochemical processing, defense, space, petroleum refining, cryogenic, energy, and other industries.

- The launch of the NextGen steam injector nozzle, expected to enhance efficiency and profitability, presents a total market opportunity of over $50 million in the next 5 to 10 years, likely driving revenue growth.

- The establishment of a new cryogenic propellant testing facility is anticipated to provide scalable testing solutions and enter new high-demand markets, expected to improve revenue and broaden market reach.

- The recent land acquisition in Colorado aims to address space constraints and support the growth of the Barber-Nichols subsidiary, suggesting future revenue expansion capabilities through new product lines and emerging programs.

- Strong financial position with no debt and significant cash reserves enables Graham to confidently pursue growth initiatives and make strategic investments, likely impacting long-term earnings and stability.

- Record backlog of $407 million and a robust book-to-bill ratio of 1.2x provide strong visibility into future revenue streams, indicating sustained growth and margin expansion potential in upcoming years.

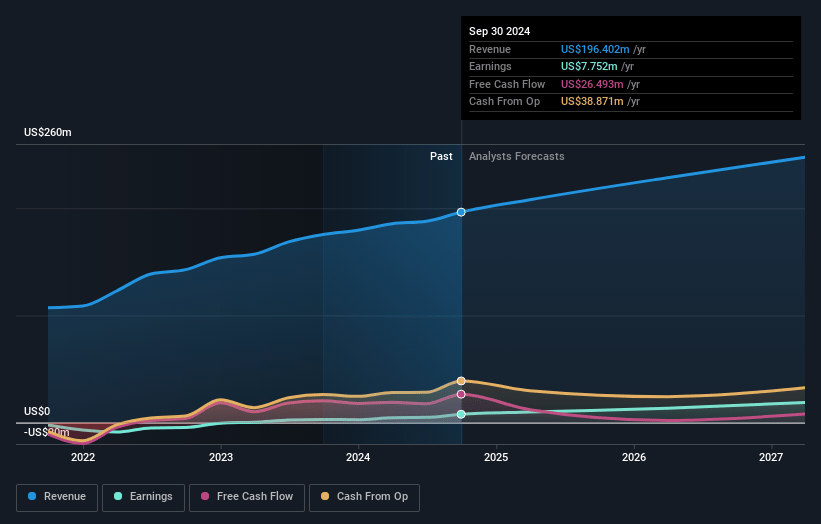

Graham Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Graham's revenue will grow by 9.8% annually over the next 3 years.

- Analysts assume that profit margins will increase from 3.9% today to 8.2% in 3 years time.

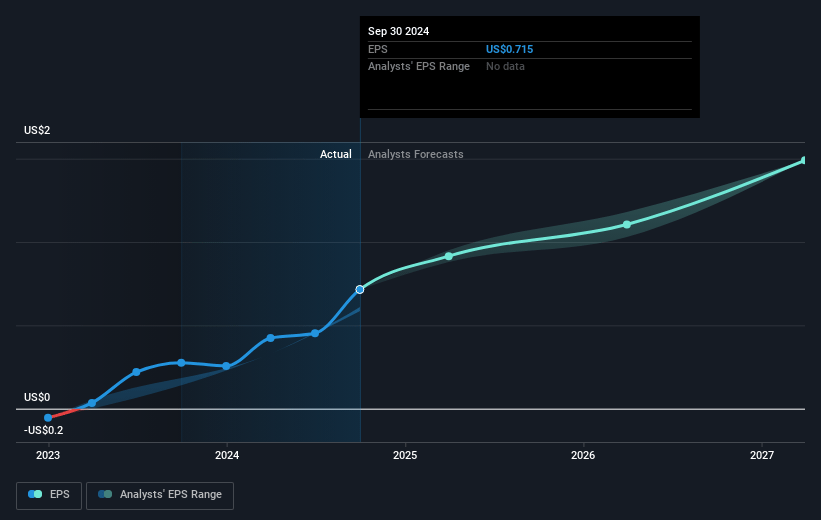

- Analysts expect earnings to reach $21.4 million (and earnings per share of $1.66) by about January 2028, up from $7.8 million today.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 35.7x on those 2028 earnings, down from 62.8x today. This future PE is greater than the current PE for the US Machinery industry at 23.3x.

- Analysts expect the number of shares outstanding to grow by 5.74% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 6.8%, as per the Simply Wall St company report.

Graham Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The potential risk of navy ship and submarine production schedule delays due to supply chain issues could impact future order rates and revenue for Graham Corporation.

- Significant investments in operations, personnel, technology, and capital expenditures may not yield the expected returns, potentially affecting net margins and long-term earnings.

- Despite a strong backlog, the conversion of orders to sales heavily relies on projections from the defense sector, which can be sensitive to changes in government defense budgets, impacting revenue stability.

- The uncertain impact of the upcoming election on defense spending and energy markets may lead to volatility in revenue streams, particularly if new policies affect current strategic priorities.

- The introduction of the NextGen steam injector nozzle depends on customer adoption and market penetration in international markets where utility costs are higher, posing a risk to revenue if the technology isn't broadly accepted.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $52.17 for Graham based on their expectations of its future earnings growth, profit margins and other risk factors.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be $260.1 million, earnings will come to $21.4 million, and it would be trading on a PE ratio of 35.7x, assuming you use a discount rate of 6.8%.

- Given the current share price of $44.67, the analyst's price target of $52.17 is 14.4% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Read more narratives

There are no other narratives for this company.

View all narratives