Last Update 07 Jul 26

Fair value Increased 37%RKLB: Iridium Deal Execution Risk Will Test Vertically Integrated Space Platform Narrative

Rocket Lab's updated analyst price target has moved higher from about $47 to roughly $64, as analysts highlight the planned Iridium acquisition as a key driver for a more vertically integrated space services platform and for refined launch pricing expectations.

Analyst Commentary

Street research around Rocket Lab has been intensely focused on the proposed Iridium acquisition, with many analysts framing it as a key step toward a more complete space services platform that couples launch, spacecraft manufacturing, and communications services under one roof.

Several firms have adjusted their price targets on Rocket Lab following the deal announcement. Recent reports describe Iridium as a largely complementary fit with Rocket Lab's existing launch and space systems operations, pointing to a combined platform that would include spectrum rights and on orbit communications capabilities alongside hardware and launch offerings.

Some analysts describe the transaction as "transformational" for Rocket Lab, highlighting the expansion into commercial, government, and defense services markets. Others focus on the fact that Iridium addresses use cases such as assured communications and low bandwidth internet of things rather than direct consumer broadband, which they see as differentiated from offerings like Starlink.

On the satellite services side, one large brokerage raised its Iridium target to US$54 after the acquisition plans were announced, citing a view that the asset is complementary to Rocket Lab and that there is a clear rationale for combining the two businesses.

Across these reports, recurring revenue potential from communications services, possible benefits from owned spectrum, and refined expectations for Electron launch pricing all show up as key factors that analysts are incorporating into their Rocket Lab valuation frameworks.

Bearish Takeaways

- Bearish analysts point out that many recent target changes, even when higher, still come with Neutral or Equal Weight ratings. They view this as a signal that current Rocket Lab valuation may already reflect a large part of the Iridium deal upside.

- There is caution around execution risk on integrating Iridium. Bearish analysts highlight the complexity of combining launch, manufacturing, and global communications services into a single platform while still moving toward profitability targets.

- Some bearish analysts flag growth risks if competitive pressure from larger space and communications companies leads to slower than expected uptake of new space based applications. In their view, this could limit the recurring revenue mix that more optimistic forecasts assume.

- Bearish commentary also points to potential downside if the deal synergies take longer than expected to materialize. This could leave Rocket Lab carrying a larger balance sheet commitment without the level of incremental revenue and margin contribution that bullish scenarios anticipate.

What’s in the News for Rocket Lab

- Rocket Lab announced a definitive agreement to acquire Iridium Communications in an US$8b cash and stock deal valued at about US$54 per Iridium share. The combination brings together Rocket Lab’s launch and satellite manufacturing with Iridium’s LEO network, L band spectrum and more than 2.55 million subscribers, and positions the company as a vertically integrated space services platform (Source: Iridium acquisition coverage).

- The company reported record Q1 2026 revenue of US$200.3 million with a contracted backlog above US$2.2b. This was supported by 31 new launch contracts for Electron and HASTE and five Neutron launches, along with acquisitions of Mynaric AG and Motiv Space Systems to bring laser communications and robotics in house (Source: Q1 2026 earnings coverage).

- Rocket Lab secured over US$1.3b in new defense contracts, including an US$816 million award for the SDA Tracking Layer Tranche 3 constellation, a US$90 million U.S. Space Force GEO mission, and US$190 million for 20 hypersonic test flights. The company also passed a key System Requirements Review for the SDA program (Source: defense contract coverage).

- NASA selected Rocket Lab for three dedicated Electron launches supporting the PolSIR and TSIS 2 science missions from Launch Complex 1 in New Zealand starting in early 2027. Reports estimate that the potential contract value could reach up to US$300 million over ten years (Source: NASA launch contracts coverage).

- Rocket Lab was added to the Nasdaq 100 Index in June 2026, reflecting its status among the largest non financial companies on Nasdaq and increasing its visibility with index tracking and institutional investors (Source: Nasdaq 100 inclusion coverage).

Valuation Changes for Rocket Lab

- Fair Value: updated from $47.00 to $64.40, indicating a higher implied valuation level in recent analyst work.

- Discount Rate: adjusted slightly higher from 7.55% to 7.87%, suggesting a modestly higher required return in current models.

- Revenue Growth: revised from 33.56% to 36.49%, reflecting higher modeled growth expectations for Rocket Lab’s top line.

- Net Profit Margin: moved from 1.24% to 0.86%, indicating lower projected profitability per dollar of revenue in the latest assumptions.

- Future P/E: increased from a very large 2,329.91x to a very large 3,857.23x, highlighting that the updated fair value is being supported by higher multiple assumptions rather than lower earnings expectations.

Catalysts

About Rocket Lab

Rocket Lab designs, manufactures and operates launch vehicles and space systems for government and commercial customers.

What are the underlying business or industry changes driving this perspective?

- Escalating capital intensity for Neutron, with cumulative spending already moving well above the original 250 million to 300 million budget range, risks structurally higher depreciation and R&D run rates. This could cap future operating leverage and delay sustainable earnings.

- Reliance on rapid growth in government space and defense programs, including SDA transport layers and hypersonic test initiatives, exposes revenue to budget debates, shutdowns and award timing. This could drive lumpier backlog conversion and slower top line growth than current expectations.

- Vertical integration and aggressive M&A, from component suppliers to payload and sensor businesses, increase fixed costs and integration complexity. This raises the risk that acquired revenue underperforms and compresses consolidated gross margins and free cash flow.

- Ambitious launch cadence targets for Electron and future Neutron missions depend on scaling highly specialized manufacturing and test infrastructure. Execution missteps or supply bottlenecks could constrain capacity, reduce launch availability and limit revenue growth while overhead remains elevated.

- Growing competition across small launch, satellite manufacturing and payload markets, including larger primes with deep capital bases, may force sharper pricing and contract terms. This could pressure average selling prices, net margins and long term return on invested capital.

Assumptions

How have these above catalysts been quantified?

- This narrative explores a more pessimistic perspective on Rocket Lab compared to the consensus, based on a Fair Value that aligns with the bearish cohort of analysts.

- The bearish analysts are assuming Rocket Lab's revenue will grow by 36.5% annually over the next 3 years.

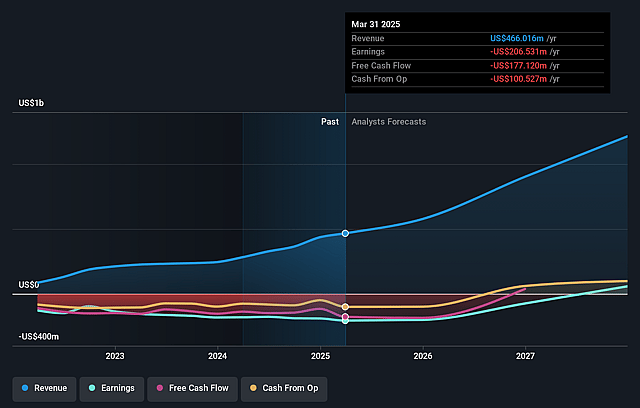

- The bearish analysts assume that profit margins will increase from -26.9% today to 0.9% in 3 years time.

- The bearish analysts expect earnings to reach $14.8 million (and earnings per share of $0.11) by about July 2029, up from -$182.6 million today. However, there is some disagreement amongst the analysts with the more bullish ones expecting earnings as high as $373.1 million.

- In order for the above numbers to justify the price target of the more bearish analyst cohort, the company would need to trade at a PE ratio of 3862.7x on those 2029 earnings, up from -295.1x today. This future PE is greater than the current PE for the US Aerospace & Defense industry at 40.6x.

- The bearish analysts expect the number of shares outstanding to grow by 7.0% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 7.87%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?

- Electron is demonstrating accelerating demand with 17 launches signed in a single quarter, a record annual launch cadence and a factory designed for significantly higher throughput, which could support sustained top line growth and operating leverage, improving revenue and earnings.

- Space Systems has scaled from small beginnings to contribute the majority of revenue with high margin satellite manufacturing, diversified government and commercial programs and a growing pipeline of large SDA and national security contracts, which may provide long duration, secular growth in space infrastructure spending that strengthens revenue visibility and margins.

- Long term government and defense trends, including hypersonic test programs like Golden Dome, SDA transport layers and increasing international agency reliance on Electron, position Rocket Lab as a key strategic supplier, which could drive structurally higher backlog, pricing power and gross margins.

- Vertical integration across launch, spacecraft buses, sensors and future laser communications, combined with disciplined M&A and a strong liquidity position above 1 billion dollars, may allow Rocket Lab to capture more of the value chain and outperform peers on cost and schedule, supporting higher net margins and cash flow over time.

- Neutron and the Archimedes engine are being developed with an emphasis on reliability, reusability and thorough ground testing, and if successful they could open a higher capacity, higher ASP launch market and enable larger satellite constellations, materially increasing long term revenue, gross margin and earnings potential.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The assumed bearish price target for Rocket Lab is $64.4, which represents up to two standard deviations below the consensus price target of $110.72. This valuation is based on what can be assumed as the expectations of Rocket Lab's future earnings growth, profit margins and other risk factors from analysts on the more bearish end of the spectrum.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $150.0, and the most bearish reporting a price target of just $60.0.

- In order for you to agree with the more bearish analyst cohort, you'd need to believe that by 2029, revenues will be $1.7 billion, earnings will come to $14.8 million, and it would be trading on a PE ratio of 3862.7x, assuming you use a discount rate of 7.9%.

- Given the current share price of $93.09, the analyst price target of $64.4 is 44.6% lower. Despite analysts expecting the underlying business to improve, they seem to believe the market's expectations are too high.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Rocket Lab?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystLowTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystLowTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystLowTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.