Last Update 18 Jun 26

DRS: Future Defense Platforms And Government Contracts Will Support Margin Upside

Analysts have lifted their consolidated price targets on Leonardo DRS stock by a few dollars, with the latest moves of $2 to $5 higher reflecting updated views on its growth outlook, profitability profile and the P/E multiples they consider appropriate.

Analyst Commentary on Leonardo DRS Stock

Recent Street research on Leonardo DRS has focused on refreshed price targets that are a few dollars higher than prior levels, with bullish analysts pointing to updated views on growth, profitability and what they see as a suitable P/E range for the stock.

Bullish analysts describe the higher targets, including moves of about $2 and $5, as reflecting their reassessment of how Leonardo DRS might execute on its current pipeline and how that could feed into future earnings power and valuation assumptions.

Across these reports, the tone remains focused on how the company is positioned in its markets, and how that positioning could support the profit profile that underpins the revised price target work.

Bullish Takeaways

- Bullish analysts highlight the recent price target increases of a few dollars as a sign that they are more comfortable using higher P/E assumptions for Leonardo DRS based on their updated modeling.

- The research points to confidence in the company’s ability to execute on its current business plans, which these analysts see as important for supporting their revised earnings and valuation frameworks.

- Positive commentary centers on Leonardo DRS having a business mix that, in their view, can support the profitability profile required to justify the higher target range.

- Some bullish analysts frame the higher targets as reflecting what they consider a more constructive view on the stock’s risk and reward balance, with execution and earnings visibility playing a key role in their stance.

What’s in the News for Leonardo DRS

- Leonardo DRS is described as a provider of advanced sensing and naval power systems with solid revenue growth, expanding profitability in FY 2025 and steady cash flow from long-term government contracts. This positions the company as a more stable defense investment option than early-stage Firefly Aerospace. (Source: recent comparative analysis, first published 11 June 2026)

- Recent coverage highlights Leonardo DRS involvement in electronic propulsion drives for the Columbia-class submarine and participation in the Golden Dome missile defense initiative. This points to additional contract opportunities linked to U.S. efforts to diversify away from larger prime contractors. (Source: program-focused news, first published 12 June 2026)

- Leonardo DRS raised its 2026 revenue guidance to a range of US$3,900m to US$3,975m from a previous range of US$3,850m to US$3,950m, giving investors updated management expectations for the year. (Source: company guidance update)

- The company reported that from 1 January 2026 to 31 March 2026 it repurchased 91,238 shares for US$4.09m, bringing total repurchases under its February 2025 authorization to 984,530 shares for US$38.9m. (Source: share buyback tranche update)

- Leonardo DRS announced multiple new products, including the Tenum 640 Orbit thermal camera module for unmanned platforms, a 2 kVA AC uninterruptible power supply for shipboard electronics, the THOR embedded computing chassis for tactical edge processing and the integration of its Maritime Mission Equipment Package on an autonomous unmanned surface vessel to provide counter UAS capabilities in the maritime domain. (Source: product announcement releases)

Valuation Changes for Leonardo DRS

- Fair Value: $59.00 is unchanged, and the updated work maintains the same central estimate for Leonardo DRS stock.

- Discount Rate: The discount rate has fallen slightly from 7.97% to 7.96%, implying a marginally lower required return in the refreshed model.

- Revenue Growth: The revenue growth assumption has risen slightly from 7.93% to 8.03%, indicating a modestly higher expected top line trajectory in the valuation framework.

- Net Profit Margin: The profit margin has edged up from 9.53% to 9.54%, reflecting a small adjustment in expected profitability for Leonardo DRS.

- Future P/E: The future P/E assumption has eased slightly from 45.0x to 44.8x, suggesting a marginally lower multiple applied in the updated valuation work.

Key Takeaways

- Alignment with rising defense budgets and rapid innovation in AI-powered battlefield solutions position the company for sustained growth and market share gains.

- U.S.-focused supply chain strategies and portfolio optimization support resilient margins, while partnerships and cross-selling drive expanded revenue streams and earnings.

- Heavy dependence on traditional defense contracts and hardware, material sourcing risks, and intensifying competition threaten revenue stability, profitability, and long-term growth prospects.

Catalysts

About Leonardo DRS- Provides defense electronic products and systems, and military support services worldwide.

- The multiyear rise in global defense budgets, particularly in the U.S. and among key allies, has created a strong, durable foundation for demand, with Leonardo DRS uniquely aligned to national priorities in shipbuilding, force protection, advanced sensors, and modernization of digital battlefield capabilities. Future increases in defense appropriations, including up to one trillion dollars and supplemental funding initiatives, are expected to provide sustained, above-market revenue growth.

- Accelerating adoption of digital technologies, artificial intelligence, and next-generation combat systems is driving demand for C5ISR, AI-powered battlefield solutions, and advanced infrared sensing—the core strengths of Leonardo DRS. The company’s rapid innovation and integration of AI processors and open operating system architectures are expected to capture meaningful share in a growing addressable market, leading to new contract wins and expanding top-line revenue.

- Investments in U.S.-based supply chain localization and increased customer preference for domestic suppliers are mitigating international supply chain risks. Leonardo DRS’s predominantly U.S. footprint and diversified supplier base position it to benefit from greater contract allocation and resilience against tariffs and raw material disruptions, supporting revenue consistency and margin stability.

- Portfolio optimization efforts, including divesting lower-margin businesses and prioritizing high-growth, high-margin segments (such as electric power, propulsion, and advanced sensors), along with operational leverage from increased program volumes, are setting the stage for meaningful net margin expansion and strong EBITDA growth over the coming years.

- Execution of organic growth initiatives alongside targeted M&A, plus deeper strategic partnerships within the Leonardo Group and externally, are expected to accelerate cross-selling, drive incremental bookings, and create new revenue streams and scale, supporting both top-line expansion and earnings growth.

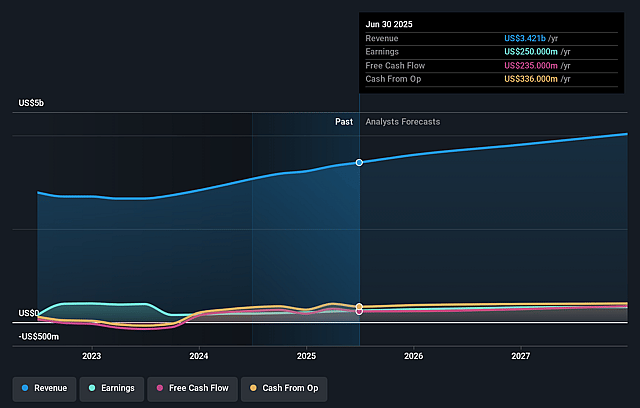

Leonardo DRS Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

- This narrative explores a more optimistic perspective on Leonardo DRS compared to the consensus, based on a Fair Value that aligns with the bullish cohort of analysts.

- The bullish analysts are assuming Leonardo DRS's revenue will grow by 8.0% annually over the next 3 years.

- The bullish analysts assume that profit margins will increase from 7.8% today to 9.5% in 3 years time.

- The bullish analysts expect earnings to reach $444.6 million (and earnings per share of $1.62) by about June 2029, up from $290.0 million today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the price target of the more bullish analyst cohort, the company would need to trade at a PE ratio of 44.9x on those 2029 earnings, up from 42.8x today. This future PE is greater than the current PE for the US Aerospace & Defense industry at 40.3x.

- The bullish analysts expect the number of shares outstanding to grow by 0.24% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 7.96%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- Heavy reliance on U.S. defense contracts makes Leonardo DRS particularly vulnerable to changes in U.S. defense spending priorities, and any fiscal tightening, procurement delays, or shifts to other areas such as cyber capabilities could lead to significant pressure on future revenues and earnings.

- Advancements in digital and cyber warfare technologies may divert government budgets away from traditional hardware such as propulsion and sensing systems, areas where DRS is highly concentrated, resulting in long-term erosion of revenues and lower net margins.

- Supply chain risks, highlighted by recent challenges in sourcing rare earth minerals such as germanium, reveal vulnerability to material cost volatility and single-source supplier disruptions, which can compress profits and pressure margins, as was evident in the ASC segment’s recent performance.

- The long and unpredictable nature of the defense procurement cycle leads to uneven cash flows and potential delays in revenue recognition, heightening risk around quarterly results and introducing volatility in both earnings and free cash flow over the long term.

- Rising competition from both innovative startups and established global defense companies, combined with increasing regulatory scrutiny, may reduce pricing power and access to international markets, negatively impacting Leonardo DRS’s ability to expand revenue streams and sustain future profitability.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The assumed bullish price target for Leonardo DRS is $59.0, which represents up to two standard deviations above the consensus price target of $52.9. This valuation is based on what can be assumed as the expectations of Leonardo DRS's future earnings growth, profit margins and other risk factors from analysts on the bullish end of the spectrum.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $59.0, and the most bearish reporting a price target of just $47.0.

- In order for you to agree with the more bullish analyst cohort, you'd need to believe that by 2029, revenues will be $4.7 billion, earnings will come to $444.6 million, and it would be trading on a PE ratio of 44.9x, assuming you use a discount rate of 8.0%.

- Given the current share price of $46.58, the analyst price target of $59.0 is 21.1% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Leonardo DRS?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystHighTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystHighTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystHighTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.