Last Update 01 May 25

Fair value Decreased 3.89%Key Takeaways

- Fortnox's focus on increasing usage among existing customers could drive higher revenue growth through improved ARPC and expanded financial services.

- Strong EBIT margin performance and cost management may sustain high margins and earnings growth as Fortnox's financial segment and customer base expand.

- Reluctance to expand internationally and strategic shifts if privatized may threaten revenue growth and future earnings stability.

Catalysts

About Fortnox- Provides smart technical products, packages, services, and integrations for financial and administration applications in small and medium sized businesses, accounting firms, and organizations in Sweden.

- Fortnox's focus on increasing usage among existing customers highlights significant growth opportunities within its current customer base, which is likely to drive higher average revenue per customer (ARPC) and boost overall revenue growth.

- The strategic emphasis on payments and financing as part of core workflows within Fortnox's platform could increase transaction-based revenue, enhancing future revenue growth and possibly improving net margins due to the potentially higher margins associated with financial services.

- Continued growth in Fortnox's Financial Services segment, which includes payments and factoring, shows potential for substantial revenue increases, as evidenced by the 34% growth in this segment. This is likely to contribute positively to overall revenue and earnings growth.

- The adoption and user base increase for Fortnox ID, which enhances customer interaction with the company's ecosystem, is expected to lead to higher customer retention and increased cross-sell opportunities, supporting future revenue growth and potentially improving net margins through increased efficiencies.

- The strong EBIT margin performance, partially driven by cost management such as lower-than-expected employee cost growth, indicates the possibility of sustaining high margins and earnings growth in the future as Fortnox continues to expand its business.

Fortnox Future Earnings and Revenue Growth

Assumptions

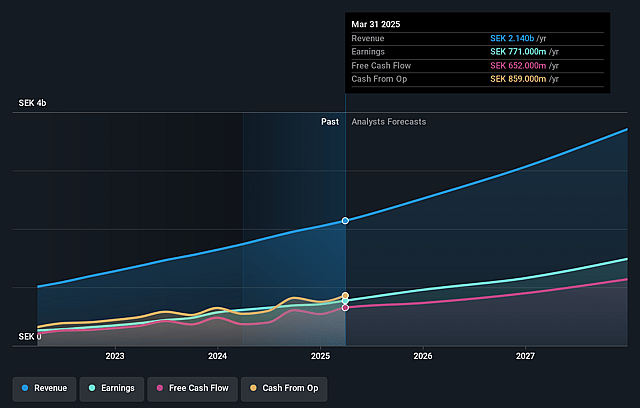

How have these above catalysts been quantified?- Analysts are assuming Fortnox's revenue will grow by 20.1% annually over the next 3 years.

- Analysts assume that profit margins will increase from 36.0% today to 39.3% in 3 years time.

- Analysts expect earnings to reach SEK 1.5 billion (and earnings per share of SEK 2.39) by about May 2028, up from SEK 771.0 million today. However, there is some disagreement amongst the analysts with the more bearish ones expecting earnings as low as SEK1.3 billion.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 40.0x on those 2028 earnings, down from 68.8x today. This future PE is greater than the current PE for the SE Software industry at 33.7x.

- Analysts expect the number of shares outstanding to remain consistent over the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 6.2%, as per the Simply Wall St company report.

Fortnox Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- Customer growth numbers are slightly below target, with actual growth from new customers being lower and relying on acquisitions like Boardeaser to maintain growth, which could affect revenue growth if not improved.

- The divestment from the previous year had a negative impact on subscription revenue, causing a 7% decrease, which could impact net sales and profitability if similar events occur.

- Employee costs appear to have grown at a lower rate due to a reorganization, raising concerns about potential underinvestment in human resources which could impact future operational capacity and net margins.

- Strategic expansion into international markets has been hinted at but not clearly planned, presenting execution risk and uncertainty about revenue growth from new geographies.

- Concerns about a potential change in business direction if the company goes private, as this can lead to strategic shifts that might not align with current growth plans, affecting future earnings.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of SEK79.625 for Fortnox based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of SEK90.0, and the most bearish reporting a price target of just SEK40.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be SEK3.7 billion, earnings will come to SEK1.5 billion, and it would be trading on a PE ratio of 40.0x, assuming you use a discount rate of 6.2%.

- Given the current share price of SEK86.98, the analyst price target of SEK79.62 is 9.2% lower. The relatively low difference between the current share price and the analyst consensus price target indicates that they believe on average, the company is fairly priced.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.