Key Takeaways

- UBL's employee-centric shift and focus on low-cost deposits aim to enhance customer satisfaction and optimize capital structure, potentially boosting revenue and net margins.

- Strategic divestment and investments in treasury securities and investment-grade bonds aim for sustainable earnings growth and stability while reducing risk.

- UBL’s strategic initiatives in employee focus, low-cost deposits, risk management, and shareholder returns strengthen its growth, profitability, and earnings stability.

Catalysts

About United Bank- Provides commercial banking and related services in Pakistan, Europe, and the Middle East.

- UBL's strategic shift to become an employee-centric bank is expected to enhance customer service, leading to higher customer satisfaction and thus, potentially driving revenue growth.

- The bank's focus on increasing low-cost deposit growth, especially current accounts, is aimed at optimizing its capital structure, which could positively impact net margins through reduced funding costs.

- The divestment of UBL U.K. operations has strengthened the bank's capital adequacy ratio, providing a catalyst for sustainable earnings growth as resources are shifted towards more profitable ventures.

- UBL has taken a strategic position in short-term T-bills and long-term treasury bonds to protect its earnings against anticipated interest rate reductions, which could result in a stable earnings outlook for 2025 and 2026.

- The shift in strategy to invest primarily in investment-grade bonds in their GCC operations aims to maintain earnings stability while reducing risk, potentially impacting the bank's overall earnings positively.

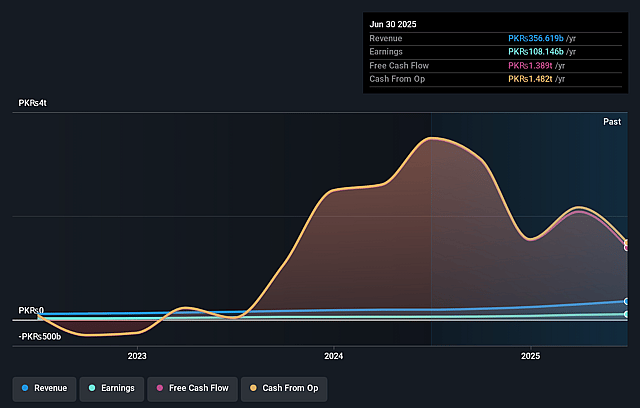

United Bank Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming United Bank's revenue will decrease by 17.4% annually over the next 3 years.

- Analysts assume that profit margins will increase from 29.3% today to 34.7% in 3 years time.

- Analysts expect earnings to reach PKR 41.5 billion (and earnings per share of PKR 55.38) by about February 2028, down from PKR 62.2 billion today.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 29.2x on those 2028 earnings, up from 8.1x today. This future PE is greater than the current PE for the GB Banks industry at 3.7x.

- Analysts expect the number of shares outstanding to remain consistent over the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 44.89%, as per the Simply Wall St company report.

United Bank Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- UBL has successfully implemented a strategic shift towards being an employee-centric bank, which has resulted in reduced staff turnover and increased customer satisfaction. This improved employee engagement and customer service could lead to revenue growth through enhanced customer loyalty and new client acquisition.

- The bank achieved a significant growth in low-cost current accounts both domestically and internationally, surpassing industry averages. Sustained growth in low-cost deposits can contribute to lower funding costs, improving net margins and bolstering profitability.

- UBL has strategically realigned its international investment portfolio towards investment-grade bonds. This shift enhances the stability of earnings and reduces risk, thereby potentially supporting consistent earnings growth in its international operations.

- The bank hedged its interest rate risk by investing in long-term fixed-rate treasury bonds, which can protect its earnings against interest rate fluctuations, providing a stable earnings outlook for 2025 and 2026.

- UBL has managed to reward its shareholders with the highest dividends in the country while maintaining strong growth. This dual achievement indicates a resilient financial structure capable of sustaining high earnings and shareholder returns.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of PKR325.15 for United Bank based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of PKR389.9, and the most bearish reporting a price target of just PKR231.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be PKR119.6 billion, earnings will come to PKR41.5 billion, and it would be trading on a PE ratio of 29.2x, assuming you use a discount rate of 44.9%.

- Given the current share price of PKR410.79, the analyst price target of PKR325.15 is 26.3% lower. Despite analysts expecting the underlying buisness to improve, they seem to believe the market's expectations are too high.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on United Bank?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.