Catalysts

About KPIT Technologies

KPIT Technologies focuses on software solutions and engineering services for global automotive and mobility companies.

What are the underlying business or industry changes driving this perspective?

- While KPIT is pushing a solutions led model that can raise revenue per employee and fixed price mix, the transition away from traditional services relies on OEMs steadily adopting these offerings over the next 12 to 18 months. Any hesitation in uptake could temper revenue growth and delay margin benefits.

- Although management is investing heavily in AI based offerings, including triaging tools and development life cycle solutions that have already been piloted with clients, broad based adoption depends on OEMs being ready to embed AI into safety critical workflows. This could cap near term earnings contribution if internal validation cycles stay lengthy.

- Even as connected car features like phone as a key and complex digital cockpits create more software content per vehicle, OEM efforts to cut vehicle costs and reprioritise programs can shift or defer spending. This may limit the pace at which KPIT converts its validated solutions into sustained revenue growth.

- Despite new relationships such as the Microsoft AI partnership, a CRM platform tie up for agentic solutions, and wins with Chinese OEMs and micro mobility players, OEM budgets in core passenger car programs have already seen material pressure. Incremental deal flow from these areas might only partly offset headwinds to overall revenue momentum.

- While off highway, commercial vehicles and India or Southeast Asia and Middle East are highlighted as areas with healthier discussions and support from the Caresoft acquisition, integration complexity and ramp up timelines mean the impact on consolidated margins and earnings could build only gradually rather than providing an immediate uplift.

Assumptions

This narrative explores a more pessimistic perspective on KPIT Technologies compared to the consensus, based on a Fair Value that aligns with the bearish cohort of analysts. How have these above catalysts been quantified?

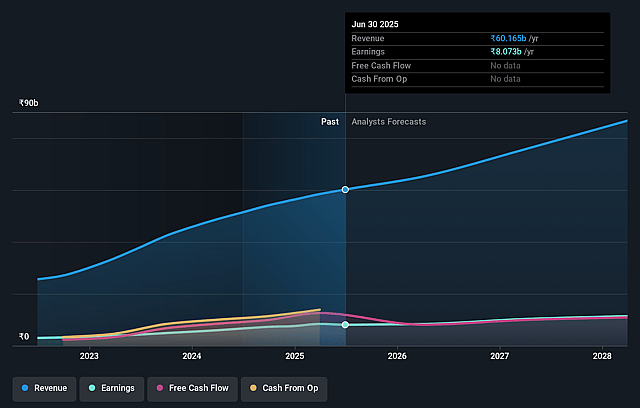

- The bearish analysts are assuming KPIT Technologies's revenue will grow by 9.8% annually over the next 3 years.

- The bearish analysts assume that profit margins will increase from 11.5% today to 12.7% in 3 years time.

- The bearish analysts expect earnings to reach ₹10.6 billion (and earnings per share of ₹38.43) by about February 2029, up from ₹7.2 billion today. However, there is some disagreement amongst the analysts with the more bullish ones expecting earnings as high as ₹14.3 billion.

- In order for the above numbers to justify the price target of the more bearish analyst cohort, the company would need to trade at a PE ratio of 37.7x on those 2029 earnings, up from 37.1x today. This future PE is greater than the current PE for the IN Software industry at 32.9x.

- The bearish analysts expect the number of shares outstanding to grow by 0.25% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 15.22%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?

- The pivot from a service led model to higher value solutions, including AI infused offerings and pre built platforms for features like digital cockpits and phone as a key, is aimed at higher revenue per employee and a larger wallet share at key OEMs. If this is successfully scaled across clients over the next few years, it could support stronger revenue and earnings growth than a flat share price view assumes and directly lift both topline and operating margins.

- OEMs are actively reprioritising spend toward areas where KPIT is already deeply involved, such as digital cockpit, cybersecurity, navigation on autopilot, multiple powertrains and cost reduction via the Caresoft acquisition. If these priorities translate into sustained deal flow across U.S., Europe, India, China and off highway or commercial programs, long term revenue and earnings could trend higher than implied by a stagnant share price expectation.

- KPIT is hearing consistently positive discussions across several regions and is adding senior leadership in AI, architecture and geo focused sales to handle more complex, higher ticket solution deals. If this expanded capability helps the company gain market share as OEMs consolidate vendors and move more work offshore to India, that could support higher revenue growth and improved net margins over time.

- Management highlights growing traction in adjacencies such as micro mobility, India and Southeast Asia, Middle East and off highway or commercial vehicles, as well as repeat wins with Chinese OEMs. If these segments scale meaningfully while large programs like the Caresoft enabled offerings ramp, they could offset current headwinds in parts of Asia and support higher consolidated earnings and cash generation.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The assumed bearish price target for KPIT Technologies is ₹950.0, which represents up to two standard deviations below the consensus price target of ₹1237.3. This valuation is based on what can be assumed as the expectations of KPIT Technologies's future earnings growth, profit margins and other risk factors from analysts on the more bearish end of the spectrum.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of ₹1550.0, and the most bearish reporting a price target of just ₹950.0.

- In order for you to agree with the more bearish analyst cohort, you'd need to believe that by 2029, revenues will be ₹83.1 billion, earnings will come to ₹10.6 billion, and it would be trading on a PE ratio of 37.7x, assuming you use a discount rate of 15.2%.

- Given the current share price of ₹981.4, the analyst price target of ₹950.0 is 3.3% lower. The relatively low difference between the current share price and the analyst consensus price target indicates that they believe on average, the company is fairly priced.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on KPIT Technologies?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystLowTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystLowTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystLowTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.