Last Update 19 Jun 26

KPITTECH: Dividend Plan And Cybersecurity Stake Will Drive Bullish Outlook

Analysts have kept their price target for KPIT Technologies steady at about ₹838 per share, citing largely unchanged assumptions around the discount rate, revenue growth, profit margin and future P/E expectations.

What’s in the News for KPIT Technologies

- A board meeting is scheduled on May 06, 2026 at 09:15 Indian Standard Time to consider and approve audited financial results for the quarter and year ended March 31, 2026.

- On the same May 06, 2026 agenda, the KPIT Technologies board will consider a final dividend for the 2025-26 financial year, if any, subject to shareholder approval at the ensuing annual general meeting. Source: Key Developments

- The May 06, 2026 board meeting will also consider acquisition of a stake in Cymotive Technologies Ltd, an automotive cybersecurity specialist headquartered in Israel, as part of a proposed strategic investment. Source: Key Developments

- A separate board meeting held on April 28, 2026 considered and approved a grant of 21,000 options to eligible employees under the KPIT Technologies Limited Restricted Stock Unit Plan 2022, previously approved by shareholders on August 24, 2022. Source: Key Developments

Valuation Changes for KPIT Technologies

- Fair Value: Estimated fair value remains unchanged at about ₹838 per share. This indicates no revision to the central valuation level.

- Discount Rate: The discount rate has risen slightly from 14.89% to 14.99%. This reflects a marginally higher required return applied in the valuation.

- Revenue Growth: The assumed revenue growth rate is effectively unchanged at around 11.17%, with only a negligible numerical adjustment.

- Net Profit Margin: The projected profit margin remains essentially flat at about 13.55%, indicating no material shift in profitability assumptions.

- Future P/E: The future P/E multiple has risen slightly from 28.78x to 28.86x. This implies a marginally higher valuation multiple applied to KPIT Technologies earnings.

Key Takeaways

- Expansion in software-defined vehicles, embedded cybersecurity, and next-gen mobility drives demand for KPIT's engineering services, reinforcing margins and future earnings resilience.

- Proprietary technology and solutions-led models boost operational efficiency and diversification, leveraging global outsourcing trends and deepening relationships with leading automotive OEMs.

- Heavy reliance on European clients, slower conversion of wins, and delayed tech commercialization raise concerns over revenue growth, margin pressures, and execution risks in emerging markets.

Catalysts

About KPIT Technologies- Provides embedded software, artificial intelligence, and digital solutions for the automobile and mobility sector in the Americas, the United Kingdom, Europe, and internationally.

- Imminent recovery in client automotive spending post-tariff/regulatory uncertainty is expected to unlock stalled programs-especially in Europe, China, and India-where KPIT's pipeline is robust and large programs are ready to ramp, setting up for stronger revenue growth in the second half and across FY27.

- Rising industry focus on software-defined vehicles (SDVs), connected/e-cockpit solutions, and embedded cybersecurity is pushing OEMs to accelerate feature rollouts and compliance initiatives, directly increasing demand for KPIT's high-value software engineering and validation services-supporting higher realization rates and net margin resilience.

- Increased use and development of proprietary tools, accelerators, and AI-infused mobility solutions allow KPIT to address client cost and speed pressures more efficiently, shifting work toward fixed-price and solutions-led models, which can improve operating leverage and buttress EBITDA margins despite wage inflation.

- Strong traction and strategic foothold in fast-growing EV and next-gen mobility markets (India and China), including multi-year platforms with leading OEMs, are expected to diversify KPIT's revenue base beyond mature Western markets and drive higher long-term earnings visibility.

- Sustained global trend of outsourcing R&D and software integration by automotive OEMs, as platform complexity and software content in vehicles surges, continues to benefit KPIT's order book and future annuity streams, positioning revenue and margin upside as the industry transitions intensify.

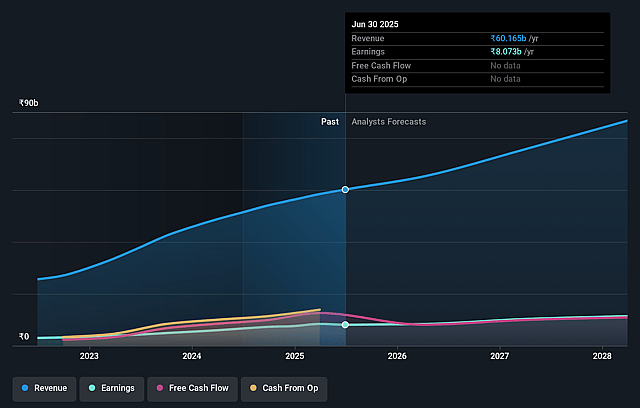

KPIT Technologies Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

- Analysts are assuming KPIT Technologies's revenue will grow by 11.2% annually over the next 3 years.

- Analysts assume that profit margins will increase from 9.9% today to 13.5% in 3 years time.

- Analysts expect earnings to reach ₹12.0 billion (and earnings per share of ₹43.53) by about June 2029, up from ₹6.4 billion today. However, there is some disagreement amongst the analysts with the more bullish ones expecting earnings as high as ₹14.4 billion.

- In order for the above numbers to justify the price target of the analysts, the company would need to trade at a PE ratio of 29.0x on those 2029 earnings, down from 31.9x today. This future PE is lower than the current PE for the IN Software industry at 30.9x.

- Analysts expect the number of shares outstanding to grow by 0.09% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 14.99%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- Ongoing reprioritization and delay of OEM automotive programs, particularly in EV and new software architectures, signal slower client spending and reduced near-term conversion of deal wins into revenue, raising concerns over future topline growth.

- Rising cannibalization from KPIT's own solutions and accelerators (faster, AI-based project delivery), though improving margins and client stickiness, may substitute previous labor-intensive revenue streams and dilute overall revenue growth despite strong deal wins.

- Overdependence on the European market and a limited client set is evident; ongoing profit downgrades and margin pressures at major European OEMs could lead to client spend reductions, exposing KPIT to revenue volatility and slower earnings growth.

- Delay in the commercialization of high-potential technologies such as sodium-ion batteries and hydrogen fuel, with management admitting revenue impact is 2–3 years out and current involvement limited to pilots, risks missing shorter-term monetization opportunities and pushes out prospective earnings.

- Expansion in China and India is in early stages, and while management is optimistic, uncertainties around local competition, pricing, currency volatility, and the complexity of scaling platforms/products in these markets could impeded margin expansion and result in operational execution risk that impacts net profitability.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The analysts have a consensus price target of ₹838.29 for KPIT Technologies based on their expectations of its future earnings growth, profit margins and other risk factors.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of ₹1030.0, and the most bearish reporting a price target of just ₹670.0.

- In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be ₹88.7 billion, earnings will come to ₹12.0 billion, and it would be trading on a PE ratio of 29.0x, assuming you use a discount rate of 15.0%.

- Given the current share price of ₹745.95, the analyst price target of ₹838.29 is 11.0% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on KPIT Technologies?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.