Key Takeaways

- Regulatory hurdles and increasing privacy concerns could drastically shrink addressable markets, threatening international growth and future revenue streams.

- Heavy reliance on government contracts and intensifying competition expose ideaForge to earnings volatility, margin pressure, and rapid product obsolescence.

- Growing focus on defense automation, innovative UAV offerings, and global expansion supports diversified revenue streams, higher margins, and long-term profitability for ideaForge.

Catalysts

About ideaForge Technology- Engages in the manufacture and marketing of unmanned aerial vehicle (UAV) systems for security and surveillance applications in India and internationally.

- Heightened regulatory scrutiny and evolving international export controls on military drones could sharply curtail ideaForge's access to large overseas markets, significantly limiting potential revenue growth from international expansion.

- Intensifying public and political backlash against aerial surveillance and data privacy in both developed and developing economies could lead to stricter domestic and global restrictions on drone deployments, reducing long-term addressable markets and severely impacting future revenue streams.

- Reliance on Indian defense procurement and government contracts leaves the company highly exposed to order volatility, delays, and unpredictable budget cycles, resulting in substantial swings in topline revenue and ongoing uncertainty in earnings visibility.

- Increasing global competition from advanced drone manufacturers, along with rapid innovation cycles from both international and domestic rivals, raises the risk of faster product obsolescence for ideaForge's current platforms, leading to potential margin compression and lower net earnings over time.

- The accelerating pace of adoption for alternative autonomous surveillance and intelligence-gathering technologies, such as AI-driven satellites and edge computing IoT systems, threatens to erode long-term demand for traditional UAV hardware, putting sustained pressure on ideaForge's future revenue growth and profitability.

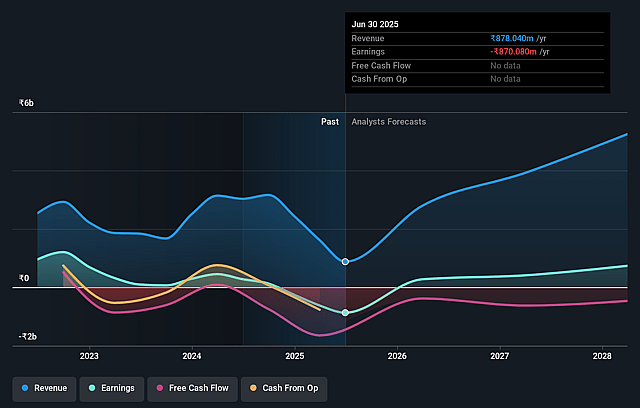

ideaForge Technology Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- This narrative explores a more pessimistic perspective on ideaForge Technology compared to the consensus, based on a Fair Value that aligns with the bearish cohort of analysts.

- The bearish analysts are assuming ideaForge Technology's revenue will grow by 91.3% annually over the next 3 years.

- The bearish analysts assume that profit margins will increase from -99.1% today to 15.8% in 3 years time.

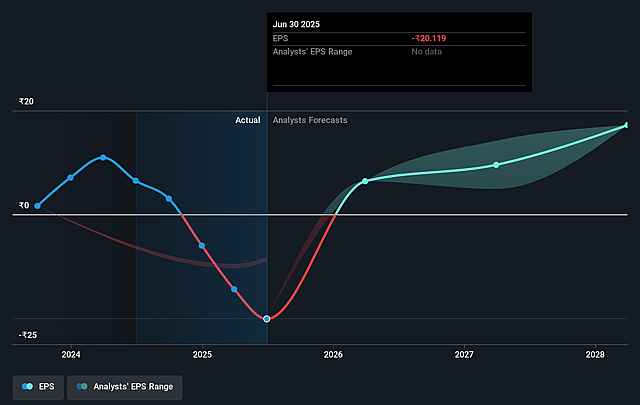

- The bearish analysts expect earnings to reach ₹970.7 million (and earnings per share of ₹22.65) by about September 2028, up from ₹-870.1 million today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the price target of the more bearish analyst cohort, the company would need to trade at a PE ratio of 18.2x on those 2028 earnings, up from -25.7x today. This future PE is lower than the current PE for the IN Aerospace & Defense industry at 54.8x.

- Analysts expect the number of shares outstanding to grow by 1.04% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 14.03%, as per the Simply Wall St company report.

ideaForge Technology Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- Sustained government focus on indigenous defense procurement and emergency allocations, as evidenced by significant and recurring budgetary commitments for high-tech drone acquisitions, could drive robust long-term revenue growth for ideaForge.

- The company's strong track record in developing and rapidly commercializing innovative, EW-resilient UAV platforms ahead of market demand positions it as a leader, which may support higher margins and enhance earnings quality over time.

- Successful expansion into international markets, including early adoption programs in the United States, new opportunities in Africa, and potential European partnerships, may diversify revenue streams and reduce reliance on Indian defense contracts, potentially resulting in greater earnings stability.

- The build-out of proprietary software, AI features, and Drone as a Service offerings introduces the possibility of growing recurring revenue and improving operating leverage, which could strengthen net margins and lift long-term profitability.

- Deep engagement in critical, large-scale national initiatives such as smart city surveillance, border security, and geospatial mapping, along with a robust pipeline of ₹400 crore (excluding emergency procurements) suggests healthy order inflows and future topline growth, contradicting expectations of declining share prices.

Valuation

How have all the factors above been brought together to estimate a fair value?- The assumed bearish price target for ideaForge Technology is ₹271.0, which represents the lowest price target estimate amongst analysts. This valuation is based on what can be assumed as the expectations of ideaForge Technology's future earnings growth, profit margins and other risk factors from analysts on the more bearish end of the spectrum.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of ₹500.0, and the most bearish reporting a price target of just ₹271.0.

- In order for you to agree with the bearish analysts, you'd need to believe that by 2028, revenues will be ₹6.1 billion, earnings will come to ₹970.7 million, and it would be trading on a PE ratio of 18.2x, assuming you use a discount rate of 14.0%.

- Given the current share price of ₹516.95, the bearish analyst price target of ₹271.0 is 90.8% lower. Despite analysts expecting the underlying buisness to improve, they seem to believe the market's expectations are too high.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

AnalystLowTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystLowTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystLowTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.