Key Takeaways

- YouGov's platform expansion and automation are set to accelerate operating leverage, margin expansion, and recurring revenues beyond current analyst expectations.

- Enhanced data integration and privacy compliance uniquely position YouGov to win major enterprise contracts, driving revenue acceleration and strengthening long-term client relationships.

- Regulatory shifts, tech disruption, rising costs, and expansion hurdles threaten YouGov's data quality, margin stability, and ability to compete or grow revenue internationally.

Catalysts

About YouGov- Provides online market research services in the United Kingdom, the Americas, the Middle East, Mainland Europe, Africa, and the Asia Pacific.

- Analyst consensus expects margin improvement from the cost optimization plan totaling 20 million pounds of savings, but this likely understates the upside, as YouGov's move toward a true platform business model and intensified automation could drive sustained operating leverage, accelerating margin expansion beyond historic highs and meaningfully boosting earnings power.

- Analysts broadly agree on future growth from the SP3 refocus and AI-driven product improvements, but this likely still underappreciates YouGov's ability to become the dominant provider of high-quality, privacy-compliant first-party data globally as third-party cookies vanish-creating the potential for YouGov's recurring data subscription revenues to sharply outpace expectations.

- The integration of behavioral and passive data-including banking, shopping and viewing data-into the core platform alongside traditional survey data uniquely positions YouGov to capture incremental wallet share across major brand, retail and digital clients, driving revenue acceleration as marketing budgets prioritize real-time, holistic consumer insight.

- YouGov's scalable, trusted panel infrastructure-coupled with ongoing advances in user experience and UI-makes it the go-to partner for global advertisers racing to adapt to stricter privacy regimes, allowing for premium pricing and sticky, multi-year contracts that underpin robust revenue visibility and margin resilience.

- As global media, advertising, and corporate clients consolidate vendor relationships, YouGov's universal connected data platform is set to win disproportionately large enterprise contracts, driving step-changes in top-line growth and elevating cash conversion and free cash flow generation over the next several years.

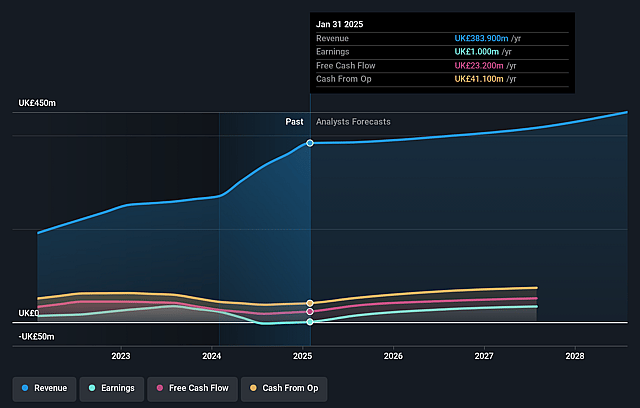

YouGov Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- This narrative explores a more optimistic perspective on YouGov compared to the consensus, based on a Fair Value that aligns with the bullish cohort of analysts.

- The bullish analysts are assuming YouGov's revenue will grow by 5.5% annually over the next 3 years.

- The bullish analysts assume that profit margins will increase from 0.3% today to 14.5% in 3 years time.

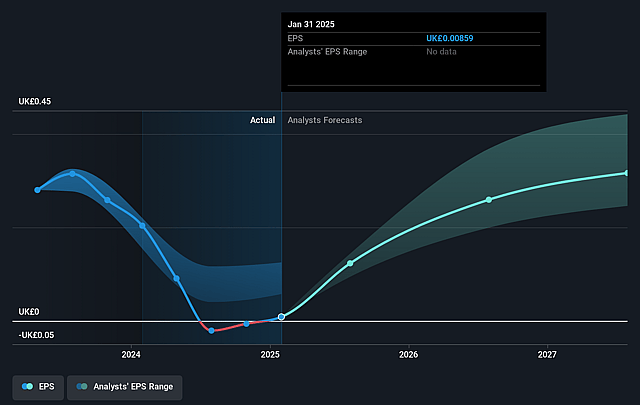

- The bullish analysts expect earnings to reach £65.3 million (and earnings per share of £0.78) by about September 2028, up from £1.0 million today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the price target of the more bullish analyst cohort, the company would need to trade at a PE ratio of 17.3x on those 2028 earnings, down from 410.8x today. This future PE is greater than the current PE for the GB Media industry at 12.1x.

- Analysts expect the number of shares outstanding to grow by 0.77% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 7.78%, as per the Simply Wall St company report.

YouGov Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- Ongoing and upcoming regulatory changes, such as data privacy laws and heightened consumer concerns about personal data, pose a significant risk to YouGov's ability to collect and utilize high-quality data from its panels, potentially reducing future revenue if these trends limit data scope or participation.

- The company's significant reliance on its proprietary panels risks sample bias and falling representativeness, especially as there are indications of panel recruitment and retention challenges and growing consumer reluctance to participate, which could erode client trust and directly impact top-line sales over the longer term.

- The market research sector is facing secular pressure from the proliferation of AI and automation, which commoditize traditional survey products; despite YouGov's AI investments, the company admitted important tools arrived late and execution slipped, increasing the threat of margin compression and lost market share if innovation lags competitors, ultimately weighing on net margins and earnings growth.

- Rising costs for technology infrastructure and personnel, as evidenced by higher staff costs, increased research admin expenses, and substantial ongoing investment in panels and tech, may result in sustained pressure on operating leverage and net margins, especially as cost savings measures are only partially realized and are offset by new investments.

- Failure to deliver rapid and effective international expansion-underscored by slow CPS integration and limited presence in major markets like the US-could leave YouGov exposed to regional shocks and prevent it from diversifying revenues, constraining the company's long-term earnings growth and making it vulnerable to competition from larger tech players and evolving client data strategies.

Valuation

How have all the factors above been brought together to estimate a fair value?- The assumed bullish price target for YouGov is £7.6, which is the highest price target estimate amongst analysts. This valuation is based on what can be assumed as the expectations of YouGov's future earnings growth, profit margins and other risk factors from analysts on the bullish end of the spectrum.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of £7.6, and the most bearish reporting a price target of just £3.4.

- In order for you to agree with the bullish analysts, you'd need to believe that by 2028, revenues will be £451.2 million, earnings will come to £65.3 million, and it would be trading on a PE ratio of 17.3x, assuming you use a discount rate of 7.8%.

- Given the current share price of £3.5, the bullish analyst price target of £7.6 is 53.9% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

AnalystHighTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystHighTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystHighTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.