Key Takeaways

- Intensifying regulation, survey fatigue, and AI-driven authenticity issues threaten YouGov's data quality, undermining its differentiation and long-term revenue prospects.

- Growing competition, rising panelist costs, and client budget shifts are set to erode profitability and constrain international expansion.

- Investments in technology, strategic expansion, and strong client retention position YouGov for resilient growth, margin improvement, and reduced financial risk amid favorable industry trends.

Catalysts

About YouGov- Provides online market research services in the United Kingdom, the Americas, the Middle East, Mainland Europe, Africa, and the Asia Pacific.

- Escalating global privacy regulations and tightening data-collection laws threaten YouGov's ability to maintain access to high-quality, representative consumer data. This significantly undermines the future value of its proprietary panel and could reduce both revenue growth and net margins over the long-term.

- Persistent and growing survey fatigue, combined with public skepticism and reduced willingness to participate in online research, poses a material risk to YouGov's core data-collection model. As response rates and sample quality erode, the company's products lose reliability and competitive differentiation, diminishing its earnings trajectory and compressing margins.

- The rise of synthetic and generative AI content is likely to further contaminate online surveys and opinion panels, making it increasingly difficult for YouGov to guarantee authenticity and accuracy. As the industry moves away from human-based panels to alternative data sources, YouGov's historical advantage in panel-based insights will deteriorate, causing long-term headwinds for revenue and recurring income.

- Increased competition from low-cost, automated survey tools and big data analytics platforms will accelerate commoditization of YouGov's traditional offerings. As clients shift budgets toward first-party data initiatives and in-house analytics solutions, YouGov will face mounting pressure on pricing power and client retention, driving down future profitability.

- Rising costs to recruit and retain quality panelists, fueled by higher incentive demands and competition for digital engagement, will directly erode net margins even as revenue growth stalls. This margin compression is likely to be exacerbated by challenges in scaling internationally, particularly outside of English-speaking regions, limiting the company's global earnings potential for the foreseeable future.

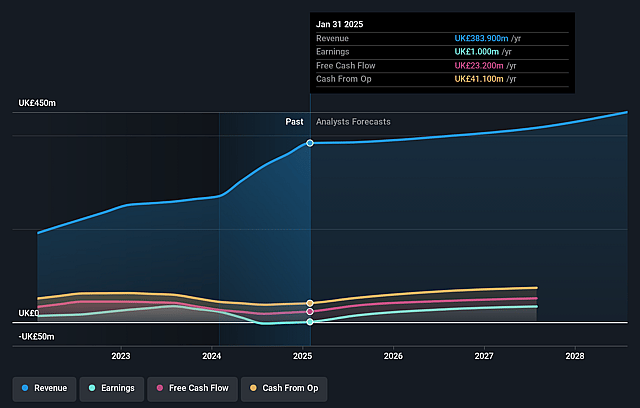

YouGov Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- This narrative explores a more pessimistic perspective on YouGov compared to the consensus, based on a Fair Value that aligns with the bearish cohort of analysts.

- The bearish analysts are assuming YouGov's revenue will grow by 5.5% annually over the next 3 years.

- The bearish analysts assume that profit margins will increase from 0.3% today to 11.4% in 3 years time.

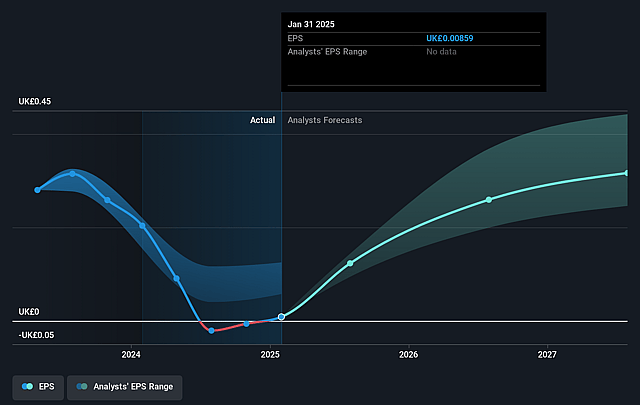

- The bearish analysts expect earnings to reach £51.4 million (and earnings per share of £0.43) by about August 2028, up from £1.0 million today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the price target of the more bearish analyst cohort, the company would need to trade at a PE ratio of 9.9x on those 2028 earnings, down from 401.7x today. This future PE is lower than the current PE for the GB Media industry at 12.8x.

- Analysts expect the number of shares outstanding to grow by 0.77% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 7.82%, as per the Simply Wall St company report.

YouGov Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- YouGov's renewed strategic focus on its data platform (SP3 vision), combined with investment in AI, automation, and dedicated sales teams for data products, positions the company to potentially return to historical levels of revenue growth and higher recurring margins over the long term.

- Expanding proprietary panels and integrating CPS's expertise, especially into new geographies such as the U.S. and Nordics, enables YouGov to scale its high-margin syndicated data offerings and diversify its revenue streams, supporting both top-line and earnings growth.

- The company's strong operational cash generation-including improvements in cash conversion as post-acquisition integrations of CPS are finalized and as data products become a larger share of business-improves its ability to reinvest in technology while managing debt, benefitting future net income and reducing financial risk.

- YouGov's high renewal rates (over 80% of clients renewing, with this figure recovering to historical norms) combined with sector growth in areas like technology, banking, and academia, provide resilience and recurring revenue visibility even through periods of macroeconomic uncertainty.

- Industry-wide secular trends-such as increasing digitalization, demand for real-time, ethical first-party data, and greater global need for trusted consumer insights-align well with YouGov's platform-based model, which could drive long-term expansion of its addressable market and support higher revenues and profit margins.

Valuation

How have all the factors above been brought together to estimate a fair value?- The assumed bearish price target for YouGov is £3.4, which represents the lowest price target estimate amongst analysts. This valuation is based on what can be assumed as the expectations of YouGov's future earnings growth, profit margins and other risk factors from analysts on the more bearish end of the spectrum.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of £7.6, and the most bearish reporting a price target of just £3.4.

- In order for you to agree with the bearish analysts, you'd need to believe that by 2028, revenues will be £450.5 million, earnings will come to £51.4 million, and it would be trading on a PE ratio of 9.9x, assuming you use a discount rate of 7.8%.

- Given the current share price of £3.43, the bearish analyst price target of £3.4 is 0.9% lower. The relatively low difference between the current share price and the analyst bearish price target indicates that they believe on average, the company is fairly priced.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on YouGov?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystLowTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystLowTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystLowTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.