Key Takeaways

- Initiatives like Project Vista and the new China plant aim to improve sales strategies and expand geographically, enhancing margins and growth potential.

- Magma mega-programme and Medical segment recovery are set to drive long-term volume increases and enhance revenue and margins.

- Operational challenges, pricing pressures, and currency impacts could hinder Victrex's earnings, while reliance on medical and auto markets adds further risks.

Catalysts

About Victrex- Through its subsidiaries, engages in the manufacture and sale of polymer solutions worldwide.

- Victrex has implemented self-help and improvement actions, including cost actions and Project Vista, to enhance go-to-market strategies, which are expected to improve sales effectiveness and operational efficiencies. This is likely to positively impact net margins and earnings.

- The completion of Victrex's new plant in China is seen as a strategic opportunity to support geographic expansion and underpin growth in key sectors such as VAR, Auto, and Electronics. Once initial operational challenges are addressed, this could lead to significant revenue growth.

- The Magma mega-programme has reached major commercial milestones, paving the way for future growth opportunities. This programme is expected to contribute considerable long-term volume increases and enhance overall revenue.

- Expectation of recovery in the Medical segment, particularly in the Spine area, along with continued growth in non-Spine applications, is anticipated to result in improved sales mix and a positive impact on gross margins.

- Strong volume momentum is being observed, supported by post-destocking normalization in several end markets and improvements from Project Vista, suggesting potential for revenue growth and better asset utilization rates which could enhance overall earnings.

Victrex Future Earnings and Revenue Growth

Assumptions

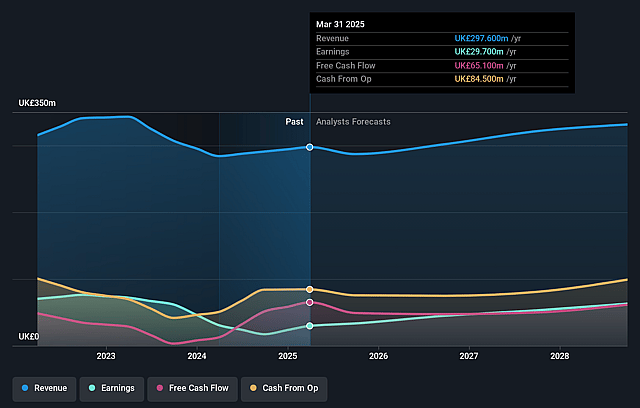

How have these above catalysts been quantified?- Analysts are assuming Victrex's revenue will grow by 3.4% annually over the next 3 years.

- Analysts assume that profit margins will increase from 10.0% today to 18.2% in 3 years time.

- Analysts expect earnings to reach £60.1 million (and earnings per share of £0.69) by about September 2028, up from £29.7 million today. However, there is some disagreement amongst the analysts with the more bearish ones expecting earnings as low as £45 million.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 15.8x on those 2028 earnings, down from 20.7x today. This future PE is lower than the current PE for the GB Chemicals industry at 22.1x.

- Analysts expect the number of shares outstanding to remain consistent over the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 7.56%, as per the Simply Wall St company report.

Victrex Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- Initial start-up operational challenges at the new plant in China and the resulting lower-than-expected production volumes could weigh on overall production efficiency, thus impacting net margins.

- The ASP (average selling price) decline driven by mix, specifically increased volume in low-priced applications like VARs, can put downward pressure on earnings despite higher sales volumes.

- Continued currency headwinds, especially the impact of a stronger Sterling, are expected to have a negative effect on revenue and profits, creating earnings volatility.

- The uncertainty faced in the Automotive sector, notably in Western markets and potential tariff impacts, could lead to reduced demand and revenue pressures.

- The heavy reliance on medical device markets for growth, with ongoing destocking cycles and pricing pressures due to VBP in China, poses risks to achieving projected revenue and maintaining profitability.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of £8.768 for Victrex based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of £11.0, and the most bearish reporting a price target of just £6.75.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be £329.2 million, earnings will come to £60.1 million, and it would be trading on a PE ratio of 15.8x, assuming you use a discount rate of 7.6%.

- Given the current share price of £7.08, the analyst price target of £8.77 is 19.3% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.