Key Takeaways

- Technology-driven efficiencies, new leadership, and recurring pension surplus are set to drive stronger margins, capital generation, and shareholder returns far beyond current market expectations.

- Diversified growth in subscription-based digital investing, private markets, and global wealth solutions positions Aberdeen for robust, long-term earnings and competitive advantages across core markets.

- Ongoing industry and structural headwinds are pressuring Aberdeen's revenues, margins, and growth prospects, while cost-cutting and technology investments face significant execution risks.

Catalysts

About Aberdeen Group- Provides asset management services in the United Kingdom, Europe, North America, and Asia.

- Analyst consensus sees the £150 million annualized cost savings as notable, but the transformation program's proven momentum, rapid tech-driven efficiencies (including automation and AI), and new leadership suggest the ultimate run-rate savings could exceed targets, delivering sustained improvements to net margins and capital generation well beyond 2025.

- While consensus highlights uncertainty around unlocking pension capital benefits, capital generation from Aberdeen Group's defined benefit pension surplus is structurally significant and designed to be recurring, positioning this as a lasting boost to capital generation and dividend cover, making both earnings and shareholder returns more resilient than the market expects.

- The interactive investor business is poised to outpace analyst growth models given its unique subscription model, fast gains in brand awareness, multiple product launches (including managed SIPP, digital advice, and ii360), and rising customer engagement-these dynamics can materially accelerate revenue and earnings growth, especially as it captures a disproportionate share of a rapidly expanding UK D2C market.

- Aberdeen's accelerated investment in private markets, alternatives, and ESG-focused real assets places the firm at the forefront of higher-growth, higher-fee market segments favored by global institutional and retail investors, promising step-changes in revenue quality, profitability, and long-term AUM growth.

- The group's integrated technology and streamlined operating model, underpinned by its scale, client data analytics, and regulatory harmonization, enables not just cross-divisional revenue synergies (e.g., in retirement solutions) but also access to emerging global wealth pools in Asia and beyond, driving sustained revenue expansion and competitive operating leverage over the coming decade.

Aberdeen Group Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- This narrative explores a more optimistic perspective on Aberdeen Group compared to the consensus, based on a Fair Value that aligns with the bullish cohort of analysts.

- The bullish analysts are assuming Aberdeen Group's revenue will grow by 1.1% annually over the next 3 years.

- The bullish analysts assume that profit margins will shrink from 17.3% today to 15.4% in 3 years time.

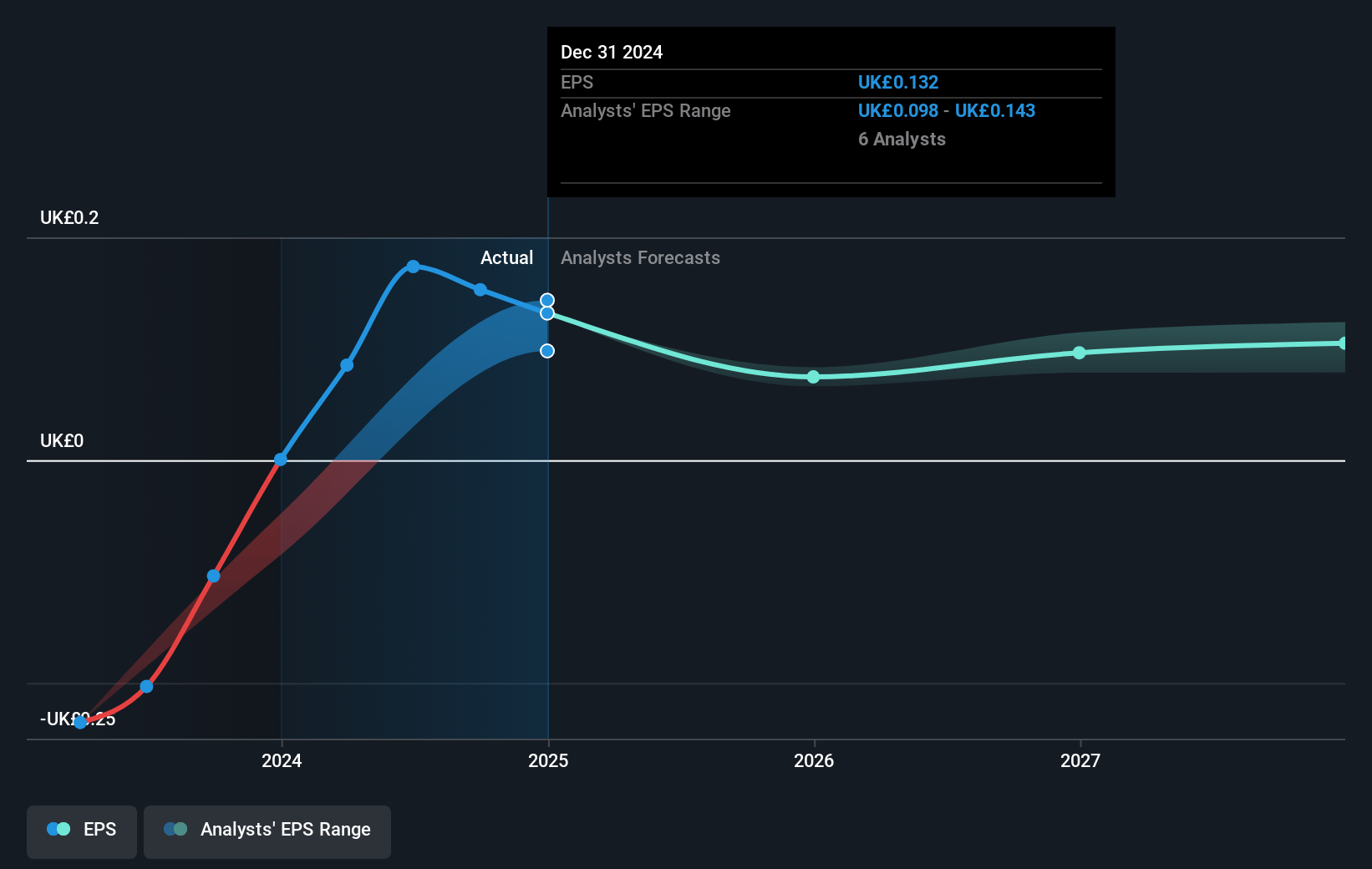

- The bullish analysts expect earnings to reach £218.8 million (and earnings per share of £0.11) by about July 2028, down from £237.0 million today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the price target of the more bullish analyst cohort, the company would need to trade at a PE ratio of 23.1x on those 2028 earnings, up from 14.5x today. This future PE is greater than the current PE for the GB Capital Markets industry at 13.0x.

- Analysts expect the number of shares outstanding to grow by 0.13% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 8.69%, as per the Simply Wall St company report.

Aberdeen Group Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The ongoing shift from active to passive investment strategies is placing pressure on active managers like Aberdeen Group, as evidenced by continuing industry-wide net outflows in high-margin equity products and the strategic shift towards alternatives and wholesale, which are higher growth but more competitive, potentially leading to ongoing revenue and margin compression that impacts overall recurring revenue and net margins.

- Management explicitly acknowledges continued contraction of revenue margins in its core Investments division, with expectations that margins will fall below 21 basis points in 2025, and little to no revenue growth anticipated, meaning profitability targets depend primarily on cost-cutting rather than top-line improvement, risking future operating profit growth if further cost efficiencies prove difficult to achieve.

- The Adviser business continues to experience net outflows (negative £3.9 billion in the latest year), and despite plans to return to £1 billion of inflows by 2026, this is a modest improvement relative to the asset base and does not restore the business to industry leadership, suggesting challenges in regaining market share and growing assets under management, which will limit future revenue growth.

- While Aberdeen is investing in digital transformation and launching new technology offerings, legacy systems and the slow pace of change in some areas, as well as the need for heavy reinvestment, create elevated operational expenses and could reduce long-term competitiveness versus both fintech entrants and larger asset managers with greater scale, ultimately pressuring net margins and earnings growth.

- The asset management industry is experiencing structural fee compression and heightened regulatory scrutiny, both highlighted by management as near-term headwinds; these trends are expected to increase compliance costs and erode pricing power for mid-sized players like Aberdeen, potentially leading to persistent downward pressure on revenue yields and group-level net margins.

Valuation

How have all the factors above been brought together to estimate a fair value?- The assumed bullish price target for Aberdeen Group is £2.2, which is the highest price target estimate amongst analysts. This valuation is based on what can be assumed as the expectations of Aberdeen Group's future earnings growth, profit margins and other risk factors from analysts on the bullish end of the spectrum.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of £2.2, and the most bearish reporting a price target of just £1.4.

- In order for you to agree with the bullish analysts, you'd need to believe that by 2028, revenues will be £1.4 billion, earnings will come to £218.8 million, and it would be trading on a PE ratio of 23.1x, assuming you use a discount rate of 8.7%.

- Given the current share price of £1.92, the bullish analyst price target of £2.2 is 12.6% higher. Despite analysts expecting the underlying buisness to decline, they seem to believe it's more valuable than what the market thinks.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

AnalystHighTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystHighTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystHighTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.