Last Update 21 Dec 25

Fair value Decreased 8.44%VNA: Future Profitability And Cost Controls May Support Share Price Upside

Analysts have modestly increased their price target on Vonovia to EUR 36 from EUR 35.50, reflecting slightly upgraded expectations for profitability despite lower fair value estimates and softer revenue growth assumptions.

Analyst Commentary

Recent research updates indicate that bullish analysts see the modest price target increase as a signal of improving risk reward, even as fundamental assumptions are adjusted more cautiously.

Bullish Takeaways

- Bullish analysts highlight the lift in the price target to EUR 36 as evidence that upside remains from current trading levels, supported by gradual progress on profitability.

- The reaffirmed Overweight stance is viewed as a vote of confidence in management execution on cost controls and portfolio optimization, which could drive margin expansion over time.

- Supporters argue that the current valuation still discounts the quality and scale of Vonovia's residential portfolio, leaving room for multiple expansion if earnings visibility continues to improve.

- The updated target, though only modestly higher, is seen as reflecting a more resilient earnings profile in a softer macro and rate environment than previously anticipated.

Bearish Takeaways

- Bearish analysts caution that the small magnitude of the target increase signals limited near term rerating potential, particularly if revenue growth stays muted.

- There is concern that lower fair value estimates for the property portfolio could cap upside, especially if transaction markets remain illiquid and repricing persists.

- Some remain wary that the pace of deleveraging and asset disposals may fall short of expectations, constraining financial flexibility and weighing on valuation multiples.

- Execution risk around managing operating costs and maintaining occupancy in a more regulated environment is seen as a key factor that could hinder delivery against the raised target.

Valuation Changes

- Fair Value decreased from €37.53 to €34.36, indicating a moderate downward revision to the underlying asset valuation.

- The Discount Rate rose slightly from 9.75 percent to 9.98 percent, reflecting a marginally higher required return and risk perception.

- Revenue Growth was lowered from minus 19.03 percent to minus 20.63 percent, pointing to a slightly more negative outlook for top line development.

- Net Profit Margin increased from 85.25 percent to 91.65 percent, suggesting expectations for stronger profitability despite weaker revenue assumptions.

- Future P/E edged down from 12.20x to 11.90x, implying a modestly lower earnings multiple embedded in the updated valuation.

Key Takeaways

- Vonovia aims to boost non-rental EBITDA with less capital-intensive service expansion, enhancing earnings and ensuring stability.

- Increased investment and focus on cash generation are expected to drive EBITDA growth, protect the balance sheet, and improve net margins.

- Rising financing costs and economic uncertainty threaten Vonovia's earnings, margins, and growth, with capital-light strategies and high cash taxes also impacting performance.

Catalysts

About Vonovia- Operates as an integrated residential real estate company in Europe.

- Vonovia plans to accelerate its non-rental EBITDA growth by expanding its service business in a less capital-intensive manner, which is expected to positively impact overall earnings.

- The company aims for a 4% CAGR in adjusted EBITDA rental driven by increased investment, potentially boosting the revenue and contributing to stable rental income growth.

- A planned increase in non-rental EBITDA by 30% by 2028, supported by initiatives like serial modernization and photovoltaic projects, could significantly enhance earnings.

- The cessation of value decline in property prices and a prediction of stable or increasing transaction volumes suggest future revenue stability and potential appreciation in asset values.

- Vonovia’s approach to prioritize cash generation and maintain financial stability, including successful completions of the disposal program at or above book value, is expected to positively impact net margins and protect the balance sheet.

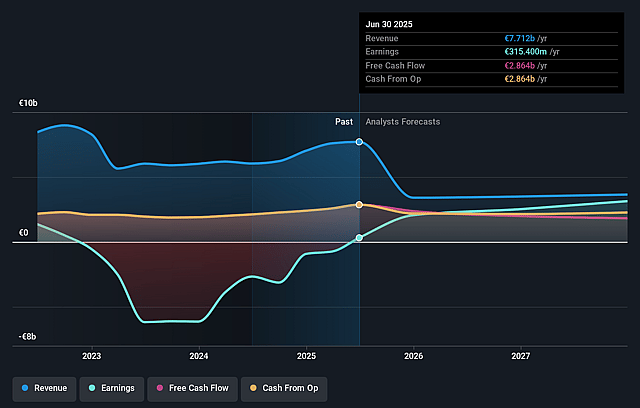

Vonovia Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Vonovia's revenue will decrease by 19.0% annually over the next 3 years.

- Analysts assume that profit margins will increase from -13.1% today to 85.3% in 3 years time.

- Analysts expect earnings to reach €3.2 billion (and earnings per share of €3.22) by about May 2028, up from €-922.7 million today. However, there is a considerable amount of disagreement amongst the analysts with the most bullish expecting €4.2 billion in earnings, and the most bearish expecting €2.4 billion.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 12.2x on those 2028 earnings, up from -26.1x today. This future PE is lower than the current PE for the GB Real Estate industry at 20.2x.

- Analysts expect the number of shares outstanding to grow by 1.01% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 9.75%, as per the Simply Wall St company report.

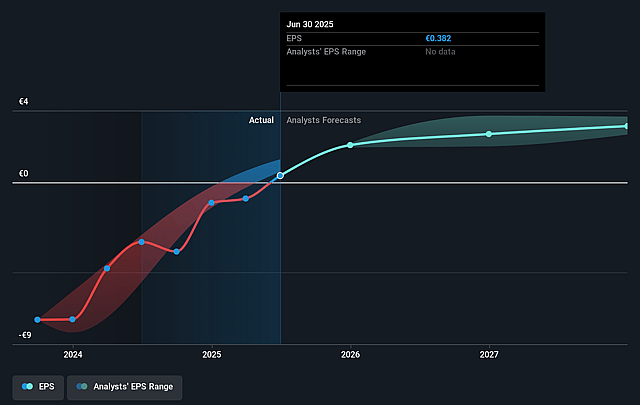

Vonovia Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- Increasing bond yields and uncertainty around German bond issuance could lead to higher financing costs and impact property values, affecting Vonovia’s overall earnings and net margins.

- The changes in interest rates due to geopolitical events have increased Vonovia's cost of capital, creating challenges in maintaining financial stability and potentially impacting net margins.

- Economic implications from the German government's planned military and infrastructure investments introduce uncertainty, with possible effects on revenue and the company's ability to finance and execute growth initiatives.

- Execution timing uncertainties for nonrental growth initiatives and priority shifts towards capital-light strategies may affect the company's revenue-generating capabilities and projected earnings growth.

- High cash taxes associated with disposals and increasing refinancing costs could suppress free cash flow, impacting Vonovia's ability to invest in growth initiatives and maintain profit margins.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of €34.653 for Vonovia based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of €52.8, and the most bearish reporting a price target of just €24.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be €3.7 billion, earnings will come to €3.2 billion, and it would be trading on a PE ratio of 12.2x, assuming you use a discount rate of 9.8%.

- Given the current share price of €29.24, the analyst price target of €34.65 is 15.6% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Vonovia?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.