Last Update 27 Nov 25

Fair value Increased 8.71%PAT: Outlook Will Improve With Rising Fair Value And Moderate Profitability

Analysts have raised their price target for PATRIZIA from €9.36 to €10.18, citing adjustments in projected growth rates and updated expectations for profitability.

Valuation Changes

- Fair Value: Increased from €9.36 to €10.18, reflecting a modest upward adjustment.

- Discount Rate: Increased slightly from 7.29% to 7.64%.

- Revenue Growth: Reduced significantly from 6.37% to 4.34%.

- Net Profit Margin: Decreased marginally from 6.89% to 6.44%.

- Future P/E: Increased sharply from 47.86x to 83.03x.

Key Takeaways

- Stabilizing real estate values and growing investor confidence are set to drive higher AUM, recurring fees, and improved margin performance.

- Strong demand for infrastructure and living assets, alongside global client diversification, is fueling sustainable growth and greater operating efficiency.

- Heavy reliance on cost discipline amid stagnant growth, market volatility, and sector headwinds leaves future margins and revenue outlook vulnerable if conditions fail to improve.

Catalysts

About PATRIZIA- With operations around the world, PATRIZIA has been offering investment opportunities in real estate and infrastructure assets for institutional, semi-professional and private investors for 41 years.

- The stabilization of real estate valuations and a return to positive capital returns after a prolonged downturn signal a cyclical inflection point; renewed investor confidence and the perceived passing of the valuation trough are likely to accelerate AUM growth and unlock higher management and performance fee income.

- Infrastructure and "living" real asset classes (including affordable housing, micro living, and senior living) are showing strong capital inflows, boosted by demographic shifts, public infrastructure investment, and urban migration-structural forces expected to drive sustainable revenue expansion and higher margins as PATRIZIA strengthens its position in these growth areas.

- Rising international client demand-particularly from Asia-Pacific (Japan, Korea) and renewed European interest-reflects ongoing global institutionalization of real assets, supporting larger fund inflows, broader client diversification, and increasing recurring fee income.

- Investments in operational efficiency through digital platforms and process optimization have materially improved cost discipline, doubled EBITDA, and raised margins; continued tech-driven productivity could support further increases in net margins and earnings quality as the investment cycle turns.

- The expected acceleration in transaction volumes and conversion of existing and newly raised client commitments positions the company for near-term AUM growth, directly enhancing management fee revenue and setting the stage for improved operating leverage as activity levels rise.

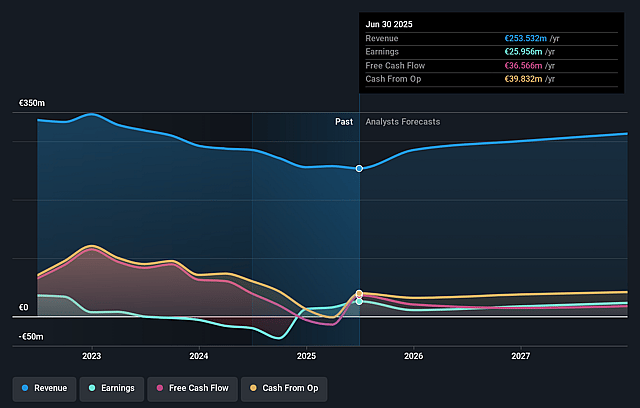

PATRIZIA Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming PATRIZIA's revenue will grow by 6.4% annually over the next 3 years.

- Analysts assume that profit margins will shrink from 10.2% today to 6.9% in 3 years time.

- Analysts expect earnings to reach €21.0 million (and earnings per share of €0.27) by about September 2028, down from €26.0 million today. However, there is a considerable amount of disagreement amongst the analysts with the most bullish expecting €31.4 million in earnings, and the most bearish expecting €18 million.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 47.9x on those 2028 earnings, up from 24.2x today. This future PE is greater than the current PE for the GB Real Estate industry at 14.5x.

- Analysts expect the number of shares outstanding to grow by 0.26% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 7.29%, as per the Simply Wall St company report.

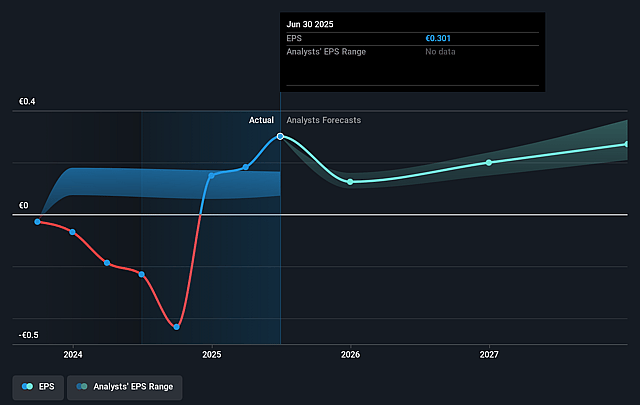

PATRIZIA Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The company reports stable or slightly declining Assets Under Management (AUM), with management expressing only cautious optimism regarding achieving their AUM growth guidance; this exposes PATRIZIA to potential stagnating or negative AUM growth if organic fundraising or deal closings fall short, which would meaningfully impact recurring fee income and constrain future revenue growth.

- Transaction and performance fees, which make up a variable and sometimes volatile portion of revenues, remain at relatively low levels amidst a slow and bumpy recovery in broader real asset transaction activity; the ongoing subdued levels in these areas suggest vulnerability to prolonged periods of weak earnings if the investment cycle does not accelerate as expected, pressuring profitability.

- PATRIZIA's cost reductions and improved EBITDA margin are largely a result of strict cost discipline rather than strong top-line growth, and CFO guidance suggests costs may rise again if business activity picks up, potentially compressing future net margins if revenue momentum does not simultaneously accelerate.

- The company's increased allocation to balance sheet investments, especially in co-investments and seed assets, exposes it further to real estate market valuation risks and foreign exchange volatility (particularly with infrastructure assets exposed to USD and AUD), increasing the risk of fair value losses that could negatively impact reported earnings.

- The sector remains exposed to long-term structural risks, including macroeconomic headwinds such as potential higher-for-longer interest rates, regulatory changes (ESG compliance, higher taxes), and institutional investor shifts that could see capital favoring other more liquid or alternative asset classes over traditional real estate, threatening both PATRIZIA's future AUM growth and its revenue and earnings outlook over the long term.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of €9.36 for PATRIZIA based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of €10.4, and the most bearish reporting a price target of just €8.2.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be €305.2 million, earnings will come to €21.0 million, and it would be trading on a PE ratio of 47.9x, assuming you use a discount rate of 7.3%.

- Given the current share price of €7.27, the analyst price target of €9.36 is 22.3% higher. Despite analysts expecting the underlying buisness to decline, they seem to believe it's more valuable than what the market thinks.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on PATRIZIA?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.