Catalysts

About MLP

MLP is a diversified German financial services group providing wealth management, insurance brokerage, banking, and consulting solutions for private, corporate, and institutional clients.

What are the underlying business or industry changes driving this perspective?

- Assets under management are at a record EUR 64.2 billion and still expanding. However, the heavy reliance on performance fees and volatile capital markets in wealth management means revenue growth could remain fragile, which may limit the pace at which earnings recover to past record levels.

- The group is investing significantly in artificial intelligence and digitalization to drive efficiency. If consultant adoption is delayed or client uptake of AI-enabled services is slower than expected, this could dilute the expected margin improvements and delay operating leverage in EBIT.

- Non-life insurance and health insurance continue to grow steadily. At the same time, a structurally weaker old age provision business and consultant time shifting toward wealth management may cap long-term premium growth, which could constrain recurring revenue expansion and net margin resilience.

- The banking arm is strong and well capitalized, with over EUR 1 billion of recent net inflows. A sustained low interest rate backdrop or intensified competition in German retail banking could compress spreads, reducing the contribution of net interest income to group earnings.

- Focusing the real estate business and exiting project development should gradually derisk the portfolio. In the near term, however, negative EBIT and lower fee potential from this area may offset part of the gains from higher quality income streams, which could mute the overall uplift to group EBIT growth.

Assumptions

This narrative explores a more pessimistic perspective on MLP compared to the consensus, based on a Fair Value that aligns with the bearish cohort of analysts. How have these above catalysts been quantified?

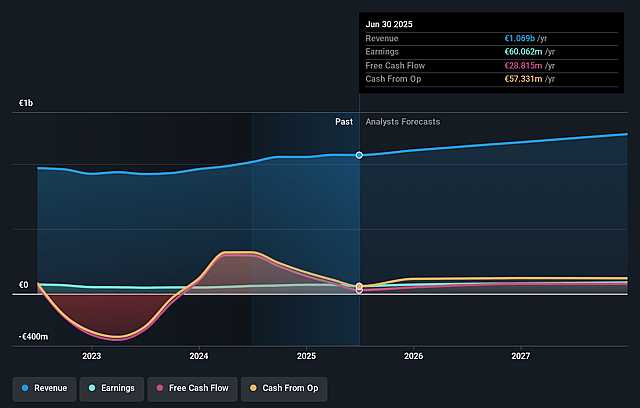

- The bearish analysts are assuming MLP's revenue will grow by 5.0% annually over the next 3 years.

- The bearish analysts assume that profit margins will increase from 6.2% today to 6.8% in 3 years time.

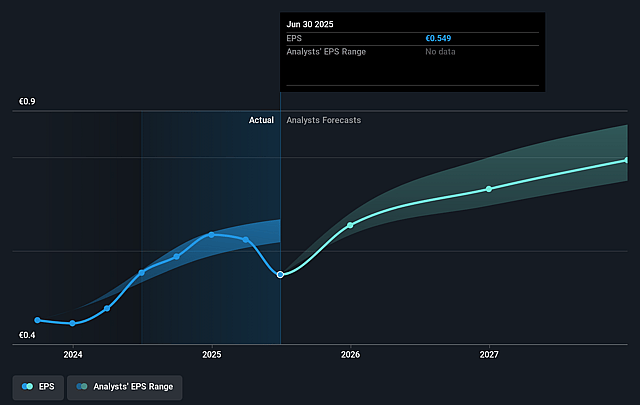

- The bearish analysts expect earnings to reach €83.1 million (and earnings per share of €0.76) by about December 2028, up from €65.5 million today. However, there is some disagreement amongst the analysts with the more bullish ones expecting earnings as high as €106.2 million.

- In order for the above numbers to justify the price target of the more bearish analyst cohort, the company would need to trade at a PE ratio of 14.0x on those 2028 earnings, up from 11.5x today. This future PE is lower than the current PE for the GB Capital Markets industry at 14.7x.

- The bearish analysts expect the number of shares outstanding to decline by 0.08% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 5.93%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?

- Performance based compensation in the Wealth competence field has fallen sharply compared to the previous year and management continues to guide cautiously, suggesting that structurally lower variable fees in volatile capital markets could cap long term revenue growth and weigh on earnings.

- The old age provision business is already weaker than expected and consultants are reallocating scarce time toward wealth management, which may structurally slow growth in Life and Health and reduce the diversification that currently supports recurring revenue and net margins.

- MLP is deliberately exiting and winding down real estate project development and expects negative EBIT from this segment in the near term. Prolonged weakness or further write downs in real estate could continue to drag on group EBIT and dilute overall margin improvement.

- The macro backdrop described by management as an ongoing economic downturn with rising unemployment and unsettled clients may persist. This could pressure client investment activity, constrain net inflows and limit the scalability of assets under management driven revenue and earnings.

- Heavy investment in artificial intelligence and digitalization is central to the midterm EBIT target uplift. Any delay in successful rollout, client adoption or realized efficiency gains would undermine the planned operating leverage and slow expansion of EBIT and net margins.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The assumed bearish price target for MLP is €9.0, which represents up to two standard deviations below the consensus price target of €10.5. This valuation is based on what can be assumed as the expectations of MLP's future earnings growth, profit margins and other risk factors from analysts on the more bearish end of the spectrum.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of €12.5, and the most bearish reporting a price target of just €9.0.

- In order for you to agree with the more bearish analyst cohort, you'd need to believe that by 2028, revenues will be €1.2 billion, earnings will come to €83.1 million, and it would be trading on a PE ratio of 14.0x, assuming you use a discount rate of 5.9%.

- Given the current share price of €6.91, the analyst price target of €9.0 is 23.2% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on MLP?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystLowTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystLowTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystLowTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.