Key Takeaways

- Focused investment in automation, digitalization, and high-value product innovation is set to enhance operational efficiency, margins, and long-term revenue quality.

- Targeting niche growth markets and expanding Southeast Asian manufacturing reduces global risks and positions the company for accelerated growth as end-markets rebound.

- Ongoing economic, protectionist, and supply chain headwinds combined with weak demand and limited progress in higher-growth segments threaten revenue stability, margin performance, and strategic repositioning.

Catalysts

About Phoenix Mecano- Manufactures and sells components for industrial customers worldwide.

- Strategic investments in digitalization and performance enhancement, including automation of internal processes and supply chain optimization, are likely to improve operational efficiency and reduce operating costs, supporting a recovery in operating margin and net earnings over time.

- Selective focus on profitable niche markets (such as explosion-proof enclosures, components for hydrogen infrastructure, current transducers for data centers, and solutions for smart grids) positions the company to capture growth from increasing industrial automation, renewable energy deployment, and infrastructure digitalization, boosting medium-to-long-term revenue growth.

- Expansion of manufacturing capacity in Southeast Asia-especially Vietnam-mitigates supply chain risks and tariff exposure linked to China, which should improve the reliability of order fulfillment and protect gross margins as global trade tensions persist.

- Actively launching product innovations for high-tech applications (e.g., data center current transformers, specialized enclosure solutions for LNG and hydrogen sectors, smart drive systems) supports a move towards higher-margin, value-added offerings and strengthens pricing power, positively impacting revenue quality and margin profile.

- The normalization of customer inventories and indications of order revival suggest a cyclical bottoming in major end-markets; a recovery in customer investments (in industrial automation, energy, and infrastructure) can drive a rebound in order intake and accelerate top-line growth in the next cycle.

Phoenix Mecano Future Earnings and Revenue Growth

Assumptions

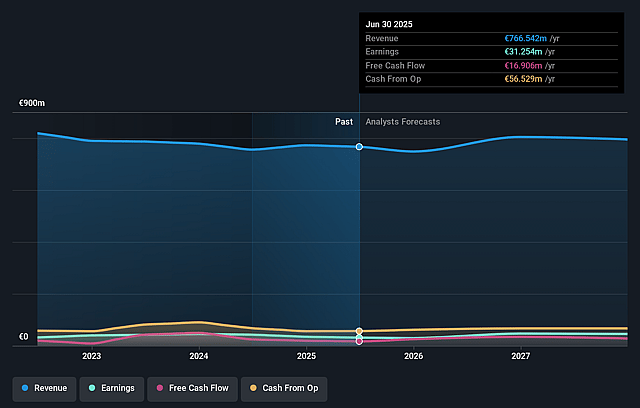

How have these above catalysts been quantified?- Analysts are assuming Phoenix Mecano's revenue will grow by 1.8% annually over the next 3 years.

- Analysts assume that profit margins will increase from 4.1% today to 6.8% in 3 years time.

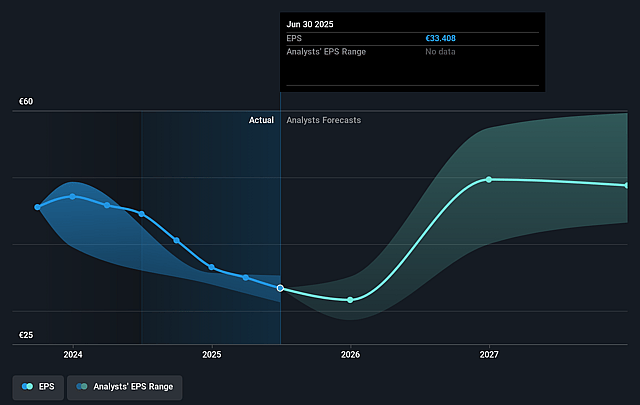

- Analysts expect earnings to reach €55.0 million (and earnings per share of €48.79) by about September 2028, up from €31.3 million today. However, there is some disagreement amongst the analysts with the more bearish ones expecting earnings as low as €38.5 million.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 0.0x on those 2028 earnings, down from 13.1x today. This future PE is lower than the current PE for the GB Electrical industry at 29.1x.

- Analysts expect the number of shares outstanding to decline by 1.07% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 6.49%, as per the Simply Wall St company report.

Phoenix Mecano Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- Continued global economic uncertainty, weak customer demand in key markets (notably in the U.S. for discretionary products like smart furniture), and delays in capital investments by industrial clients could lead to prolonged softness in revenue and declining or volatile earnings.

- The spike in U.S.-led tariffs, combined with broader global protectionist trends and supply chain disruptions (including rerouting from China to Southeast Asia), may impose indirect costs and operational complexity, increasing margin pressure and potentially affecting both top

- and bottom-line performance.

- The company's exposure to segments affected by commoditization, including traditional enclosures and component products that are increasingly subject to price competition and delayed orders, risks eroding gross margins and limits pricing power over time.

- Persistent volatility in order intake-highlighted by a book-to-bill "roller coaster," especially in the DewertOkin Technology Group-suggests significant unpredictability in short

- and medium-term revenue streams, which could undermine earnings stability and risk investor confidence.

- Significant one-off restructuring and performance enhancement costs, paired with only moderate penetration in higher-growth, software-driven automation solutions, raise questions about the speed and effectiveness of Phoenix Mecano's strategic repositioning, potentially limiting its ability to capture future revenue growth and improve net margins.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of CHF514.477 for Phoenix Mecano based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of CHF580.06, and the most bearish reporting a price target of just CHF440.46.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be €808.9 million, earnings will come to €55.0 million, and it would be trading on a PE ratio of 0.0x, assuming you use a discount rate of 6.5%.

- Given the current share price of CHF415.0, the analyst price target of CHF514.48 is 19.3% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Phoenix Mecano?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.