Last Update 07 Jul 26

Fair value Increased 29%SPB: Cautious Execution Outlook Will Temper Benefits Of Recent Share Buybacks

Analyst fair value for Superior Plus has been updated from CA$6.00 to CA$7.75, with recent price target increases across several firms reflecting analysts' revised expectations around growth, profitability, and risk assumptions.

Analyst Commentary

Recent research on Superior Plus points to a mix of optimism and restraint, with several firms updating their price targets and ratings as they refresh their models and assumptions. While the fair value estimate has moved higher overall, not all commentary is positive, and some signals highlight execution and growth risks that readers should keep in mind.

Across the latest updates, price targets on Superior Plus cluster in a relatively tight band around the mid single digit to low double digit range in Canadian dollars. Some analysts are comfortable reiterating more constructive ratings alongside higher targets, while others are holding the line with more neutral stances despite modest upward revisions. This split underlines that, even with revised assumptions, there is no clear consensus on how much upside is justified relative to current trading levels.

Several firms have raised their targets on Superior Plus in recent months, including adjustments to C$8, C$8.50, C$9 and C$10. In many cases, these moves sit alongside Hold, Market Perform, or Sector Perform ratings rather than more aggressive calls. For readers, that combination typically suggests that while analysts see room for fair value to sit above earlier estimates, they also see meaningful risks around the company hitting its growth and profitability objectives.

Rating language across these reports signals that some analysts remain cautious about Superior Plus, even as they fine tune their models. The presence of ratings such as Hold, Market Perform, and Sector Perform implies a view that the stock may trade roughly in line with peers rather than clearly outperforming. This ties back to open questions around execution, balance sheet priorities, and the timing of any improvement in margins or volumes.

In addition, recent research includes incremental target increases that are relatively modest in size, often in C$0.50 steps. That pattern suggests that for some bearish analysts, new information is not triggering a major reset in expectations. Instead, they appear to be nudging their valuation work higher while keeping a firm grip on risk assumptions related to operational performance, acquisition integration, and the broader demand backdrop in the propane and related services markets that Superior Plus serves.

Investors evaluating Superior Plus may want to consider how these mixed signals fit with their own expectations on earnings power, capital allocation, and the company’s ability to deliver against its stated priorities. The balance between higher fair value estimates and still cautious ratings captures the current debate around whether the stock already reflects much of the anticipated improvement or whether there is still a reasonable margin of safety.

Bearish Takeaways

- Bearish analysts maintaining Hold or equivalent ratings, even as they adjust price targets upward, signal concerns that Superior Plus may offer limited return potential relative to its risk profile at current levels.

- Incremental target moves of around C$0.50 suggest that some bearish analysts are only modestly revising their valuation work, which can reflect uncertainty around execution on growth plans and the durability of any margin improvement.

- Neutral style ratings such as Market Perform and Sector Perform indicate that certain analysts see Superior Plus tracking in line with peers rather than clearly outperforming, highlighting questions about the company’s ability to outgrow or out-earn its sector over time.

- The cautious tone embedded in these ratings, despite higher targets, points to underlying worries about operational risks, acquisition integration, and the potential for volatility in earnings if market conditions or demand trends do not support current assumptions.

What’s in the News for Superior Plus

- Superior Plus reported that from January 1, 2026 to March 31, 2026, it repurchased 4,200,000 shares for C$22 million, representing 1.92% of its shares, under its existing buyback program. (Source: Key Developments)

- The company has now completed the repurchase of 8,400,000 shares in total for C$44.1 million, representing 3.8% of its shares, under the buyback that was announced on November 17, 2025. (Source: Key Developments)

Valuation Changes for Superior Plus

- Fair Value: The analyst fair value estimate has increased from CA$6.00 to CA$7.75, indicating a higher assessed value for Superior Plus based on updated assumptions.

- Discount Rate: The discount rate has decreased slightly from 7.35% to 6.76%, which increases the present value placed on Superior Plus cash flows in analysts' models.

- Revenue Growth: The assumed annual revenue growth rate has risen from 1.44% to 2.63%, reflecting a higher modeled pace of top line expansion for Superior Plus.

- Net Profit Margin: The assumed net profit margin has moved up from 4.47% to 5.36%, suggesting analysts now model stronger earnings generation on each dollar of revenue.

- Future P/E: The future P/E multiple has risen from 8.64x to 9.06x, implying a slightly higher valuation multiple applied to Superior Plus projected earnings.

Key Takeaways

- Electrification, alternative heating, and urbanization trends threaten long-term propane demand, revenue growth, and core market stability.

- Reliance on fossil fuels exposes the company to regulatory risk, higher compliance costs, and pressure on net margins as energy standards tighten.

- Accelerating electrification, regulatory pressure, and balance sheet risks threaten Superior Plus's traditional fuel businesses, margin stability, and long-term growth amid market and customer attrition challenges.

Catalysts

About Superior Plus- Distributes propane, compressed natural gas, and renewable energy and related products and services in the United States and Canada.

- While Superior Plus is benefiting from short-term volume and efficiency gains spurred by the transformation efforts in its propane and CNG divisions, the company faces ongoing structural headwinds as ongoing electrification and adoption of alternative heating technologies threaten to steadily erode long-term propane demand, which could restrict both revenue growth and margin expansion beyond the next several years.

- Although the company is actively optimizing delivery logistics and investing in digital transformation to lift net margins and bolster customer retention, continued reliance on fossil fuels leaves it susceptible to stricter environmental regulations and higher compliance costs over time, which may ultimately curb net earnings and compress operating margins as energy standards tighten across North America.

- While population growth and suburbanization continue to support a stable market for propane in rural and off-grid regions, demographic trends toward urbanization and increasing penetration of electric heating solutions could gradually diminish Superior Plus's addressable residential and commercial customer base, capping long-term volume growth and future revenues in its core propane segment.

- Even as the CNG (Certarus) division sees robust expansion in industrial, RNG, and hydrogen business lines-reflecting successful diversification-the core well site CNG market remains highly cyclical and exposed to volatile oil and gas drilling activity, which introduces sustained unpredictability into segment EBITDA and challenges stable year-over-year earnings performance.

- Though Superior Plus's acquisition-driven consolidation strategy and operational improvements have yielded near-term scale and cost benefits, persistent execution risks in integrating acquired businesses, as well as the industry's ongoing shift away from fossil fuels, present material obstacles to achieving sustainable margin improvements and earnings growth over the longer term.

Superior Plus Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

- This narrative explores a more pessimistic perspective on Superior Plus compared to the consensus, based on a Fair Value that aligns with the bearish cohort of analysts.

- The bearish analysts are assuming Superior Plus's revenue will grow by 2.6% annually over the next 3 years.

- The bearish analysts assume that profit margins will increase from 1.6% today to 5.4% in 3 years time.

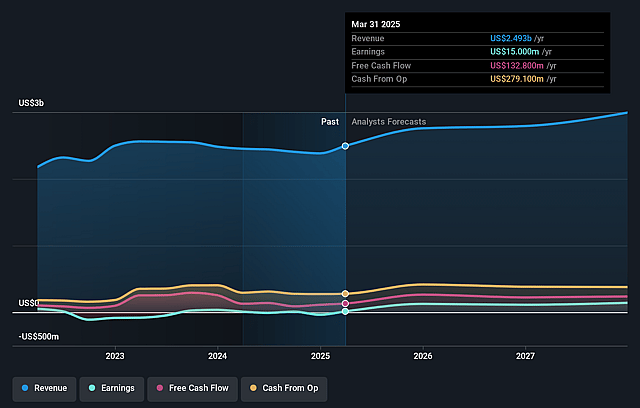

- The bearish analysts expect earnings to reach $136.2 million (and earnings per share of $0.5) by about July 2029, up from $38.4 million today. However, there is some disagreement amongst the analysts with the more bullish ones expecting earnings as high as $160.2 million.

- In order for the above numbers to justify the price target of the more bearish analyst cohort, the company would need to trade at a PE ratio of 9.1x on those 2029 earnings, down from 30.9x today. This future PE is lower than the current PE for the CA Gas Utilities industry at 30.9x.

- The bearish analysts expect the number of shares outstanding to decline by 4.54% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 6.76%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- Superior Plus's core propane and CNG divisions are exposed to long-term demand erosion as electrification and decarbonization accelerate, with widespread adoption of heat pumps and electric solutions steadily reducing total addressable markets, negatively impacting revenue growth and margin stability.

- The company's acquisition-driven growth model, combined with leverage near 3.7 times EBITDA and ongoing share repurchases, risks overextending the balance sheet, which could lead to increased interest expense and reduced capacity for reinvestment, placing pressure on earnings in a rising rate or tightening credit environment.

- Increased customer attrition in key U.S. propane markets and anticipated ongoing churn, especially before the full rollout of customer retention and pricing optimization tools, may challenge organic volume growth, with risks to base revenues and potential for higher bad debt expense if engagement initiatives underdeliver.

- The CNG segment remains vulnerable to commodity-driven cycles and industry overcapacity, as indicated by idle trailer capacity, shrinking returns on new MSU deployments, and competitors exiting the market, raising the likelihood of margin compression and volatility in adjusted EBITDA if market conditions deteriorate further or industrial demand lags.

- Secular trends toward urbanization and regulatory scrutiny of greenhouse gas emissions from fossil fuels could accelerate customer migration away from propane and CNG, requiring heavier investment in lower-carbon alternatives and compliance, threatening long-term revenue streams and compressing net margins.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The assumed bearish price target for Superior Plus is CA$7.75, which represents up to two standard deviations below the consensus price target of CA$8.84. This valuation is based on what can be assumed as the expectations of Superior Plus's future earnings growth, profit margins and other risk factors from analysts on the more bearish end of the spectrum.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of CA$10.0, and the most bearish reporting a price target of just CA$7.75.

- In order for you to agree with the more bearish analyst cohort, you'd need to believe that by 2029, revenues will be $2.5 billion, earnings will come to $136.2 million, and it would be trading on a PE ratio of 9.1x, assuming you use a discount rate of 6.8%.

- Given the current share price of CA$7.85, the analyst price target of CA$7.75 is 1.3% lower. The relatively low difference between the current share price and the analyst consensus price target indicates that they believe on average, the company is fairly priced.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Superior Plus?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystLowTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystLowTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystLowTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.