Last Update 08 Jul 26

Fair value Decreased 3.64%ABX: Rich Multiple And Execution Risks Will Pressure Future Share Returns

The analyst price target for Barrick Mining has shifted from CA$33.69 to CA$32.46 as analysts update their assumptions around fair value, discount rates, revenue growth, profit margins and future P/E expectations.

Analyst Commentary

With the recent adjustment in the analyst price target for Barrick Mining to CA$32.46, recent commentary has focused on how valuation assumptions, execution risks and growth expectations line up with this updated view of fair value. For investors, the key themes are how sensitive Barrick Mining’s valuation is to changes in discount rates, revenue trajectories, profit margins and future P/E assumptions.

Bearish analysts point to the revised target as a signal that the balance of risks and rewards around Barrick Mining is being reassessed, rather than as a simple call on short term price moves. The discussion is centering on whether current market pricing fully reflects uncertainties around the company’s ability to deliver on its operational and financial plans.

Bearish Takeaways

- Bearish analysts view the shift to a lower price target as a sign that the margin of safety in Barrick Mining’s valuation may have narrowed, with less room for execution missteps or weaker than expected operating results.

- Some caution that expectations for future P/E multiples could be too optimistic relative to perceived risks in project delivery, cost control and capital allocation, which might limit upside versus the updated CA$32.46 target.

- There is concern that assumptions around revenue and profit margin trajectories leave Barrick Mining exposed if commodity pricing or operational performance does not align with forecasts, creating downside risk to valuation models.

- Bearish analysts also flag that higher discount rate assumptions in some models can have a material impact on fair value estimates, suggesting that Barrick Mining’s long dated cash flows could be more vulnerable to changes in market required returns.

What’s in the News for Barrick Mining

- A comparison of Agnico Eagle Mines Limited and Barrick Mining highlights both companies advancing major growth projects, maintaining strong liquidity, and focusing on debt reduction alongside dividends and share buybacks, source: “Agnico Eagle vs. Barrick Mining: Which Gold Miner is Shining Brighter?”

- Barrick Mining is being discussed as a potential gold safe haven stock as geopolitical tensions rise, with recent earnings per share reported above analyst expectations, source: “Barrick Mining (B) Is Becoming A Gold Safe Haven After An Earnings Beat.”

- The Board of Directors of Barrick Mining has authorized a share repurchase plan dated May 11, 2026, allowing the company to buy back its own shares.

- Barrick Mining has announced a share repurchase program of up to US$3,000 million at prevailing market prices, with management indicating this follows solid execution and strong free cash flow and is timed with what the company views as exceptional value in its shares ahead of the planned IPO of North American Barrick.

- Barrick Mining has provided 2026 production guidance, with gold production expected in a range of 2.90 to 3.25 million ounces and copper production expected in a range of 190,000 to 220,000 tonnes, with gold output anticipated to be higher in the third and fourth quarters in line with typical seasonality.

Valuation Changes for Barrick Mining

- Fair Value revised from CA$33.69 to CA$32.46, representing a modest reduction in the assessed price target range.

- Discount Rate adjusted from 7.81% to 7.90%, indicating a slight increase in the required return applied to Barrick Mining’s future cash flows.

- Revenue Growth revised from 10.22% to 6.51%, indicating a meaningfully lower assumed revenue growth trajectory in updated models.

- Net Profit Margin adjusted from 24.99% to 24.24%, reflecting a small reduction in expected profitability on each dollar of revenue.

- Future P/E updated from 8.48x to 8.17x, showing a slightly lower valuation multiple applied to Barrick Mining’s projected earnings.

Key Takeaways

- Decarbonization trends, material recycling, and alternative materials threaten long-term demand, potentially undermining Barrick's growth, revenue, and project viability.

- Reliance on high-risk regions and tightening ESG regulations exposes Barrick to heightened operational, compliance, and cost pressures that may erode margins and cash flow.

- Expanded high-grade assets, operational efficiency gains, disciplined capital allocation, and portfolio optimization are driving strong profitability, stable earnings, and sustainable growth.

Catalysts

About Barrick Mining- Engages in the exploration, development, production, and sale of mineral properties.

- The push for global decarbonization and renewables may severely erode future demand for both gold and copper, undermining Barrick's core long-term growth assumptions and putting sustained pressure on revenues, especially as investor appetite for metals as stores of value or electrification inputs diminishes.

- The company's increasing reliance on projects and expansions located in politically unstable or high-risk jurisdictions, such as Mali and Pakistan, exposes Barrick to heightened risks of expropriation, project delays, and new resource nationalism measures, which may materially disrupt production flows, raise development costs, and lead to permanent asset impairments impacting net earnings.

- Intensifying global ESG regulations and stakeholder expectations will likely force Barrick to absorb escalating compliance costs, delayed permitting, and potentially higher sustaining and development CapEx, which could squeeze operating margins and blunt the cash flow improvements the company currently highlights.

- Long-term risks from accelerating advances in recycling technologies and alternative materials threaten to undercut global primary metal demand, making large brownfield expansions and greenfield projects less economically viable and potentially leading to stranded assets or declining returns on invested capital.

- Depleting average ore grades and maturing flagship mines may mean Barrick faces a structurally higher cost base over the next decade, requiring ever-greater investments to merely sustain current production levels, which could drive margin compression and erode free cash flow despite management's current focus on cost reductions.

Barrick Mining Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

- This narrative explores a more pessimistic perspective on Barrick Mining compared to the consensus, based on a Fair Value that aligns with the bearish cohort of analysts.

- The bearish analysts are assuming Barrick Mining's revenue will grow by 6.5% annually over the next 3 years.

- The bearish analysts assume that profit margins will shrink from 32.1% today to 24.2% in 3 years time.

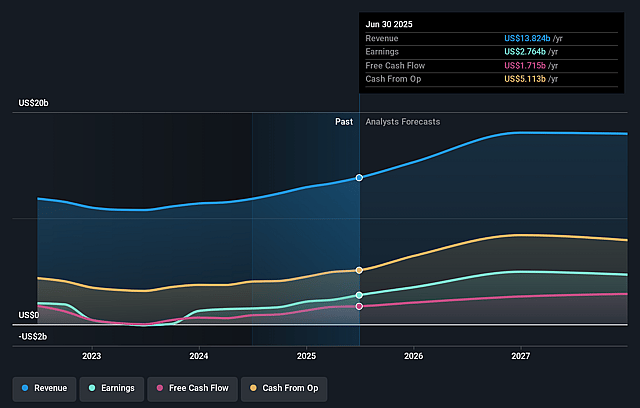

- The bearish analysts expect earnings to reach $5.6 billion (and earnings per share of $3.49) by about July 2029, down from $6.1 billion today. However, there is some disagreement amongst the analysts with the more bullish ones expecting earnings as high as $9.7 billion.

- In order for the above numbers to justify the price target of the more bearish analyst cohort, the company would need to trade at a PE ratio of 8.2x on those 2029 earnings, down from 10.1x today. This future PE is lower than the current PE for the CA Metals and Mining industry at 14.4x.

- The bearish analysts expect the number of shares outstanding to decline by 1.79% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 7.9%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- The discovery and ongoing definition of the massive, high-grade Fourmile orebody in Nevada-potentially doubling current resources and lowering unit costs-could meaningfully increase Barrick's gold production and improve net margins for years to come.

- The successful ramp-up and expansion projects at Pueblo Viejo, Lumwana, and the Reko Diq copper-gold project signal a clear pipeline of long-life, low-cost Tier 1 assets that enhance revenue growth, extend mine life, and deliver improved earnings stability.

- Strong year-over-year and quarter-on-quarter improvements in operational efficiency, with sustained reductions in all-in sustaining costs and robust production increases, point to strengthening profitability and resilience in both net earnings and free cash flow.

- A highly disciplined capital allocation strategy, including active share buybacks, significant dividend payments, and a robust net-cash balance sheet, positions Barrick to boost shareholder returns and stabilize long-term earnings even during commodity cycles.

- Strategic portfolio optimization-rationalizing non-core assets while continually replacing and expanding reserves through organic growth and exploration success-supports a sustainable growth trajectory and provides visibility to rising long-term revenues and cash flows.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The assumed bearish price target for Barrick Mining is CA$32.46, which represents up to two standard deviations below the consensus price target of CA$72.53. This valuation is based on what can be assumed as the expectations of Barrick Mining's future earnings growth, profit margins and other risk factors from analysts on the more bearish end of the spectrum.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of CA$98.52, and the most bearish reporting a price target of just CA$31.8.

- In order for you to agree with the more bearish analyst cohort, you'd need to believe that by 2029, revenues will be $23.0 billion, earnings will come to $5.6 billion, and it would be trading on a PE ratio of 8.2x, assuming you use a discount rate of 7.9%.

- Given the current share price of CA$52.33, the analyst price target of CA$32.46 is 61.2% lower.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Barrick Mining?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystLowTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystLowTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystLowTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.