Last Update 04 Dec 25

Fair value Increased 0.65%UCB: Pipeline Execution And New Launches Will Support Balanced Future Upside Potential

UCB's fair value estimate has been nudged higher to approximately EUR 258 from EUR 257, reflecting analysts' upward revisions to price targets, with recent moves to EUR 240, EUR 285 and EUR 290. These changes highlight confidence in the company's earnings trajectory despite slightly softer margin and growth assumptions.

Analyst Commentary

Recent target price increases signal that bullish analysts see UCB as well positioned to deliver on its growth strategy, with upside potential relative to the current trading range. The cluster of upward revisions indicates broad support for the earnings outlook despite a more tempered view on margins.

Bullish Takeaways

- Bullish analysts view the stepped up price targets, moving into the EUR 240 to EUR 290 range, as justified by improved earnings visibility from the late stage pipeline and recent launches.

- The higher fair value assumptions reflect confidence that UCB can execute on new product rollouts and expand market share in key immunology and neurology indications, supporting high single digit to low double digit medium term growth.

- Valuation is seen as attractive on a risk adjusted basis, with the increased price targets implying further upside if UCB delivers on its innovation and regulatory milestones.

- Analysts also highlight a stronger balance sheet and cash generation profile, which should provide flexibility for continued investment in R and D and targeted business development without stretching leverage.

Bearish Takeaways

- More cautious analysts point to ongoing execution risk around launch trajectories, noting that any delays in uptake or pricing pressure could challenge the assumptions embedded in higher valuation targets.

- There is some concern that margin expansion may be slower than previously expected as UCB continues to invest heavily in commercialization and development, potentially limiting near term earnings leverage.

- Competitive dynamics in core therapy areas remain a watch point, with the possibility that emerging treatments or biosimilar competition could cap long term growth and put pressure on premium pricing assumptions.

- Regulatory and reimbursement uncertainties in key markets are seen as potential downside catalysts, especially if outcomes do not fully support the optimistic revenue scenarios underlying recent target upgrades.

What's in the News

- Citizen Health and UCB launched a multi year, AI driven partnership focused on epilepsy and five rare diseases to accelerate patient centered drug discovery and clinical trial participation. (Strategic Alliances)

- The FDA approved KYGEVVI, the first treatment for thymidine kinase 2 deficiency in patients with symptom onset at or before age 12, with data showing an approximately 86% reduction in overall risk of death versus matched controls. (Product Related Announcements)

- UCB reported three year Phase 3 and extension data for BIMZELX across psoriatic arthritis, axial spondyloarthritis and ankylosing spondylitis, reinforcing its long term efficacy and supporting its leadership ambitions in rheumatology. (Product Related Announcements)

- Three year BE HEARD data for BIMZELX in moderate to severe hidradenitis suppurativa showed durable high threshold responses and improved quality of life, particularly when treatment is initiated earlier after diagnosis. (Product Related Announcements)

- UCB expanded its FASTRAX Canada program to a new Thunder Bay rheumatology site, aiming to shorten diagnostic delays in axial spondyloarthritis and improve access to specialist care in underserved North Western Ontario communities. (Business Expansions)

Valuation Changes

- The fair value estimate has risen slightly to approximately €258 from around €257, reflecting modestly higher analyst expectations despite softer operating assumptions.

- The discount rate is unchanged at 6.16%, indicating no adjustment to the perceived risk profile or cost of capital for UCB.

- Revenue growth has eased marginally to about 13.16% from roughly 13.22%, pointing to a slightly more conservative top line trajectory.

- The net profit margin has fallen modestly to around 21.50% from about 22.22%, implying somewhat lower profitability expectations over the forecast period.

- The future P/E multiple has risen slightly to approximately 27.4x from around 26.3x, suggesting investors may be willing to pay a bit more for UCB's expected earnings stream.

Key Takeaways

- Expansion into chronic and underserved conditions with innovative therapies and specialty biologics positions UCB for sustained growth and resilience against competitive pressures.

- Investments in manufacturing, digital R&D, and effective global market access enhance scalability, operational efficiency, and long-term margin expansion.

- Sustained pressures from pricing, patent expiries, changing reimbursement, R&D risks, and therapeutic alternatives threaten UCB's long-term growth, margins, and demand for core products.

Catalysts

About UCB- A biopharmaceutical company, develops products and solutions for people with neurology and immunology diseases worldwide.

- Strong demand drivers are in place due to the expansion of chronic disease prevalence in aging populations and increased global healthcare spending, especially in emerging markets; UCB's launch of BIMZELX and other late-stage therapies targeting underserved and chronic conditions positions the company to capture significant new revenue streams over the coming years.

- UCB's deep and advancing innovation pipeline, along with its focus on differentiated products in neurology and immunology, supports the ability to launch multiple new indications, address rare/orphan diseases, and leverage advances in personalized medicine, all of which underpin sustained long-term revenue growth and margin expansion.

- Effective global market access and rapid penetration-especially in the U.S., Europe, and Japan-with high conversion rates to paid scripts, broadening indications, and robust patient onboarding programs for key launches like BIMZELX are driving accelerating top-line growth and improved gross margin mix.

- Significant investments into manufacturing capacity (e.g., U.S. greenfield expansion) and digitalization of R&D are expected to support future scalability, operational efficiencies, and cost competitiveness, directly benefiting net margin and long-term earnings potential.

- Strategic focus on rare diseases and specialty biologics, where UCB already demonstrates strong expertise and growing market share, aligns with long-term industry trends toward higher pricing power and less competition, providing resilience against generic erosion and supporting durable high-margin revenue.

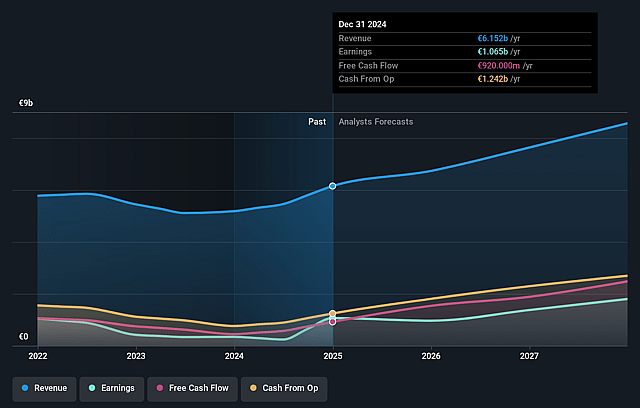

UCB Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming UCB's revenue will grow by 11.3% annually over the next 3 years.

- Analysts assume that profit margins will increase from 19.5% today to 21.7% in 3 years time.

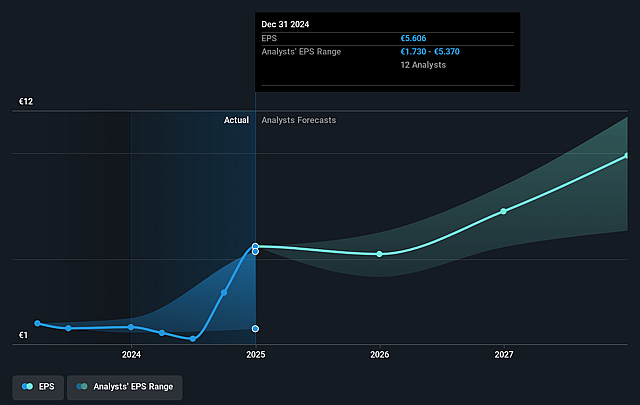

- Analysts expect earnings to reach €2.1 billion (and earnings per share of €10.98) by about September 2028, up from €1.3 billion today. However, there is a considerable amount of disagreement amongst the analysts with the most bullish expecting €2.4 billion in earnings, and the most bearish expecting €1.4 billion.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 24.6x on those 2028 earnings, down from 28.8x today. This future PE is lower than the current PE for the GB Pharmaceuticals industry at 53.4x.

- Analysts expect the number of shares outstanding to remain consistent over the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 5.97%, as per the Simply Wall St company report.

UCB Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- Intense pricing pressure and increasing rebate rates in the U.S. market, especially for BIMZELX, are expected to continue as market access expands and payer negotiations intensify-this structural pricing erosion threatens UCB's long-term revenue growth and net margins.

- Patent expiries and biosimilar competition loom for key mature assets such as CIMZIA, as acknowledged with ongoing price erosion and normalization of U.S. buying patterns, putting significant pressure on both revenue and future earnings as exclusivity wanes.

- Rising global healthcare cost containment, payer scrutiny, and the potential implementation of U.S. tariffs could materially reduce reimbursement, increase supply chain costs, and create uncertainty around UCB's ability to sustain profitability, impacting both net margin and revenues over the long term.

- High R&D spending and pipeline concentration within neurology, immunology, and a few launch products (especially BIMZELX) increases vulnerability to late-stage clinical setbacks, regulatory hurdles, or competitive launches, risking volatility in R&D expenses and future earnings if approvals disappoint or therapeutic displacement occurs.

- Advancements in alternative modalities-such as efficacious oral therapies for chronic inflammatory diseases (e.g., Icotrokinra)-in combination with a general trend towards preventative medicine and digital health, may reduce long-term reliance on chronic biologic interventions and threaten sustained demand and revenue for UCB's cornerstone biologic products.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of €225.0 for UCB based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of €255.0, and the most bearish reporting a price target of just €160.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be €9.4 billion, earnings will come to €2.1 billion, and it would be trading on a PE ratio of 24.6x, assuming you use a discount rate of 6.0%.

- Given the current share price of €202.0, the analyst price target of €225.0 is 10.2% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.