Key Takeaways

- Erosion of pricing power and reimbursement constraints are compressing margins and limiting the ability to convert prescription growth into sustainable revenue gains.

- Pipeline and legacy products face revenue risks from generic competition, innovation disruption, and rising R&D costs challenging long-term business model viability.

- Strong innovation pipeline, successful product launches, and disciplined global strategy position UCB for sustained revenue growth, margin improvement, and long-term shareholder value.

Catalysts

About UCB- A biopharmaceutical company, develops products and solutions for people with neurology and immunology diseases worldwide.

- Heightened global regulatory scrutiny and persistent pricing pressures are set to intensify in the coming years, particularly in key markets like the U.S. and Europe, resulting in steadily eroding net revenue per prescription across UCB's growing portfolio and limiting the ability to translate volume growth into corresponding revenue growth.

- Structural healthcare budget constraints, especially in Europe where many of UCB's products rely on public reimbursement, will further compress reimbursement rates, slow the pace of new product uptake, and place severe pressure on net margins for both legacy and recently launched therapies.

- The progressive loss of exclusivity for current and upcoming blockbuster products, such as CIMZIA and BRIVIACT, leaves UCB highly exposed to competition from generics and biosimilars, accelerating revenue cliffs and causing volatility in earnings despite pipeline expansion.

- Escalating costs and complexity of clinical development threaten to outpace topline growth, as delays, increasing R&D expense, and operational inefficiencies erode profitability, particularly if late-stage pipeline assets fail to deliver sufficient commercial returns to offset high initial investment.

- Rapid disruption by novel treatment modalities such as gene and cell therapies, combined with increasingly stringent safety requirements in immunology and neurology, risk rendering UCB's core business model and conventional biologic pipeline obsolete, exposing future top-line and earnings to secular decline.

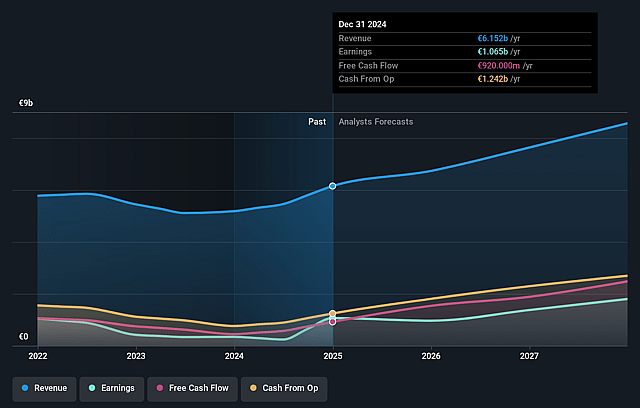

UCB Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- This narrative explores a more pessimistic perspective on UCB compared to the consensus, based on a Fair Value that aligns with the bearish cohort of analysts.

- The bearish analysts are assuming UCB's revenue will grow by 8.4% annually over the next 3 years.

- The bearish analysts assume that profit margins will shrink from 17.3% today to 16.8% in 3 years time.

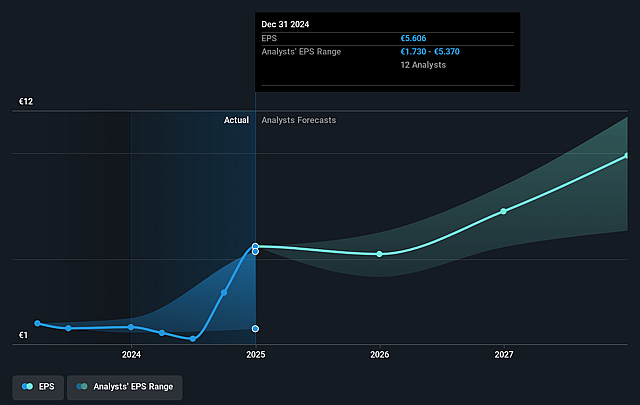

- The bearish analysts expect earnings to reach €1.3 billion (and earnings per share of €6.93) by about July 2028, up from €1.1 billion today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the price target of the more bearish analyst cohort, the company would need to trade at a PE ratio of 27.5x on those 2028 earnings, down from 31.7x today. This future PE is lower than the current PE for the GB Pharmaceuticals industry at 49.0x.

- Analysts expect the number of shares outstanding to grow by 0.17% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 5.86%, as per the Simply Wall St company report.

UCB Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- UCB's strong track record of innovation, highlighted by an R&D success rate significantly above the industry average and a robust, diversified pipeline in immunology and neurology, positions it to deliver sustained long-term revenue and earnings growth.

- The rapid launch uptake and expanding market penetration of key growth products such as BIMZELX, RYSTIGGO, ZILBRYSQ, and FINTEPLA, across multiple geographies and indications, create multiple independent growth drivers that lower reliance on legacy products and help stabilize topline revenues.

- The strategic focus on margin expansion, discipline in operational execution, and enhanced gross margin due to a favorable product mix point toward ongoing improvement in net margins and core EPS for the coming years.

- UCB's global reach, with successful reimbursement negotiations and broadening access in the US, Europe, Japan, and other regions, provides resilience against single-market risks and opens avenues for increased international revenue.

- Management's commitment to continued investment in innovative R&D, sustained dividend growth, and a measured approach to M&A and portfolio optimization indicate prudent capital allocation, supporting long-term earnings stability and shareholder returns.

Valuation

How have all the factors above been brought together to estimate a fair value?- The assumed bearish price target for UCB is €159.58, which represents two standard deviations below the consensus price target of €214.39. This valuation is based on what can be assumed as the expectations of UCB's future earnings growth, profit margins and other risk factors from analysts on the more bearish end of the spectrum.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of €250.0, and the most bearish reporting a price target of just €135.0.

- In order for you to agree with the bearish analysts, you'd need to believe that by 2028, revenues will be €7.8 billion, earnings will come to €1.3 billion, and it would be trading on a PE ratio of 27.5x, assuming you use a discount rate of 5.9%.

- Given the current share price of €177.85, the bearish analyst price target of €159.58 is 11.4% lower. Despite analysts expecting the underlying buisness to improve, they seem to believe the market's expectations are too high.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

AnalystLowTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystLowTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystLowTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.