Key Takeaways

- Expansion and strategic investments aim to boost revenue, improve stability, and enhance operational efficiencies in the rapidly evolving energy market.

- Focus on electrification and innovative energy solutions could capture growing demand and protect margins against market volatility and contract expirations.

- Increased investment, market volatility, and operational challenges could pressure revenue and margins, potentially impacting future earnings for AGL Energy.

Catalysts

About AGL Energy- Engages in the supply of energy and other essential services to residential, business, and wholesale customers in Australia.

- AGL Energy is expanding its development pipeline with new firming options, including the 500-megawatt Liddell battery, which is on track to commence operations in early 2026. This expansion is likely to increase revenue and provide stability against market volatility.

- The strategic partnership and equity investment in Kaluza is part of AGL's retail transformation program. This investment is expected to lead to operational efficiencies and simplify the product offerings, potentially improving net margins by $70 to $90 million annually starting FY '29.

- AGL's focus on electrification, including the capture of the rapidly growing EV market, is anticipated to significantly drive up energy demand and future revenue, leveraging growth expected from a doubling of NEM demand by 2050.

- The deployment of grid-scale batteries and flexible assets is improving the company's capability to capture market volatility and achieve premium pricing. This capability could enhance the realized pricing outcomes and boost earnings.

- AGL's gas contracting strategy post-2027, including new supply opportunities, aims to secure margins and optimize the dual fuel customer base, safeguarding against potential margin compression when the QGC contract expires.

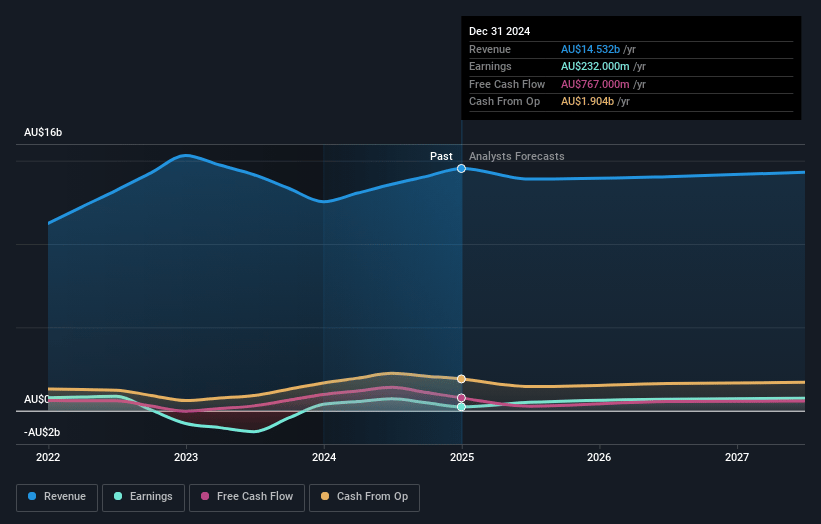

AGL Energy Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming AGL Energy's revenue will decrease by 1.3% annually over the next 3 years.

- Analysts assume that profit margins will increase from 1.6% today to 4.6% in 3 years time.

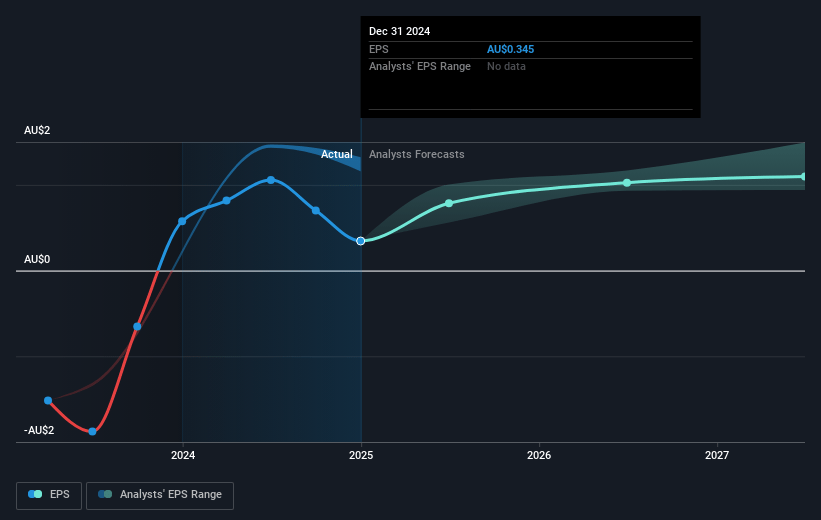

- Analysts expect earnings to reach A$643.0 million (and earnings per share of A$0.96) by about July 2028, up from A$232.0 million today. However, there is some disagreement amongst the analysts with the more bullish ones expecting earnings as high as A$1.0 billion.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 15.1x on those 2028 earnings, down from 28.6x today. This future PE is lower than the current PE for the AU Integrated Utilities industry at 22.8x.

- Analysts expect the number of shares outstanding to remain consistent over the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 6.41%, as per the Simply Wall St company report.

AGL Energy Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- Planned major outages and unplanned outages reduced thermal fleet availability, lowering revenue from generation.

- Increased depreciation and amortization due to continued investment reduces net income and future earnings.

- Market volatility and potential competition in the second half may compress customer margins, impacting overall revenue.

- Growing operating costs and higher investments in acquisitions and asset management could exert pressure on net margins.

- Upcoming recontracting of the QGC gas supply at potentially less favorable terms may impact revenue and margin sustainability.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of A$12.008 for AGL Energy based on their expectations of its future earnings growth, profit margins and other risk factors.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be A$14.0 billion, earnings will come to A$643.0 million, and it would be trading on a PE ratio of 15.1x, assuming you use a discount rate of 6.4%.

- Given the current share price of A$9.86, the analyst price target of A$12.01 is 17.9% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.