Key Takeaways

- Leadership in digital advice and strong client trust position Bravura for rapid expansion and enhanced market share across APAC and EMEA.

- Operational efficiencies, product standardisation, and SaaS adoption are set to boost long-term margins and sustainable above-industry earnings growth.

- Lack of innovation and overreliance on a few major clients threaten Bravura's growth, revenue stability, and ability to compete with agile, tech-focused rivals.

Catalysts

About Bravura Solutions- Develops, licenses, and maintains administration and management software applications for the wealth management and funds administration sectors in Australia, the United Kingdom, New Zealand, and internationally.

- Analyst consensus expects APAC Digital Advice traction and EMEA market demand to modestly support revenue, but these trends are likely understated: with Bravura now a clear leader in Digital Advice and top-of-mind in new RFPs, rapid market expansion in APAC and renewed client trust in EMEA could drive outsized revenue acceleration and earlier capture of high-margin registry and workplace opportunities.

- While margin improvements are in line with analyst expectations, ongoing engineering enhancements and operational cost-outs, combined with increasing SaaS adoption, position Bravura for a structural uplift in long-term EBITDA and net margins well above the software industry benchmark as recurring revenues scale.

- The accelerating digitisation of global financial services and greater regulatory complexity create a secular tailwind that expands Bravura's addressable market, increasing the velocity of new client wins and driving sustainable, double-digit revenue growth for several years.

- Bravura's strategic investments in engineering and product standardisation-such as consolidating code bases and leveraging global centers of excellence-will not only continue to lower delivery costs but also enable superior scalability, helping gross margin expand and opening the door to significant operating leverage over time.

- The company is primed to capture further market share as large institutions consolidate their wealth management platforms and demand interoperability-Bravura's established cloud-native, API-enabled suite positions it to win larger deals, cross-sell seamlessly, and support above-market EPS growth through both new contracts and deeper client penetration.

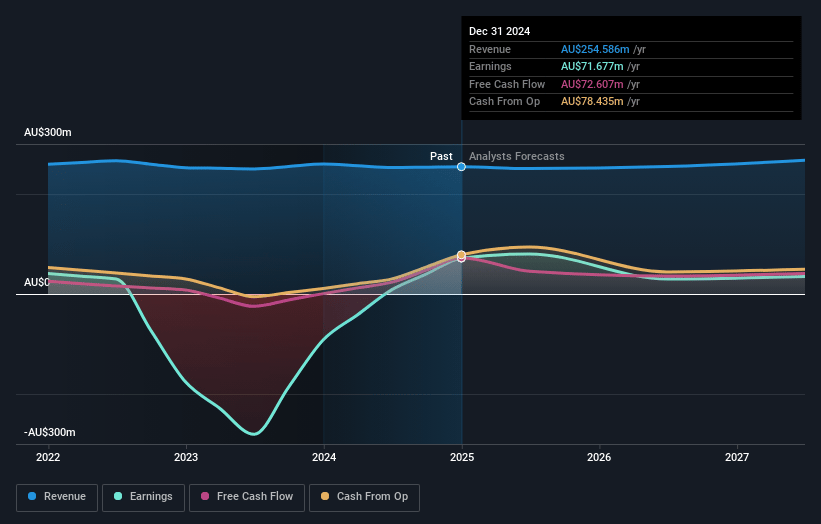

Bravura Solutions Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- This narrative explores a more optimistic perspective on Bravura Solutions compared to the consensus, based on a Fair Value that aligns with the bullish cohort of analysts.

- The bullish analysts are assuming Bravura Solutions's revenue will grow by 3.4% annually over the next 3 years.

- The bullish analysts assume that profit margins will shrink from 28.2% today to 15.3% in 3 years time.

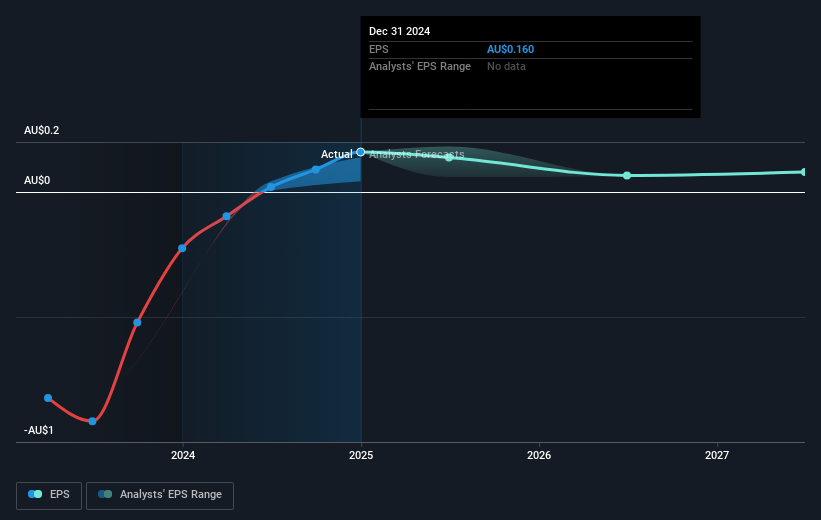

- The bullish analysts expect earnings to reach A$43.1 million (and earnings per share of A$0.09) by about July 2028, down from A$71.7 million today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the price target of the more bullish analyst cohort, the company would need to trade at a PE ratio of 41.4x on those 2028 earnings, up from 13.3x today. This future PE is lower than the current PE for the AU Software industry at 73.4x.

- Analysts expect the number of shares outstanding to remain consistent over the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 7.93%, as per the Simply Wall St company report.

Bravura Solutions Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The accelerating pace of digital disruption and automation in wealth management and superannuation could reduce the need for traditional, full-suite software platforms like Bravura's, putting recurring revenues at risk as clients seek more modern or modular alternatives.

- Bravura's lack of significant near-term investment or clear strategy around emerging technologies such as artificial intelligence risks them lagging behind agile fintech competitors, potentially eroding future market share and top-line revenue growth.

- The company's continued reliance on a limited number of large clients, highlighted by the material financial impact from the Fidelity International license transaction, exposes Bravura to revenue concentration risk and potential earnings volatility if key clients migrate or internalize solutions.

- Persistent challenges in transitioning existing clients from customized, legacy on-premises software to more standardized, cloud-based or configurable offerings could increase client churn, inhibit margin expansion, and create elevated R&D expenditure pressures on net earnings.

- Ongoing consolidation in client segments-such as global financial services and superannuation markets-may restrict Bravura's new customer growth opportunities and intensify pricing pressure, which can limit sustainable revenue expansion and compress profit margins over the long term.

Valuation

How have all the factors above been brought together to estimate a fair value?- The assumed bullish price target for Bravura Solutions is A$3.17, which is the highest price target estimate amongst analysts. This valuation is based on what can be assumed as the expectations of Bravura Solutions's future earnings growth, profit margins and other risk factors from analysts on the bullish end of the spectrum.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of A$3.17, and the most bearish reporting a price target of just A$2.15.

- In order for you to agree with the bullish analysts, you'd need to believe that by 2028, revenues will be A$281.6 million, earnings will come to A$43.1 million, and it would be trading on a PE ratio of 41.4x, assuming you use a discount rate of 7.9%.

- Given the current share price of A$2.12, the bullish analyst price target of A$3.17 is 33.1% higher. Despite analysts expecting the underlying buisness to decline, they seem to believe it's more valuable than what the market thinks.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

AnalystHighTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystHighTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystHighTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.