Key Takeaways

- Evolving regulatory demands and increased competition from agile fintechs are pressuring Bravura's profitability, market share, and revenue growth.

- Heavy reliance on large Australian clients amid industry consolidation increases revenue volatility and reduces competitive flexibility against global peers shifting to SaaS and cloud platforms.

- Bravura benefits from digital transformation, regulatory complexity, demographic trends, SaaS expansion, and international diversification, driving stable recurring revenues and improved margins.

Catalysts

About Bravura Solutions- Develops, licenses, and maintains administration and management software applications for the wealth management and funds administration sectors in Australia, the United Kingdom, New Zealand, and internationally.

- Bravura's exposure to intensifying regulatory scrutiny and mounting compliance obligations in global financial markets will likely force ongoing and significant investment in security and compliance infrastructure, which will result in sustained cost inflation and place downward pressure on both net margins and long-term profitability.

- The threat from new low-cost and agile fintech entrants with integrated all-in-one solutions and rapidly evolving cloud-native architectures is expected to erode Bravura's market share, compress software license fees, and drive down average contract values-damaging revenue growth prospects.

- Increasing industry consolidation among wealth managers and superannuation funds is forecast to shrink Bravura's addressable client base over time, heightening price competition and amplifying revenue volatility as larger clients gain greater negotiating power over contracts.

- Persistent customer concentration within the Australian wealth platform sector means that any client loss or renegotiation at lower rates could have an outsized negative impact on recurring revenue, further elevating earnings volatility and reducing visibility into future cash flows.

- Despite recent cost-out initiatives and margin improvements, Bravura risks lagging global peers in the pace of technological innovation and full SaaS/cloud migration; this could result in legacy products losing relevance, lower net margins, and declining competitiveness as client preferences accelerate toward platform flexibility and richer functionality.

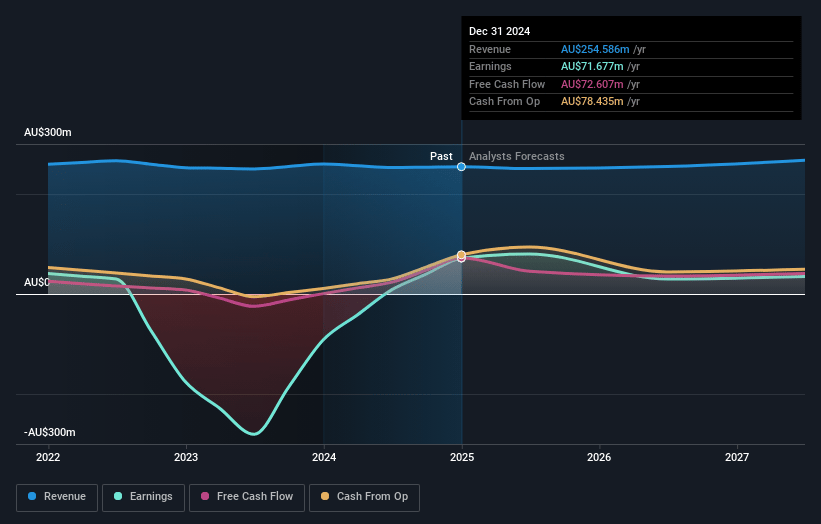

Bravura Solutions Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- This narrative explores a more pessimistic perspective on Bravura Solutions compared to the consensus, based on a Fair Value that aligns with the bearish cohort of analysts.

- The bearish analysts are assuming Bravura Solutions's revenue will grow by 3.4% annually over the next 3 years.

- The bearish analysts assume that profit margins will shrink from 28.2% today to 15.4% in 3 years time.

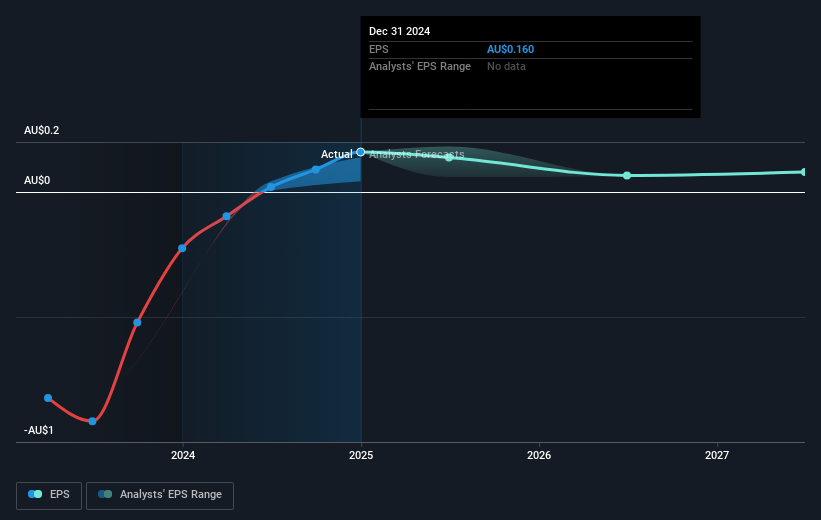

- The bearish analysts expect earnings to reach A$43.2 million (and earnings per share of A$0.09) by about July 2028, down from A$71.7 million today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the price target of the more bearish analyst cohort, the company would need to trade at a PE ratio of 28.0x on those 2028 earnings, up from 13.6x today. This future PE is lower than the current PE for the AU Software industry at 54.5x.

- Analysts expect the number of shares outstanding to remain consistent over the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 7.94%, as per the Simply Wall St company report.

Bravura Solutions Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The acceleration of digital transformation across financial services continues to drive demand for scalable, cloud-based wealth and fund administration platforms, directly supporting Bravura's potential for new client wins and contract expansion, which could result in top-line revenue growth well above bearish expectations.

- Rising regulatory complexity and compliance demands in global pensions, wealth management, and insurance are likely to sustain the need for advanced reporting and risk monitoring solutions, increasing Bravura's sales pipeline and client retention rates, thereby supporting stable or expanding recurring revenues.

- Demographic shifts, particularly aging populations and increased retirement savings assets, are set to fuel long-term demand for automated and integrated superannuation administration technology, forming a durable tailwind for Bravura's platform adoption and underpinning revenue stability and growth.

- Ongoing expansion of Bravura's SaaS and cloud-based product suite, along with investments to improve engineering quality and standardize offerings, are leading to higher recurring revenues and reduced implementation costs, which are already resulting in notable EBITDA margin improvement and could drive sustainable net margin expansion.

- Strategic moves in international markets, especially recent progress with digital advice solutions in APAC and successful client engagement in EMEA, increase geographic diversification and reduce customer concentration risk, supporting earnings resilience and potentially boosting long-term profitability.

Valuation

How have all the factors above been brought together to estimate a fair value?- The assumed bearish price target for Bravura Solutions is A$2.15, which represents the lowest price target estimate amongst analysts. This valuation is based on what can be assumed as the expectations of Bravura Solutions's future earnings growth, profit margins and other risk factors from analysts on the more bearish end of the spectrum.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of A$3.17, and the most bearish reporting a price target of just A$2.15.

- In order for you to agree with the bearish analysts, you'd need to believe that by 2028, revenues will be A$281.5 million, earnings will come to A$43.2 million, and it would be trading on a PE ratio of 28.0x, assuming you use a discount rate of 7.9%.

- Given the current share price of A$2.18, the bearish analyst price target of A$2.15 is 1.4% lower. The relatively low difference between the current share price and the analyst bearish price target indicates that the bearish analysts believe on average, the company is fairly priced.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

AnalystLowTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystLowTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystLowTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.