Key Takeaways

- Regulatory approvals and strategic partnerships are expanding market access for Penthrox, driving revenue growth and improved operational leverage in key markets.

- Increased demand for non-opioid pain relief, manufacturing efficiencies, and cost discipline are strengthening competitive positioning and supporting margin expansion.

- Heavy reliance on a single product, execution risks in new markets, and cost pressures threaten revenue growth and margin stability amidst regulatory and trade uncertainties.

Catalysts

About Medical Developments International- Manufactures and distributes emergency medical solutions in Australia, Asia, Europe, the United States, and internationally.

- The recent regulatory approval for the expanded pediatric indication of Penthrox across Europe is set to significantly broaden MVP's addressable market, enabling access to new patient populations and unlocking growth in key segments such as ambulance and emergency medicine – highly likely to accelerate top-line revenue and drive volume growth over the coming years.

- Increased penetration of Penthrox in hospital emergency departments in Australia, supported by inclusion in major state formularies (e.g., Queensland LAM) and strong procedural adoption, positions the company to capitalize on the ongoing rise in demand for acute pain management solutions as the population ages and healthcare utilization increases – expected to materially boost revenue and operational leverage.

- Strategic distribution partnerships in France and Switzerland with established players are anticipated to drive deeper market access and sustained double-digit volume growth, with long-term benefits from higher sales volumes and a lower cost-to-serve model enhancing group revenue and improving net margins as operational scale builds.

- Heightened global awareness and regulatory preference for non-opioid pain relief, as driven by the opioid crisis, strengthens MVP's competitive positioning and should underpin consistent demand tailwinds for Penthrox and new pipeline products – translating into resilient earnings growth and expanded international market share.

- Realization of manufacturing efficiency gains and disciplined cost base following FY '25 transformation means incremental revenue growth can fall through more directly to net profit, setting the stage for margin expansion and improved long-term earnings as volumes scale globally.

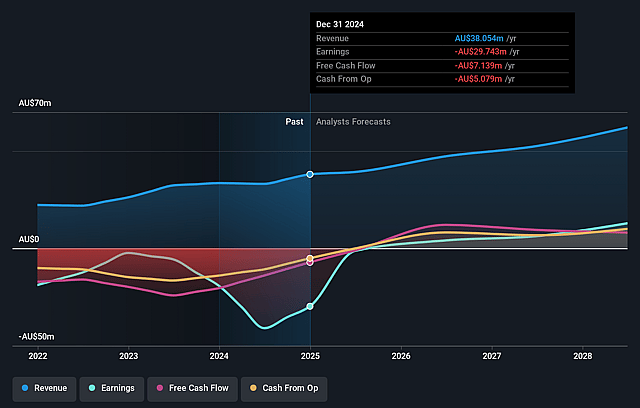

Medical Developments International Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Medical Developments International's revenue will grow by 11.8% annually over the next 3 years.

- Analysts assume that profit margins will increase from 0.2% today to 7.9% in 3 years time.

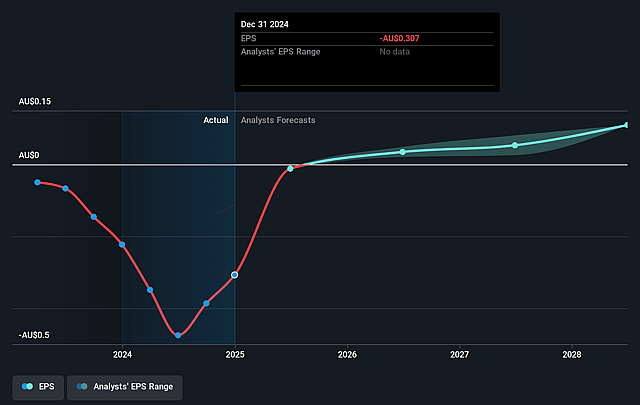

- Analysts expect earnings to reach A$4.3 million (and earnings per share of A$0.04) by about September 2028, up from A$94.0 thousand today. However, there is a considerable amount of disagreement amongst the analysts with the most bullish expecting A$7.4 million in earnings, and the most bearish expecting A$1.2 million.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 71.2x on those 2028 earnings, down from 695.1x today. This future PE is greater than the current PE for the AU Pharmaceuticals industry at 13.7x.

- Analysts expect the number of shares outstanding to remain consistent over the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 6.48%, as per the Simply Wall St company report.

Medical Developments International Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- Heavy reliance on Penthrox as the primary revenue driver creates concentration risk; if uptake stagnates due to competition, slower-than-expected behavioral adoption in hospitals, or emerging alternatives, it could cause revenue volatility and earnings risk.

- The company's expansion into new international markets, particularly Europe and the U.K., remains dependent on timely and successful regulatory approvals and smooth execution by new distribution partners; delays, post-market regulatory hurdles, or underperformance by partners could slow revenue growth and increase operating costs.

- The shift to a partner-distribution model in key European markets like France and Switzerland will result in near-term reductions in revenue and margins, while the expectation of higher long-term volumes introduces execution risk and relies on successful partner ramp-up (potentially impacting short-to-medium term profitability).

- Manufacturing scale and cost-efficiency improvements are crucial for long-term margin expansion; however, MVP's relatively limited scale compared to larger pharmaceutical peers could lead to persistently lower net margins, particularly if input costs rise or pricing pressures emerge in core markets.

- Increasing trade barriers, such as new tariffs in the U.S. for respiratory products, inject near-term uncertainty; if MVP cannot successfully pass these costs to customers, or if tariff regimes worsen, this could compress segment margins and negatively affect group earnings.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of A$2.265 for Medical Developments International based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of A$3.73, and the most bearish reporting a price target of just A$0.8.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be A$54.6 million, earnings will come to A$4.3 million, and it would be trading on a PE ratio of 71.2x, assuming you use a discount rate of 6.5%.

- Given the current share price of A$0.58, the analyst price target of A$2.26 is 74.4% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.