Key Takeaways

- Efficient project ramp-up and favorable gold market dynamics could drive substantial revenue and earnings growth beyond current market estimates.

- Strong ESG profile and disciplined financial management position the company for premium valuation and strategic growth through consolidation.

- Elevated capital spending, regulatory hurdles, cost pressures, and decarbonization risks threaten profitability, cash flow, and the long-term sustainability of revenues and valuation.

Catalysts

About Northern Star Resources- Engages in the exploration, development, mining, and processing of gold deposits.

- Analyst consensus anticipates steady growth from De Grey integration and KCGM expansion, but this likely understates the scale of operational leverage available as both projects ramp efficiently within a structurally higher gold price environment, pointing to a step-change in revenue and free cash flow that could outpace market expectations.

- While the consensus views near-term efficiency gains at KCGM as modest margin enhancers, the resolution of recent productivity issues and accelerated underground development point to the possibility of record production levels and materially higher EBITDA margins as high-grade ore contributions and expanded mill capacity coincide with a market undersupplied in gold.

- Northern Star's strong ESG credentials and position in low-risk jurisdictions are likely to attract a disproportionate share of global capital flows as institutional mandates and sustainability-focused investors increasingly favor tier-1 gold miners, setting the stage for higher valuation multiples and a lower cost of capital.

- The company's disciplined balance sheet, net cash position, and demonstrated technical integration capability set up for ongoing portfolio optimization and further large-scale, value-accretive M&A, with underappreciated optionality to accelerate top-line and EPS growth via consolidation as industry supply constraints worsen.

- Persistently high inflation, ongoing geopolitical risk, and the demonstrated supply discipline among global gold miners provide a rare macro backdrop where realized gold prices and demand can surprise to the upside, amplifying Northern Star's leverage to net margins and long-term earning power.

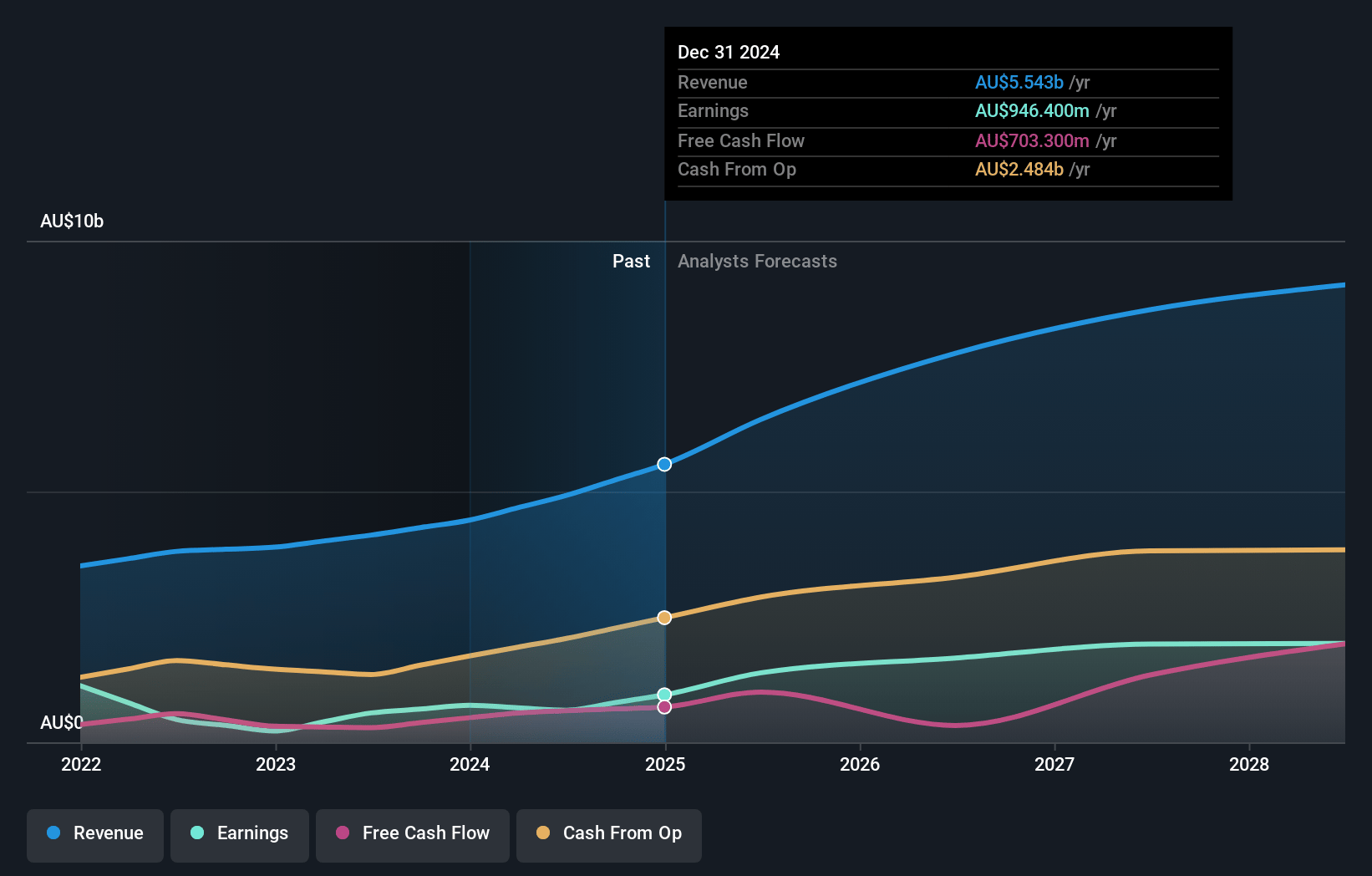

Northern Star Resources Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- This narrative explores a more optimistic perspective on Northern Star Resources compared to the consensus, based on a Fair Value that aligns with the bullish cohort of analysts.

- The bullish analysts are assuming Northern Star Resources's revenue will grow by 25.2% annually over the next 3 years.

- The bullish analysts assume that profit margins will increase from 17.1% today to 22.1% in 3 years time.

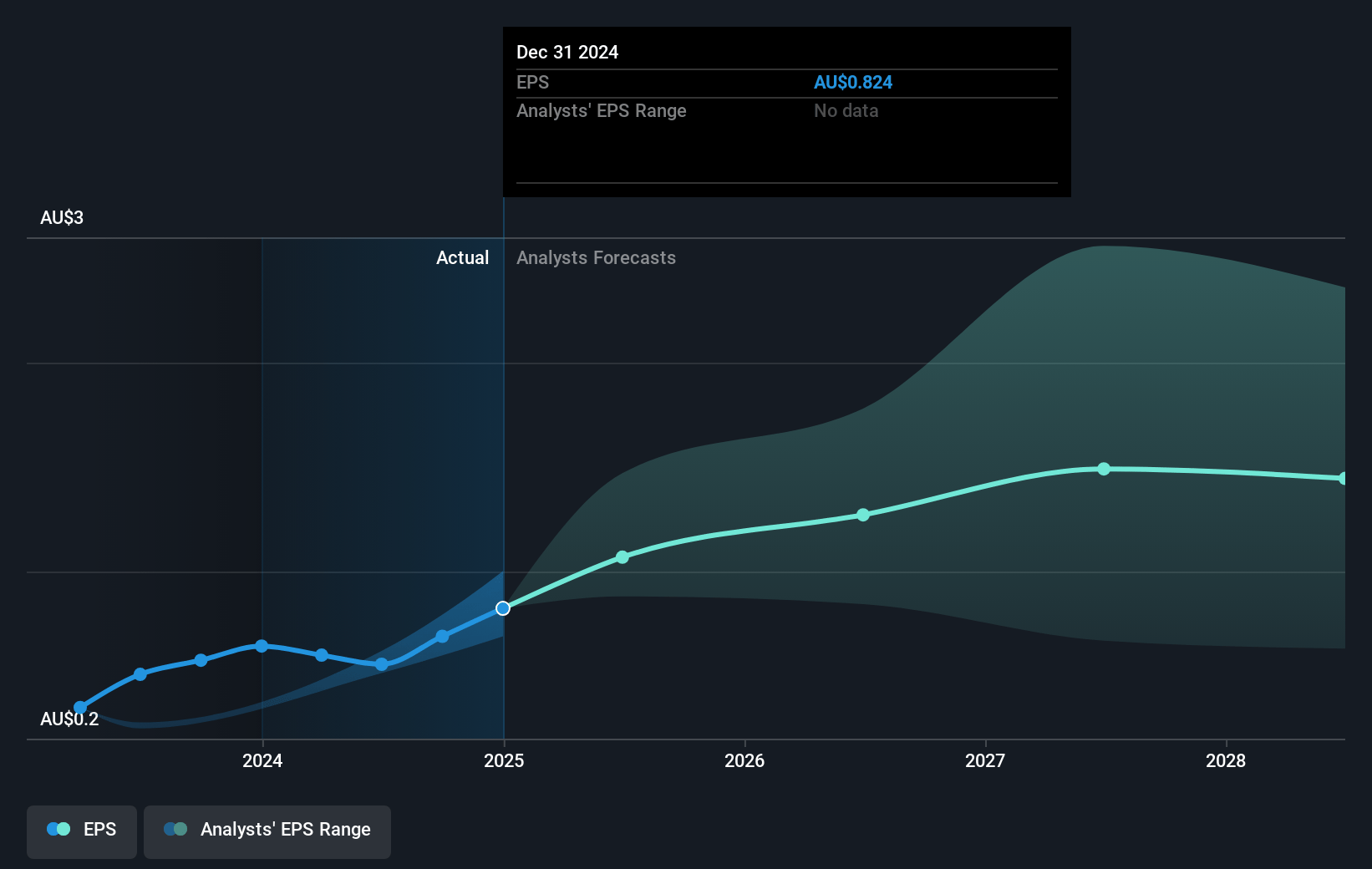

- The bullish analysts expect earnings to reach A$2.4 billion (and earnings per share of A$2.1) by about July 2028, up from A$946.4 million today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the price target of the more bullish analyst cohort, the company would need to trade at a PE ratio of 19.5x on those 2028 earnings, down from 24.5x today. This future PE is greater than the current PE for the AU Metals and Mining industry at 13.3x.

- Analysts expect the number of shares outstanding to decline by 0.41% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 7.14%, as per the Simply Wall St company report.

Northern Star Resources Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- Substantial growth capital expenditures, including $500 million to $530 million for the KCGM mill expansion and up to $1.1 billion for the broader portfolio, may elevate financial leverage and increase depreciation charges over time, which could constrain future free cash flow and suppress net earnings.

- Revised group production guidance, stemming from operational challenges and delayed access to high-grade ore at KCGM, points to ongoing risks from mine grade deterioration or reserve depletion, raising concerns about the sustainability of future revenues.

- Tightening environmental permitting processes, as evidenced by the necessity for state and federal approvals for projects like Hemi, introduce the risk of regulatory delays and increased compliance costs, which could lead to costly project deferrals and erode operating margins.

- Rising all-in sustaining costs, influenced by factors such as higher maintenance expenses, increased royalties, and cost fluctuations in remote operations, threaten to squeeze EBITDA margins and overall profitability, particularly if gold prices moderate from current historical highs.

- Accelerating global decarbonization and the shift toward ESG investing could restrict future institutional capital flows, elevate the company's cost of capital, and reduce industry-wide investment demand for gold, which in turn poses long-term downward pressure on both valuation and revenue generation.

Valuation

How have all the factors above been brought together to estimate a fair value?- The assumed bullish price target for Northern Star Resources is A$27.0, which is the highest price target estimate amongst analysts. This valuation is based on what can be assumed as the expectations of Northern Star Resources's future earnings growth, profit margins and other risk factors from analysts on the bullish end of the spectrum.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of A$27.0, and the most bearish reporting a price target of just A$13.0.

- In order for you to agree with the bullish analysts, you'd need to believe that by 2028, revenues will be A$10.9 billion, earnings will come to A$2.4 billion, and it would be trading on a PE ratio of 19.5x, assuming you use a discount rate of 7.1%.

- Given the current share price of A$16.25, the bullish analyst price target of A$27.0 is 39.8% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

AnalystHighTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystHighTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystHighTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.