Key Takeaways

- Rebranding to Quality Value targets broader market opportunities and increased revenue through expanded client interest in value branding.

- New strategic investments in Abu Dhabi and PCS expansion enhance diversity, revenue growth, and operational efficiency.

- Potential revenue and earnings instability arise from market shifts, geopolitical risks, net outflows, and strategic transitions in investment products.

Catalysts

About GQG Partners- Operates as a boutique asset management company worldwide.

- The rebranding of their Quality Dividend Income strategies to Quality Value aligns with market opportunities for value products that are substantially larger. This strategic shift is expected to drive significant growth and increase revenues by capturing a wider client base interested in value branding.

- The establishment and expansion of operations in Abu Dhabi are set to provide access to a global talent pool, drive operational efficiencies, and open new investment avenues, which can contribute to long-term revenue growth.

- The first acquisition and development of the Private Client Services (PCS) business, with robust current performance and a strong deal pipeline, are positioned to provide significant additional revenue streams and diversification for GQG Partners.

- There is a focus on strengthening the wholesale distribution channel, which has shown strong growth globally, especially in the U.S. and other international markets, potentially driving net sales and revenue expansion.

- The introduction of new strategic investments, such as the development of the Middle East operations and further integration of PCS assets, aims to enhance operational capabilities and leverage new markets, which could improve earnings and operational margins.

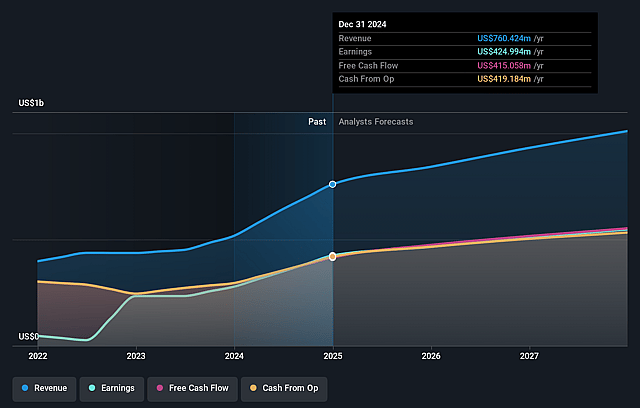

GQG Partners Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming GQG Partners's revenue will grow by 9.0% annually over the next 3 years.

- Analysts assume that profit margins will shrink from 55.9% today to 53.3% in 3 years time.

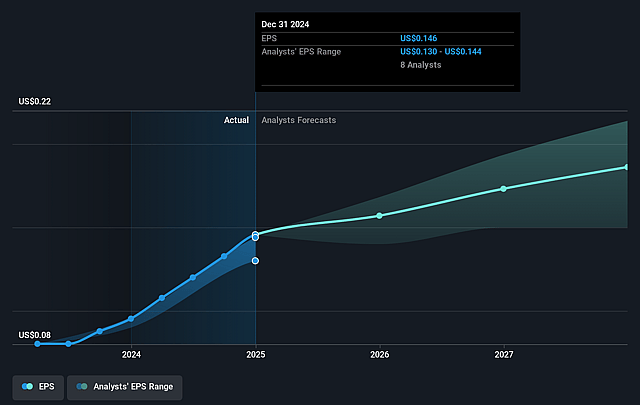

- Analysts expect earnings to reach $525.7 million (and earnings per share of $0.18) by about August 2028, up from $425.0 million today. However, there is a considerable amount of disagreement amongst the analysts with the most bullish expecting $626.0 million in earnings, and the most bearish expecting $379.6 million.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 12.8x on those 2028 earnings, up from 7.8x today. This future PE is lower than the current PE for the AU Capital Markets industry at 16.3x.

- Analysts expect the number of shares outstanding to grow by 0.06% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 8.07%, as per the Simply Wall St company report.

GQG Partners Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The forward-looking statements made by GQG Partners are inherently uncertain and susceptible to change, which may impact the reliability of their future revenue and earnings projections.

- The company's net flows could be adversely affected by a shift in asset allocation trends, as exemplified by the Q4 movement from non-U.S. to U.S. equity, potentially impacting future revenue and earnings.

- There is a noted trend of consecutive net outflows in the institutional business over multiple quarters, which may indicate maturity or saturation and could impede revenue growth.

- Potential geopolitical risks, like changing investment climates or regulatory shifts (e.g., ESG emphasis changes), could impact fund flows and revenue, particularly in regions like Europe.

- The repositioning and rebranding of investment strategies (such as Quality Dividend Income to Quality Value) might face client resistance or confusion impacting revenue and net margins during the transition phase.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of A$2.756 for GQG Partners based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of A$3.6, and the most bearish reporting a price target of just A$1.8.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be $986.0 million, earnings will come to $525.7 million, and it would be trading on a PE ratio of 12.8x, assuming you use a discount rate of 8.1%.

- Given the current share price of A$1.72, the analyst price target of A$2.76 is 37.6% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.