Last Update01 May 25Fair value Decreased 4.76%

Key Takeaways

- Strategic investments and asset consolidation are expected to enhance liquidity, integrated offerings, and profitability through increased revenues and stable operations.

- Cost-saving initiatives and improved customer management could boost net margins and revenue growth by regaining market share and promoting safer gambling environments.

- Regulatory challenges and compliance costs are undermining revenue, profitability, and financial stability, amid threats from litigation and the need for strategic investments.

Catalysts

About Star Entertainment Group- Operates and manages integrated resorts in Australia.

- The $300 million strategic investment from Bally's Corporation and Investment Holdings provides The Star with critical liquidity, expected to give the company financial stability to pursue revenue initiatives and improve operations over the medium term. This will potentially impact revenue and earnings positively.

- The transaction to exit the Destination Brisbane Consortium and consolidate assets on the Gold Coast is expected to enhance The Star's fully integrated offering in the area, which could drive higher future revenues and profitability.

- The focus on cost-saving initiatives, targeting a $100 million reduction in costs, is expected to improve The Star's net margins and overall profitability once these savings are fully realized and additional cost-out opportunities are identified.

- The emphasis on regaining market share and reactivating customers through improved customer management and nongaming experiences may lead to an increase in gaming and nongaming revenues, positively impacting overall revenue growth.

- The ongoing dialogue with regulators to achieve a safer gambling environment and potential future level playing field across competitors could restore market share and revenue levels, contributing positively to future revenue growth.

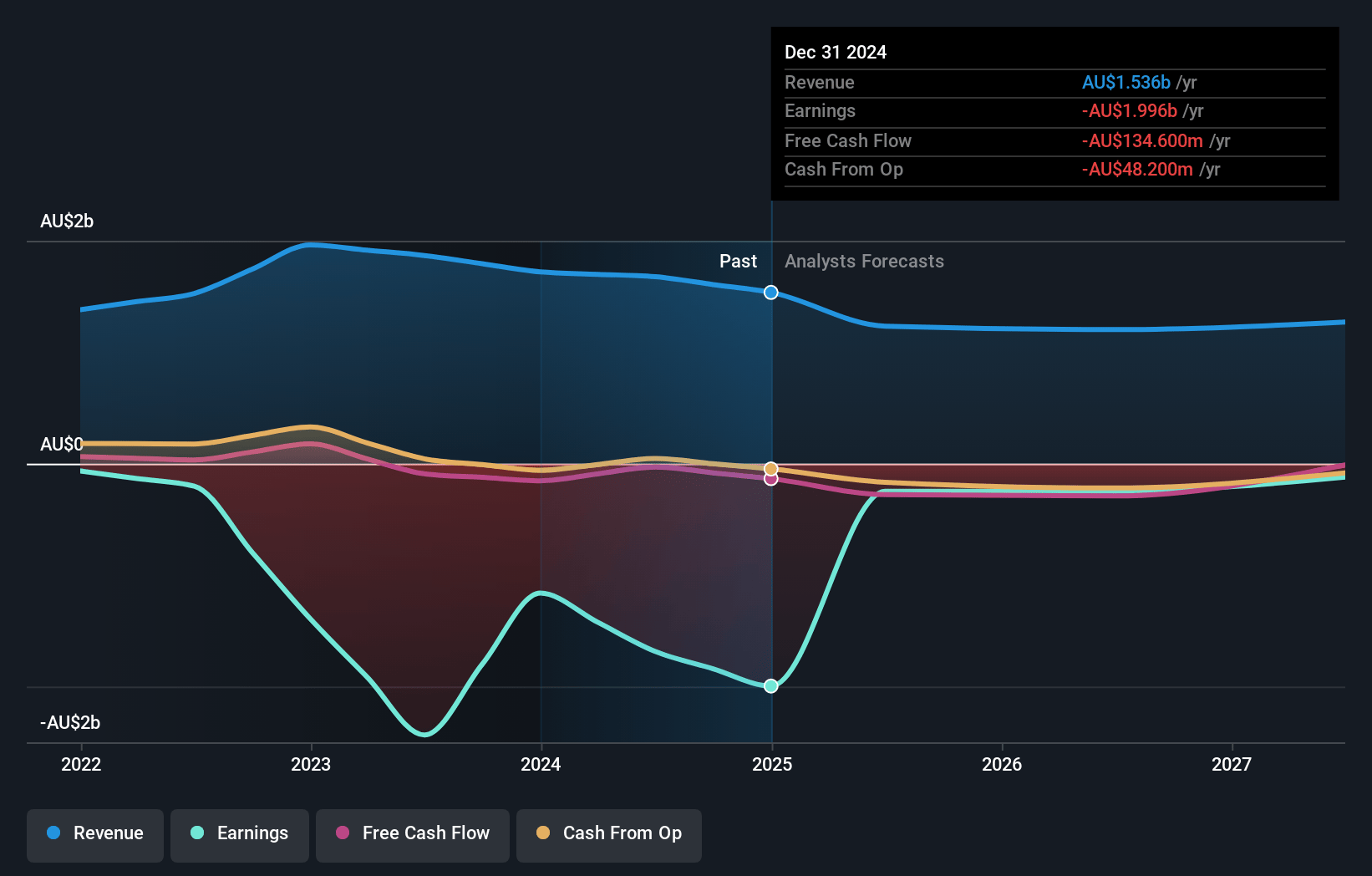

Star Entertainment Group Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Star Entertainment Group's revenue will decrease by 5.6% annually over the next 3 years.

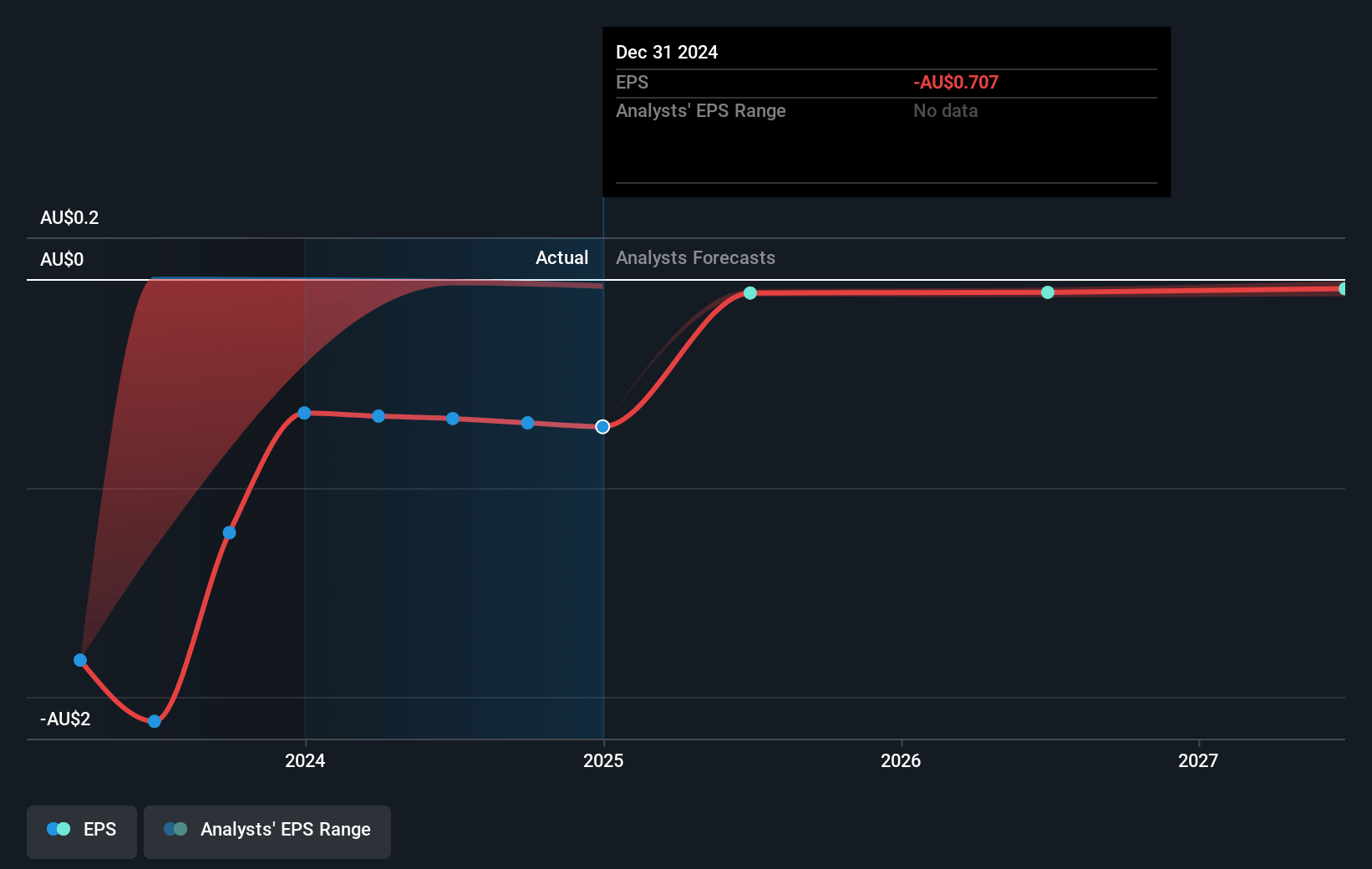

- Analysts are not forecasting that Star Entertainment Group will become profitable in next 3 years. To represent the Analyst Price Target as a Future PE Valuation we will estimate Star Entertainment Group's profit margin will increase from -129.9% to the average AU Hospitality industry of 8.2% in 3 years.

- If Star Entertainment Group's profit margin were to converge on the industry average, you could expect earnings to reach A$105.2 million (and earnings per share of A$0.04) by about May 2028, up from A$-2.0 billion today.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 5.0x on those 2028 earnings, up from -0.2x today. This future PE is lower than the current PE for the AU Hospitality industry at 20.7x.

- Analysts expect the number of shares outstanding to remain consistent over the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 10.91%, as per the Simply Wall St company report.

Star Entertainment Group Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The ongoing impact of regulatory reforms, including mandatory carded play and cash limits, has resulted in a significant loss of market share and decline in gaming revenues, impacting overall earnings.

- The company continues to operate in a challenging trading environment with elevated operating expenses due to compliance and transformation activities, negatively affecting net margins.

- The Star recorded an EBITDA loss due to decreased revenue and increased costs, reflecting negative operating leverage and threatening future profitability.

- The suspension of The Star's casino licenses and ongoing litigation, including unresolved penalties from AUSTRAC proceedings, pose financial risks and uncertainty that could further harm earnings.

- The requirement for significant strategic investments and asset sales to maintain liquidity suggests potential financial instability, impacting the company's long-term revenue growth and financial health.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of A$0.133 for Star Entertainment Group based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of A$0.2, and the most bearish reporting a price target of just A$0.09.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be A$1.3 billion, earnings will come to A$105.2 million, and it would be trading on a PE ratio of 5.0x, assuming you use a discount rate of 10.9%.

- Given the current share price of A$0.1, the analyst price target of A$0.13 is 21.2% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.