Key Takeaways

- Digital challengers and regulatory pressures threaten market share and revenue growth, while high compliance costs and operational risks will erode profitability.

- Overreliance on domestic mortgages and a slowing, aging population limit growth opportunities, creating heightened vulnerability to housing downturns and stagnant credit demand.

- Robust demand, digital innovation, and strong customer relationships reinforce CBA's dominant market position and earnings resilience, supported by conservative balance sheet and regulatory advantages.

Catalysts

About Commonwealth Bank of Australia- Provides retail and commercial banking services in Australia, New Zealand, and internationally.

- The relentless advance of fintechs, neobanks and digital payment platforms is intensifying digital disruption, which threatens to erode Commonwealth Bank of Australia's traditional banking market share and stifle future revenue growth despite heavy investments in technology.

- CBA's overdependence on domestic mortgage lending heightens sensitivity to even moderate residential property downturns or regulatory tightening, putting future earnings and asset growth at significant risk if a housing market correction or regulatory intervention occurs.

- The growing impact of an aging Australian population combined with slower population growth means demand for credit products is likely to stagnate or fall, while provisions for bad debts will need to trend higher, both dampening long-term loan book and net interest income expansion.

- Persistent market saturation, especially in Australia's mature retail and business banking sectors, means CBA has fewer viable avenues for organic growth; as a result, increases in revenue will be constrained and barriers to expanding average revenue per customer will mount.

- Escalating compliance costs as ESG and regulatory requirements for lending, climate risk management, and customer protection tighten will erode net margins in the coming years, aggravating cost growth and diminishing CBA's profitability even if topline revenues remain stable.

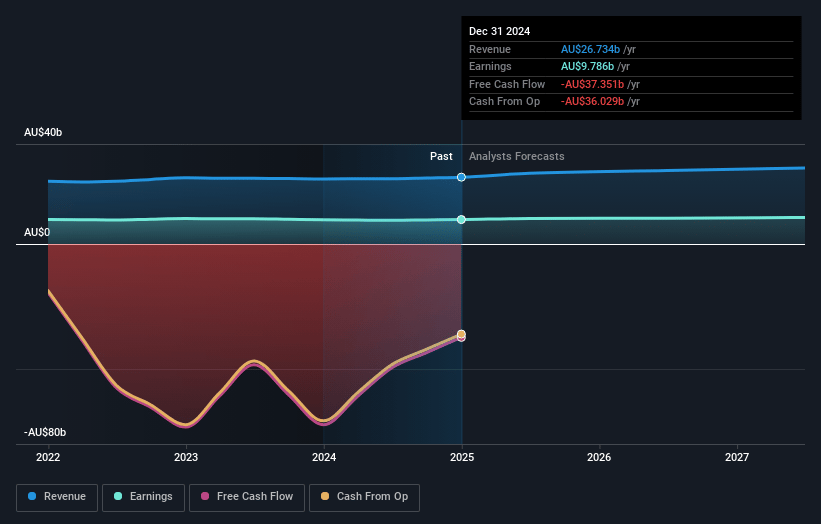

Commonwealth Bank of Australia Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- This narrative explores a more pessimistic perspective on Commonwealth Bank of Australia compared to the consensus, based on a Fair Value that aligns with the bearish cohort of analysts.

- The bearish analysts are assuming Commonwealth Bank of Australia's revenue will grow by 4.9% annually over the next 3 years.

- The bearish analysts assume that profit margins will shrink from 36.6% today to 34.8% in 3 years time.

- The bearish analysts expect earnings to reach A$10.7 billion (and earnings per share of A$6.41) by about July 2028, up from A$9.8 billion today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the price target of the more bearish analyst cohort, the company would need to trade at a PE ratio of 18.9x on those 2028 earnings, down from 30.3x today. This future PE is greater than the current PE for the AU Banks industry at 15.2x.

- Analysts expect the number of shares outstanding to remain consistent over the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 7.62%, as per the Simply Wall St company report.

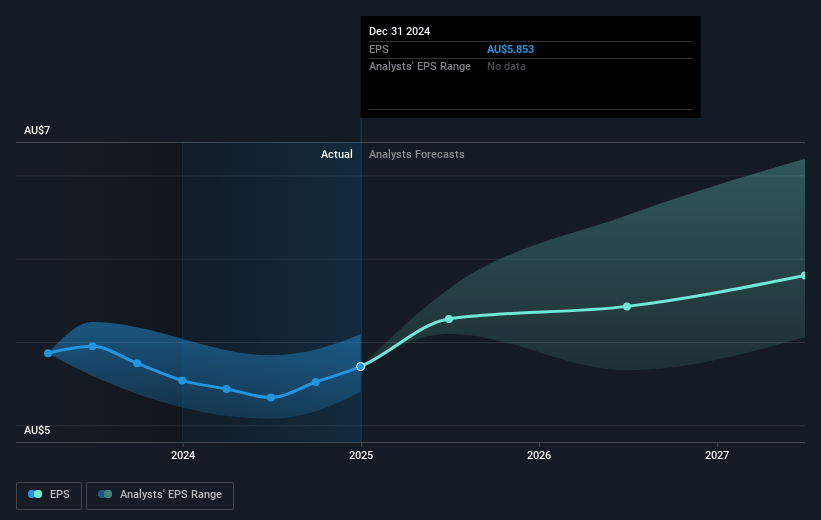

Commonwealth Bank of Australia Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- Sustained population growth, urbanization, and business formation in Australia are likely to underpin ongoing demand for mortgages, retail banking, and business lending, which supports Commonwealth Bank of Australia's revenue and loan book expansion in the long term.

- The bank's accelerated investments in digital technology, artificial intelligence, and modernization of its technology stack enable improvements in operational efficiency, customer engagement, and risk management, contributing to improved net margins and earnings resilience.

- CBA's market-leading customer experience, high Net Promoter Scores, and deepening of both retail and business main financial institution relationships facilitate effective cross-selling and product innovation, which could boost average revenue per customer and support earnings growth.

- The group's strong capital position, conservative balance sheet settings, and stable deposit funding base allow for disciplined lending growth and capacity to fund strategic acquisitions, underpinning the sustainability of returns on equity and higher dividend payouts.

- Industry consolidation, high barriers to entry, and stricter regulatory oversight on new entrants favor major incumbents like CBA, helping maintain its dominant market share and pricing power, which protect long-term revenue and profitability.

Valuation

How have all the factors above been brought together to estimate a fair value?- The assumed bearish price target for Commonwealth Bank of Australia is A$97.49, which represents the lowest price target estimate amongst analysts. This valuation is based on what can be assumed as the expectations of Commonwealth Bank of Australia's future earnings growth, profit margins and other risk factors from analysts on the more bearish end of the spectrum.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of A$143.0, and the most bearish reporting a price target of just A$97.49.

- In order for you to agree with the bearish analysts, you'd need to believe that by 2028, revenues will be A$30.9 billion, earnings will come to A$10.7 billion, and it would be trading on a PE ratio of 18.9x, assuming you use a discount rate of 7.6%.

- Given the current share price of A$177.57, the bearish analyst price target of A$97.49 is 82.2% lower. Despite analysts expecting the underlying buisness to improve, they seem to believe the market's expectations are too high.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

AnalystLowTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystLowTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystLowTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.