Advertisement

- South Africa

- /

- Specialty Stores

- /

- JSE:ITE

Investors Shouldn't Overlook The Favourable Returns On Capital At Italtile (JSE:ITE)

If we want to find a potential multi-bagger, often there are underlying trends that can provide clues. Firstly, we'd want to identify a growing return on capital employed (ROCE) and then alongside that, an ever-increasing base of capital employed. Basically this means that a company has profitable initiatives that it can continue to reinvest in, which is a trait of a compounding machine. Ergo, when we looked at the ROCE trends at Italtile (JSE:ITE), we liked what we saw.

Understanding Return On Capital Employed (ROCE)

If you haven't worked with ROCE before, it measures the 'return' (pre-tax profit) a company generates from capital employed in its business. The formula for this calculation on Italtile is:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

0.26 = R2.3b ÷ (R9.8b - R935m) (Based on the trailing twelve months to June 2023).

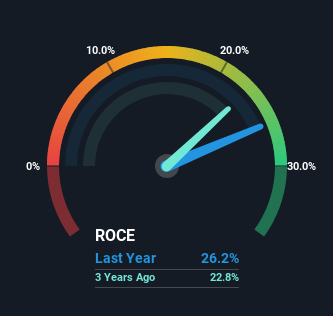

Thus, Italtile has an ROCE of 26%. That's a fantastic return and not only that, it outpaces the average of 13% earned by companies in a similar industry.

Check out our latest analysis for Italtile

Historical performance is a great place to start when researching a stock so above you can see the gauge for Italtile's ROCE against it's prior returns. If you want to delve into the historical earnings, revenue and cash flow of Italtile, check out these free graphs here.

How Are Returns Trending?

It's hard not to be impressed by Italtile's returns on capital. The company has consistently earned 26% for the last five years, and the capital employed within the business has risen 56% in that time. With returns that high, it's great that the business can continually reinvest its money at such appealing rates of return. If these trends can continue, it wouldn't surprise us if the company became a multi-bagger.

The Key Takeaway

In the end, the company has proven it can reinvest it's capital at high rates of returns, which you'll remember is a trait of a multi-bagger. And given the stock has only risen 3.2% over the last five years, we'd suspect the market is beginning to recognize these trends. So to determine if Italtile is a multi-bagger going forward, we'd suggest digging deeper into the company's other fundamentals.

If you want to continue researching Italtile, you might be interested to know about the 1 warning sign that our analysis has discovered.

High returns are a key ingredient to strong performance, so check out our free list ofstocks earning high returns on equity with solid balance sheets.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About JSE:ITE

Italtile

Manufactures, retails, and franchises tiles, bathroom ware, and related home-finishing products in South Africa, rest of Africa, and Australia.

Flawless balance sheet, good value and pays a dividend.

Market Insights

Advertisement

Community Narratives

Vita Life Sciences Set for a 12.72% Revenue Growth While Tackling Operational Challenges

Fair Value AU$2.42|8.7% undervalued

RO

Community Contributor

Vossloh rides a €500 billion wave to boost growth and earnings in the next decade

Fair Value €78.41|6.3% undervalued

CH

Community Contributor

Intuitive Surgical Will Transform Healthcare with 12% Revenue Growth

Fair Value US$325.55|56.5% overvalued

UN

Community Contributor