Advertisement

- South Africa

- /

- Specialty Stores

- /

- JSE:HIL

HomeChoice International's (JSE:HIL) Shareholders Will Receive A Bigger Dividend Than Last Year

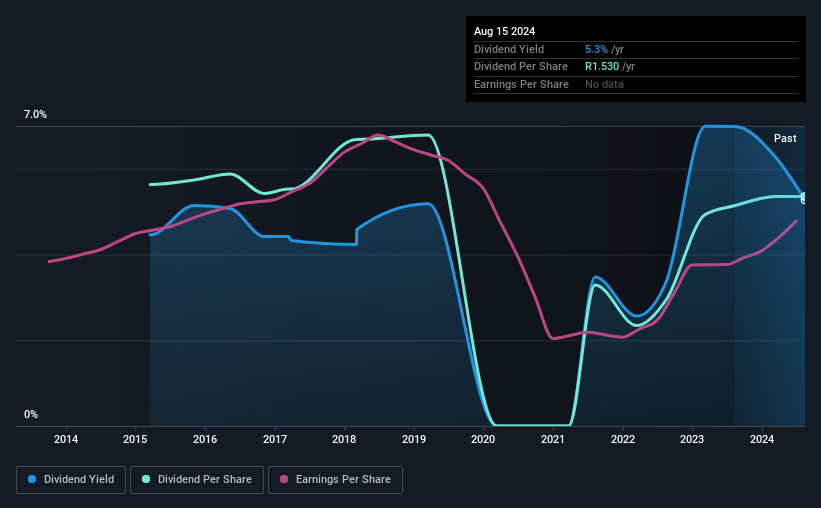

The board of HomeChoice International plc (JSE:HIL) has announced that the dividend on 9th of September will be increased to ZAR0.95, which will be 36% higher than last year's payment of ZAR0.70 which covered the same period. This will take the dividend yield to an attractive 5.3%, providing a nice boost to shareholder returns.

Check out our latest analysis for HomeChoice International

HomeChoice International's Payment Has Solid Earnings Coverage

A big dividend yield for a few years doesn't mean much if it can't be sustained. Prior to this announcement, HomeChoice International's earnings easily covered the dividend, but free cash flows were negative. Since a dividend means the company is paying out cash to investors, this could prove to be a problem in the future.

EPS is set to fall by 5.3% over the next 12 months if recent trends continue. If the dividend continues along the path it has been on recently, we estimate the payout ratio could be 49%, which is definitely feasible to continue.

HomeChoice International's Dividend Has Lacked Consistency

Even in its relatively short history, the company has reduced the dividend at least once. This suggests that the dividend might not be the most reliable. Since 2015, the annual payment back then was ZAR1.61, compared to the most recent full-year payment of ZAR1.53. Payments have been decreasing at a very slow pace in this time period. Generally, we don't like to see a dividend that has been declining over time as this can degrade shareholders' returns and indicate that the company may be running into problems.

Dividend Growth May Be Hard To Come By

Growing earnings per share could be a mitigating factor when considering the past fluctuations in the dividend. HomeChoice International has seen earnings per share falling at 5.3% per year over the last five years. If earnings continue declining, the company may have to make the difficult choice of reducing the dividend or even stopping it completely - the opposite of dividend growth.

The Dividend Could Prove To Be Unreliable

Overall, this is probably not a great income stock, even though the dividend is being raised at the moment. While the low payout ratio is a redeeming feature, this is offset by the minimal cash to cover the payments. This company is not in the top tier of income providing stocks.

It's important to note that companies having a consistent dividend policy will generate greater investor confidence than those having an erratic one. However, there are other things to consider for investors when analysing stock performance. Case in point: We've spotted 3 warning signs for HomeChoice International (of which 2 don't sit too well with us!) you should know about. If you are a dividend investor, you might also want to look at our curated list of high yield dividend stocks.

Valuation is complex, but we're here to simplify it.

Discover if HomeChoice International might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About JSE:HIL

HomeChoice International

Operates as an omni-channel retailer in South Africa.

Moderate with proven track record.

Market Insights

Advertisement

Community Narratives

Groundbreaking therapies that could change the treatment landscape for PTSD, fibromyalgia, MS & Alzheimer’s

Fair Value US$6.20|86.9% undervalued

CM

Community Contributor

DigitalOcean Will Grow 14% by Embracing AI with Paperspace Acquisition

Fair Value US$50.00|42.8% undervalued

NE

Community Contributor

Viant Technology: A Rising AdTech Challenger in the AI-Powered CTV Market

Fair Value US$38.61|66.0% undervalued

BL

Community Contributor

Volvo will Accelerate Forward into Electric and Autonomous Leadership in Five Years

Fair Value SEK 438.80|40.8% undervalued

UN

Community Contributor