Advertisement

- South Africa

- /

- Real Estate

- /

- JSE:PPR

Statutory Profit Doesn't Reflect How Good Putprop's (JSE:PPR) Earnings Are

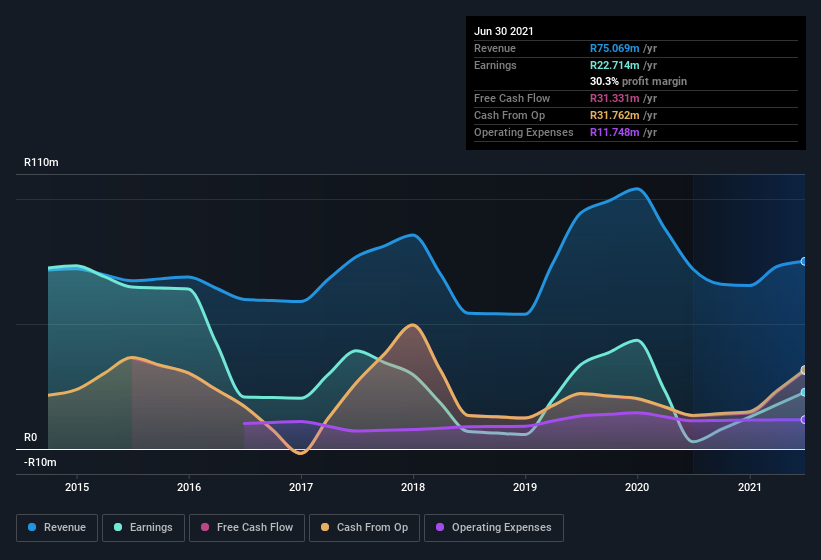

When companies post strong earnings, the stock generally performs well, just like Putprop Limited's (JSE:PPR) stock has recently. Our analysis found some more factors that we think are good for shareholders.

View our latest analysis for Putprop

Operating Revenue Or Not?

Companies will classify their revenue streams as either operating revenue or other revenue. Generally speaking, operating revenue is a more reliable guide to the sustainable revenue generating capacity of the business. Importantly, the non-operating revenue often comes without associated ongoing costs, so it can boost profit by letting it fall straight to the bottom line, making the operating business seem better than it really is. Notably, Putprop had a significant increase in non-operating revenue over the last year. In fact, our data indicates that non-operating revenue increased from -R1.87m to R1.99m. The high levels of non-operating revenue are problematic because if (and when) they do not repeat, then overall revenue (and profitability) of the firm will fall. Sometimes, you can get a better idea of the underlying earnings potential of a company by excluding unusual boosts to non-operating revenue.

Note: we always recommend investors check balance sheet strength. Click here to be taken to our balance sheet analysis of Putprop.

How Do Unusual Items Influence Profit?

Alongside that spike in non-operating revenue, it's also important to note that Putprop'sprofit suffered from unusual items, which reduced profit by R15m in the last twelve months. It's never great to see unusual items costing the company profits, but on the upside, things might improve sooner rather than later. We looked at thousands of listed companies and found that unusual items are very often one-off in nature. And, after all, that's exactly what the accounting terminology implies. If Putprop doesn't see those unusual expenses repeat, then all else being equal we'd expect its profit to increase over the coming year.

Our Take On Putprop's Profit Performance

In its last report Putprop benefitted from a spike in non-operating revenue which may have boosted its profit in a way that may be no more sustainable than low quality coal mining. But on the other hand, it also saw an unusual item depress its profit, suggesting the statutory profit number will actually improve next year, if the unusual expenses are not repeated, and all else stays equal. After taking into account all these factors, we think that Putprop's statutory results are a decent reflection of its underlying earnings power. If you'd like to know more about Putprop as a business, it's important to be aware of any risks it's facing. Every company has risks, and we've spotted 7 warning signs for Putprop (of which 2 are a bit unpleasant!) you should know about.

In this article we've looked at a number of factors that can impair the utility of profit numbers, as a guide to a business. But there is always more to discover if you are capable of focussing your mind on minutiae. Some people consider a high return on equity to be a good sign of a quality business. While it might take a little research on your behalf, you may find this free collection of companies boasting high return on equity, or this list of stocks that insiders are buying to be useful.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About JSE:PPR

Proven track record with slight risk.

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60.00|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|1.3% undervalued

TI

Community Contributor