Advertisement

- South Africa

- /

- Metals and Mining

- /

- JSE:KIO

Kumba Iron Ore Limited's (JSE:KIO) Popularity With Investors Is Under Threat From Overpricing

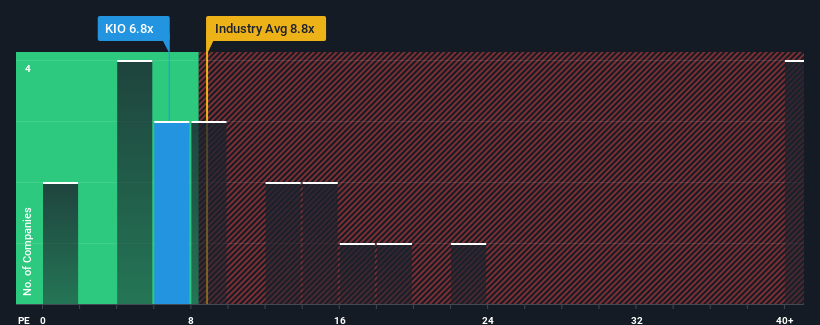

It's not a stretch to say that Kumba Iron Ore Limited's (JSE:KIO) price-to-earnings (or "P/E") ratio of 6.8x right now seems quite "middle-of-the-road" compared to the market in South Africa, where the median P/E ratio is around 9x. Although, it's not wise to simply ignore the P/E without explanation as investors may be disregarding a distinct opportunity or a costly mistake.

Kumba Iron Ore certainly has been doing a good job lately as it's been growing earnings more than most other companies. It might be that many expect the strong earnings performance to wane, which has kept the P/E from rising. If you like the company, you'd be hoping this isn't the case so that you could potentially pick up some stock while it's not quite in favour.

Check out our latest analysis for Kumba Iron Ore

What Are Growth Metrics Telling Us About The P/E?

The only time you'd be comfortable seeing a P/E like Kumba Iron Ore's is when the company's growth is tracking the market closely.

Taking a look back first, we see that the company grew earnings per share by an impressive 52% last year. Still, EPS has barely risen at all from three years ago in total, which is not ideal. So it appears to us that the company has had a mixed result in terms of growing earnings over that time.

Looking ahead now, EPS is anticipated to slump, contracting by 12% each year during the coming three years according to the eleven analysts following the company. That's not great when the rest of the market is expected to grow by 12% each year.

With this information, we find it concerning that Kumba Iron Ore is trading at a fairly similar P/E to the market. It seems most investors are hoping for a turnaround in the company's business prospects, but the analyst cohort is not so confident this will happen. Only the boldest would assume these prices are sustainable as these declining earnings are likely to weigh on the share price eventually.

The Bottom Line On Kumba Iron Ore's P/E

Using the price-to-earnings ratio alone to determine if you should sell your stock isn't sensible, however it can be a practical guide to the company's future prospects.

We've established that Kumba Iron Ore currently trades on a higher than expected P/E for a company whose earnings are forecast to decline. When we see a poor outlook with earnings heading backwards, we suspect share price is at risk of declining, sending the moderate P/E lower. Unless these conditions improve, it's challenging to accept these prices as being reasonable.

It is also worth noting that we have found 3 warning signs for Kumba Iron Ore (1 is a bit unpleasant!) that you need to take into consideration.

Of course, you might find a fantastic investment by looking at a few good candidates. So take a peek at this free list of companies with a strong growth track record, trading on a low P/E.

Valuation is complex, but we're here to simplify it.

Discover if Kumba Iron Ore might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About JSE:KIO

Kumba Iron Ore

Engages in the exploration, extraction, beneficiation, marketing, sale, and shipping of iron ore for the steel industry in South Africa.

Flawless balance sheet established dividend payer.

Similar Companies

Market Insights

Advertisement

Community Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|11.0% undervalued

BE

Community Contributor

Procter & Gamble: A Dividend Giant Facing Slowing Growth

Fair Value US$119.81|23.3% overvalued

AN

Community Contributor

Eli Lilly's Future Growth Driven by Tirzepatide and Favorable Market Conditions

Fair Value US$1.19k|13.8% undervalued

EA

Community Contributor