Advertisement

- South Africa

- /

- Metals and Mining

- /

- JSE:KIO

Kumba Iron Ore Limited (JSE:KIO) Analysts Just Trimmed Their Revenue Forecasts By 14%

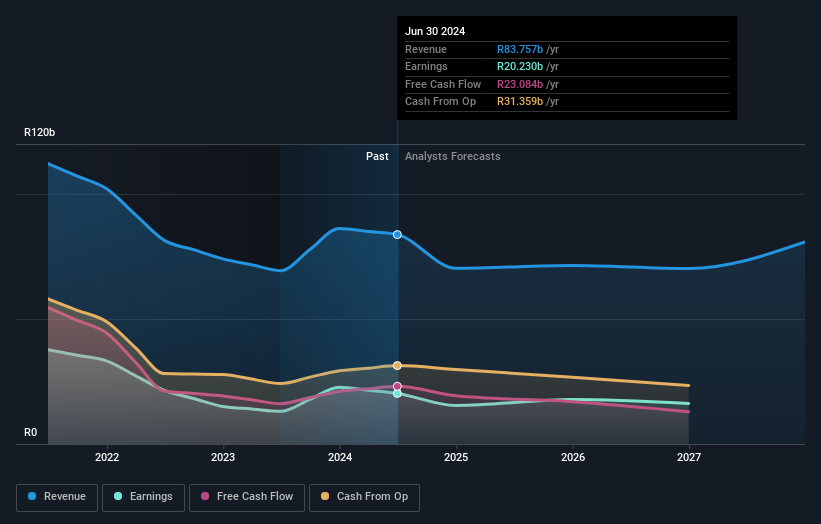

The analysts covering Kumba Iron Ore Limited (JSE:KIO) delivered a dose of negativity to shareholders today, by making a substantial revision to their statutory forecasts for this year. This report focused on revenue estimates, and it looks as though the consensus view of the business has become substantially more conservative.

Following the latest downgrade, the ten analysts covering Kumba Iron Ore provided consensus estimates of R61b revenue in 2025, which would reflect a disturbing 27% decline on its sales over the past 12 months. Before the latest update, the analysts were foreseeing R72b of revenue in 2025. The consensus view seems to have become more pessimistic on Kumba Iron Ore, noting the substantial drop in revenue estimates in this update.

See our latest analysis for Kumba Iron Ore

There was no particular change to the consensus price target of R374, with Kumba Iron Ore's latest outlook seemingly not enough to result in a change of valuation.

Looking at the bigger picture now, one of the ways we can make sense of these forecasts is to see how they measure up against both past performance and industry growth estimates. These estimates imply that sales are expected to slow, with a forecast annualised revenue decline of 27% by the end of 2025. This indicates a significant reduction from annual growth of 4.0% over the last five years. Compare this with our data, which suggests that other companies in the same industry are, in aggregate, expected to see their revenue grow 6.6% per year. It's pretty clear that Kumba Iron Ore's revenues are expected to perform substantially worse than the wider industry.

The Bottom Line

The clear low-light was that analysts slashing their revenue forecasts for Kumba Iron Ore this year. They're also anticipating slower revenue growth than the wider market. Given the stark change in sentiment, we'd understand if investors became more cautious on Kumba Iron Ore after today.

In light of the downgrade, our automated discounted cash flow valuation tool suggests that Kumba Iron Ore could now be moderately overvalued. Learn why, and examine the assumptions that underpin our valuation by visiting our free platform here to learn more about our valuation approach.

Another way to search for interesting companies that could be reaching an inflection point is to track whether management are buying or selling, with our free list of growing companies backed by insiders.

Valuation is complex, but we're here to simplify it.

Discover if Kumba Iron Ore might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About JSE:KIO

Kumba Iron Ore

Engages in the exploration, extraction, beneficiation, marketing, sale, and shipping of iron ore for the steel industry in South Africa.

Flawless balance sheet established dividend payer.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.6% undervalued

TI

Community Contributor

Recently Updated Narratives

BL

BlackGoat on Alphabet ·

Alphabet: The Under-appreciated Compounder Hiding in Plain Sight

Fair Value:US$324.481.3% undervalued

74 followersusers have followed this narrative

3 commentsusers have commented on this narrative

1 likeusers have liked this narrative

BE

Bejgal on MINISO Group Holding ·

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value:US$26.6926.7% undervalued

44 followersusers have followed this narrative

3 commentsusers have commented on this narrative

0 likesusers have liked this narrative

TI

TickerTickle on Oracle ·

The Quiet Giant That Became AI’s Power Grid

Fair Value:US$389.8147.4% undervalued

9 followersusers have followed this narrative

1 commentusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.9% undervalued

136 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

89 followersusers have followed this narrative

11 commentsusers have commented on this narrative

18 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$232.7922.6% undervalued

926 followersusers have followed this narrative

6 commentsusers have commented on this narrative

22 likesusers have liked this narrative