Advertisement

- United States

- /

- Renewable Energy

- /

- NYSE:VST

Vistra (VST): Revisiting Valuation After Earnings, Clean Energy Strategy, and Updated Growth Guidance

Simply Wall St

Reviewed by Simply Wall St

Vistra (VST) is in focus after reporting quarterly results showing lower net income and sales year-over-year, along with a minor asset impairment. However, the company highlighted long-term growth through strategic clean energy moves and raised its guidance.

See our latest analysis for Vistra.

Shares of Vistra have delivered a 19.7% year-to-date price return, with momentum rebounding after brief weakness in recent weeks. The company’s long-term outlook remains strong, as shown by a striking 684.7% total shareholder return over three years. This occurs despite the mixed reaction to its latest results and ongoing strategic expansion.

If you want to explore more opportunities beyond the utilities sector, now is a great time to discover fast growing stocks with high insider ownership

The real question for investors is whether Vistra’s robust future projections and recent strategic moves are already reflected in its share price, or if there is still room for upside as growth unfolds.

Most Popular Narrative: 21.5% Undervalued

Vistra’s most-followed narrative pegs fair value at $228.26, substantially above the latest close of $179.14. This suggests a notable disconnect between the current price and the anticipated future potential.

“Structural increases in electricity demand driven by AI, data centers, and U.S. manufacturing are expected to significantly boost the utilization of Vistra's generation assets. This supports sustained revenue and potential margin expansion as higher fixed cost absorption improves profitability.”

Curious how surging demand and expansion plans factor into this bullish outlook? The narrative leans on ambitious financial growth, future market leadership, and aggressive projections seldom seen in the sector. Uncover the assumptions powering this valuation and see if you spot the linchpin forecast hidden in the details.

Result: Fair Value of $228.26 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, risks such as political shifts in core markets or unexpected project delays could undermine the upbeat projections that are driving Vistra’s current valuation narrative.

Find out about the key risks to this Vistra narrative.

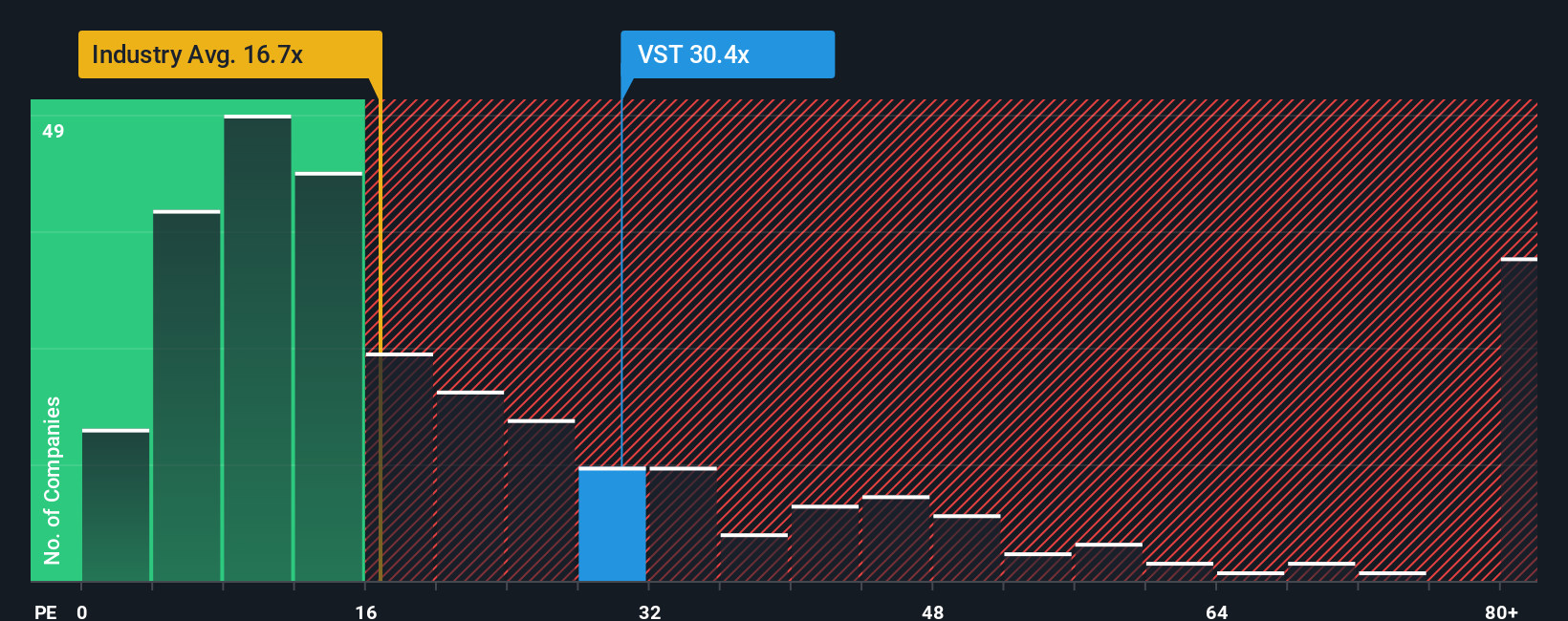

Another View: Market Multiples Send a Caution Signal

While our earlier discussion focused on Vistra's significant upside based on future growth potential, the market’s chosen yardstick, the standard price-to-earnings ratio, tells a more expensive story. Vistra trades at 63.2x earnings, far higher than both the industry’s 16.9x and peer average of 31x, and even above the fair ratio of 55.8x. Such a gap signals elevated valuation risk if market sentiment shifts or growth doesn't deliver as anticipated. Could this premium price reflect justified optimism, or is the room for error now uncomfortably narrow?

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own Vistra Narrative

If you see the story unfolding differently, or believe your own research leads in another direction, you can easily shape your perspective in just a few minutes: Do it your way

A great starting point for your Vistra research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

Looking for More Investment Ideas?

Shake up your watchlist and get ahead by targeting stocks tailored for today’s boldest trends. Miss this chance now and you might regret not acting sooner.

- Capture yield potential with companies delivering reliable income by checking out these 15 dividend stocks with yields > 3% with eye-catching yields above 3%.

- Jump on the AI transformation by exploring these 27 AI penny stocks that could benefit from the unstoppable momentum in artificial intelligence.

- Position yourself for long-term value by reviewing these 898 undervalued stocks based on cash flows based on robust cash flow analysis and proven financial health.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:VST

Vistra

Operates as an integrated retail electricity and power generation company in the United States.

Reasonable growth potential and slightly overvalued.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60.00|98.5% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|2.3% undervalued

TI

Community Contributor