Advertisement

- United States

- /

- Electric Utilities

- /

- NYSE:OGE

OGE Energy (OGE): Valuation Insights After Oklahoma Ruling on Construction Cost Recovery

Simply Wall St

Reviewed by Simply Wall St

The Oklahoma Corporation Commission’s recent decision on construction cost recovery has put OGE Energy’s capital planning in the spotlight. While the company received approval to build new gas units, upfront cost recovery was denied.

See our latest analysis for OGE Energy.

OGE Energy’s share price has held steady despite regulatory headwinds, with an 8.40% year-to-date gain and a solid 8.73% total shareholder return over the past year. Recent decisions around cost recovery have added a degree of uncertainty, but the company’s multi-year return of nearly 66% shows that long-term momentum remains in play for investors who can ride out short-term bumps.

If you’re looking to discover what else is possible beyond utilities, now is a great moment to broaden your watchlist and uncover fast growing stocks with high insider ownership.

With shares maintaining their gains despite regulatory noise, investors have to ask whether OGE Energy’s current valuation is overlooking fresh risks, or if the market has already reflected the company’s future growth in its stock price.

Most Popular Narrative: 5.9% Undervalued

OGE Energy’s last close of $44.76 sits roughly 6% below the narrative’s fair value of $47.55. This suggests some room for upside. This gap is built on several key catalysts the narrative sees driving higher revenue and profitability.

Sustained customer growth, electrification trends, and major projects are driving higher revenue and expanding opportunities, especially with data centers and large industrial clients. Strategic investments in infrastructure, favorable policies, and a strong financial position support stable earnings, improved margins, and long-term profitability.

What is fueling this optimistic price target? Tucked inside the forecast are growth assumptions and a margin outlook that hint at a future profit blueprint not seen in most utilities. Want to know which specific financial bets set the stage for this premium valuation? Click through and see what’s behind the narrative’s calculation.

Result: Fair Value of $47.55 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, continued weakness in key industrial segments and uncertainty around future regulatory changes could challenge the optimistic scenario that analysts now expect for OGE Energy.

Find out about the key risks to this OGE Energy narrative.

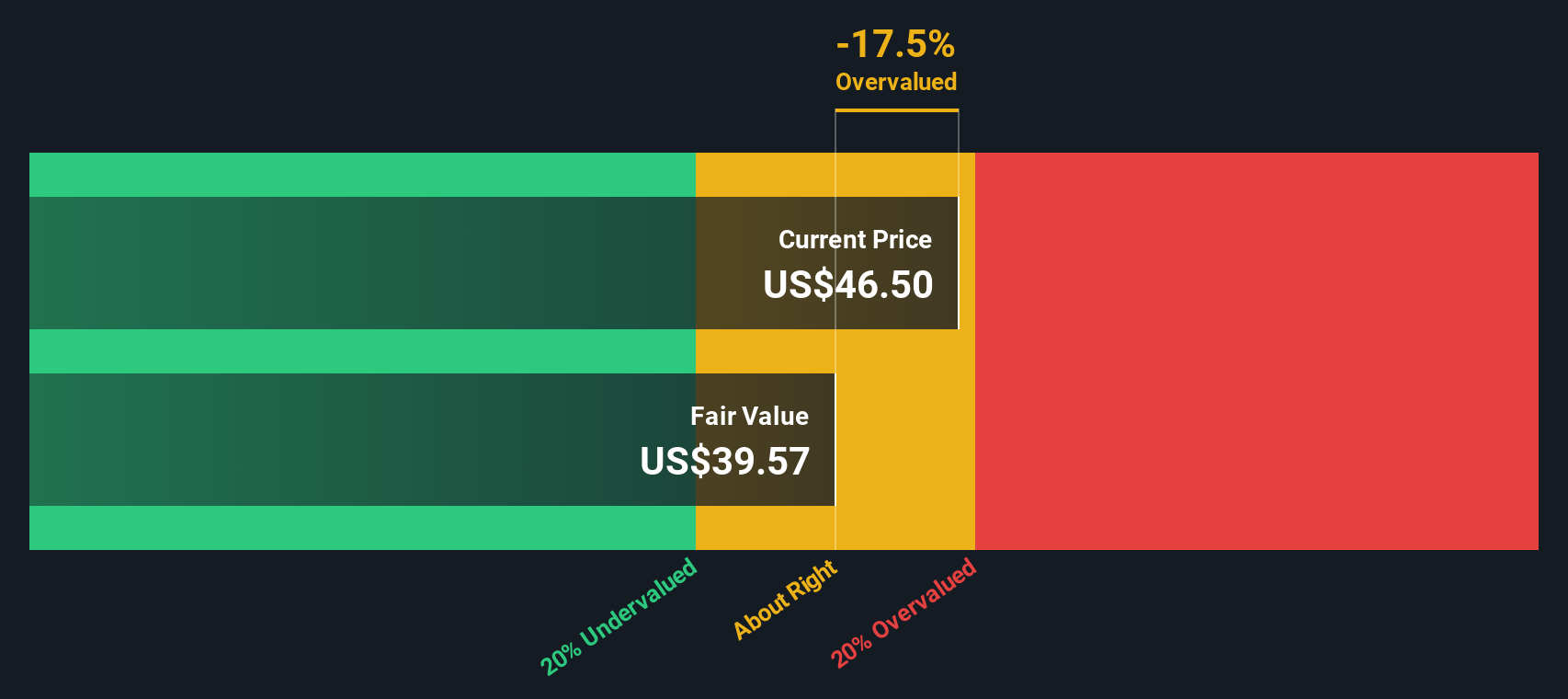

Another View: What Does Our SWS DCF Model Say?

Looking through the lens of our SWS DCF model, OGE Energy’s shares actually appear overvalued, trading above the estimated fair value of $37.51. This DCF outlook prompts investors to consider whether the current narrative is a little too optimistic, or if market confidence is simply ahead of the curve.

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out OGE Energy for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 878 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own OGE Energy Narrative

If this perspective doesn’t match your view or you’d like to dig into the details yourself, you can craft your own take on OGE Energy in just a few minutes. Do it your way.

A great starting point for your OGE Energy research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

Looking for more investment ideas?

Ready to seize new opportunities? Supercharge your watchlist by checking out standout stocks and breakthrough sectors thoughtfully curated with the Simply Wall Street Screener.

- Unlock value and spot strong cash flow opportunities by checking out these 878 undervalued stocks based on cash flows which consistently meet tough financial benchmarks.

- Tap into robust yields by scanning these 16 dividend stocks with yields > 3% that offer over 3% returns and stable income potential for your portfolio.

- Capture the momentum of the AI revolution as you review these 24 AI penny stocks leading the next wave of intelligent technology growth.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:OGE

OGE Energy

Through its subsidiary, operates as an energy services provider in the United States.

Solid track record average dividend payer.

Similar Companies

Market Insights

Advertisement

Community Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|11.0% undervalued

BE

Community Contributor

Procter & Gamble: A Dividend Giant Facing Slowing Growth

Fair Value US$119.81|23.3% overvalued

AN

Community Contributor

Eli Lilly's Future Growth Driven by Tirzepatide and Favorable Market Conditions

Fair Value US$1.19k|13.8% undervalued

EA

Community Contributor