Advertisement

- United States

- /

- Electric Utilities

- /

- NYSE:NRG

Are NRG Energy, Inc.’s (NYSE:NRG) High Returns Really That Great?

Want to participate in a short research study? Help shape the future of investing tools and you could win a $250 gift card!

Today we are going to look at NRG Energy, Inc. (NYSE:NRG) to see whether it might be an attractive investment prospect. To be precise, we'll consider its Return On Capital Employed (ROCE), as that will inform our view of the quality of the business.

Firstly, we'll go over how we calculate ROCE. Next, we'll compare it to others in its industry. Last but not least, we'll look at what impact its current liabilities have on its ROCE.

Return On Capital Employed (ROCE): What is it?

ROCE measures the amount of pre-tax profits a company can generate from the capital employed in its business. In general, businesses with a higher ROCE are usually better quality. In brief, it is a useful tool, but it is not without drawbacks. Author Edwin Whiting says to be careful when comparing the ROCE of different businesses, since 'No two businesses are exactly alike.'

How Do You Calculate Return On Capital Employed?

The formula for calculating the return on capital employed is:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

Or for NRG Energy:

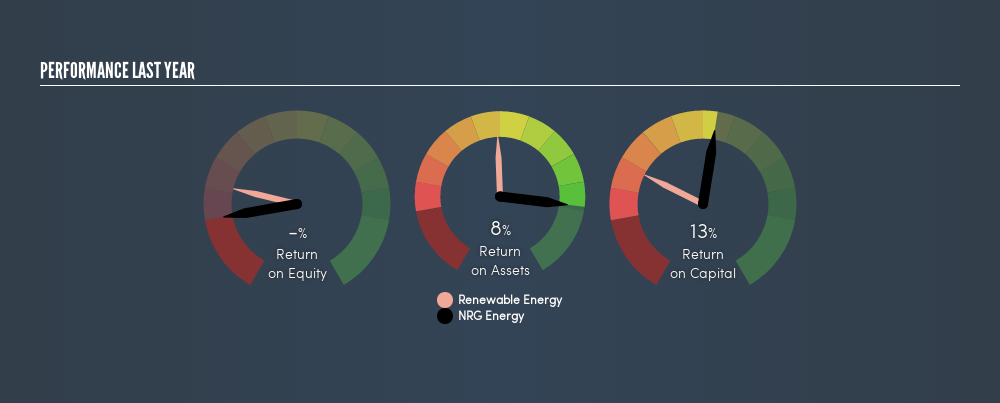

0.13 = US$993m ÷ (US$9.5b - US$1.9b) (Based on the trailing twelve months to March 2019.)

So, NRG Energy has an ROCE of 13%.

View our latest analysis for NRG Energy

Is NRG Energy's ROCE Good?

ROCE can be useful when making comparisons, such as between similar companies. In our analysis, NRG Energy's ROCE is meaningfully higher than the 5.8% average in the Renewable Energy industry. We consider this a positive sign, because it suggests it uses capital more efficiently than similar companies. Independently of how NRG Energy compares to its industry, its ROCE in absolute terms appears decent, and the company may be worthy of closer investigation.

As we can see, NRG Energy currently has an ROCE of 13% compared to its ROCE 3 years ago, which was 4.4%. This makes us think about whether the company has been reinvesting shrewdly.

When considering this metric, keep in mind that it is backwards looking, and not necessarily predictive. ROCE can be misleading for companies in cyclical industries, with returns looking impressive during the boom times, but very weak during the busts. ROCE is, after all, simply a snap shot of a single year. Since the future is so important for investors, you should check out our free report on analyst forecasts for NRG Energy.

What Are Current Liabilities, And How Do They Affect NRG Energy's ROCE?

Short term (or current) liabilities, are things like supplier invoices, overdrafts, or tax bills that need to be paid within 12 months. The ROCE equation subtracts current liabilities from capital employed, so a company with a lot of current liabilities appears to have less capital employed, and a higher ROCE than otherwise. To check the impact of this, we calculate if a company has high current liabilities relative to its total assets.

NRG Energy has total assets of US$9.5b and current liabilities of US$1.9b. Therefore its current liabilities are equivalent to approximately 20% of its total assets. Current liabilities are minimal, limiting the impact on ROCE.

The Bottom Line On NRG Energy's ROCE

This is good to see, and with a sound ROCE, NRG Energy could be worth a closer look. There might be better investments than NRG Energy out there, but you will have to work hard to find them . These promising businesses with rapidly growing earnings might be right up your alley.

For those who like to find winning investments this free list of growing companies with recent insider purchasing, could be just the ticket.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.

About NYSE:NRG

NRG Energy

Operates as an energy and home services company in the United States and Canada.

Adequate balance sheet average dividend payer.

Similar Companies

Market Insights

Advertisement

Community Narratives

The Future of Drug Testing? Fingerprint Tech Shows Serious Promise

Fair Value US$2.98|40.3% undervalued

JO

Community Contributor

Suncorp’s Next Chapter: Insurance-Only and Ready to Grow

Fair Value AU$22.83|7.6% undervalued

RO

Community Contributor

Thyssenkrupp Nucera Will Achieve Double-Digit Profits by 2030 Boosted by Hydrogen Growth

Fair Value €14.40|30.6% undervalued

CH

Community Contributor

Tesla’s Nvidia Moment – The AI & Robotics Inflection Point

Fair Value US$359.72|12.3% undervalued

BL

Community Contributor