- United States

- /

- Electric Utilities

- /

- NYSE:NEE

NextEra Energy (NYSE:NEE) Issues US$875 Million Series U Debentures Maturing in 2085

Reviewed by Simply Wall St

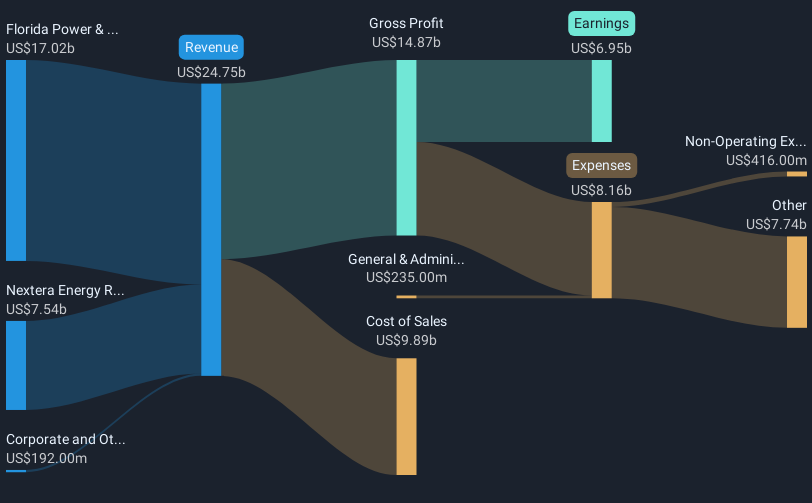

NextEra Energy (NYSE:NEE) recently issued Series U Junior Subordinated Debentures worth $875 million, bolstering its financial position with a long-term maturity and a favorable interest rate. This capital raise aligns with broader market trends, as the S&P 500 is extending its winning streak. Although the company's net income decline contrasts with broader market gains, its recent capital strategies could have stabilized its position amidst the positive market sentiment, contributing to its 10% price increase last month. Despite no recent dividend announcements or share repurchases, the issuance provided a significant financial buffer amidst the evolving economic landscape.

NextEra Energy has 2 weaknesses (and 1 which is a bit unpleasant) we think you should know about.

The recent issuance of Series U Junior Subordinated Debentures has injected significant financial resilience into NextEra Energy, which could influence its trajectory against the backdrop of broader global decarbonization goals and U.S. electrification trends. The fresh capital may bolster NextEra's ability to pursue renewable projects, aligning with its strengths in scale and cost efficiency. This might not only enhance revenue growth prospects but also contribute to improved margins as more electricity generation projects come online.

Over the past five years, NextEra Energy's total shareholder return, inclusive of share price appreciation and dividends, stands at 46.96%. This long-term performance demonstrates robust growth, particularly in fast-evolving energy sectors. However, in the past year, the company's performance was not as favorable, underperforming the U.S. Electric Utilities industry, which grew by 11.8%.

In terms of revenue and earnings forecasts, the new capital raise could provide additional flexibility for investments, potentially accelerating growth beyond current projections. As the company continues to focus on renewable infrastructure, these strategic investments might drive its revenue and earnings trajectory equally or beyond consensus expectations.

NextEra's recent share price of $66.54 reflects a moderate discount to the consensus analyst price target of $81.86, with more bullish projections reaching up to $103. Despite short-term underperformance relative to the market, the company's ability to leverage fresh capital for strategic growth initiatives could support a future valuation re-rating as it captures emerging electrification opportunities.

Explore NextEra Energy's analyst forecasts in our growth report.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if NextEra Energy might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:NEE

NextEra Energy

Through its subsidiaries, generates, transmits, distributes, and sells electric power to retail and wholesale customers in North America.

Average dividend payer with questionable track record.

Similar Companies

Market Insights

Community Narratives