Advertisement

- United States

- /

- Electric Utilities

- /

- NYSE:ES

Eversource Energy (NYSE:ES) Might Be Having Difficulty Using Its Capital Effectively

There are a few key trends to look for if we want to identify the next multi-bagger. One common approach is to try and find a company with returns on capital employed (ROCE) that are increasing, in conjunction with a growing amount of capital employed. Ultimately, this demonstrates that it's a business that is reinvesting profits at increasing rates of return. In light of that, when we looked at Eversource Energy (NYSE:ES) and its ROCE trend, we weren't exactly thrilled.

Understanding Return On Capital Employed (ROCE)

For those that aren't sure what ROCE is, it measures the amount of pre-tax profits a company can generate from the capital employed in its business. To calculate this metric for Eversource Energy, this is the formula:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

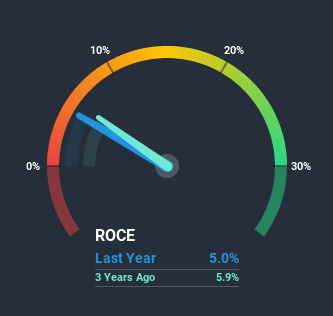

0.05 = US$2.0b ÷ (US$46b - US$4.9b) (Based on the trailing twelve months to December 2020).

So, Eversource Energy has an ROCE of 5.0%. In absolute terms, that's a low return but it's around the Electric Utilities industry average of 4.5%.

See our latest analysis for Eversource Energy

In the above chart we have measured Eversource Energy's prior ROCE against its prior performance, but the future is arguably more important. If you'd like, you can check out the forecasts from the analysts covering Eversource Energy here for free.

How Are Returns Trending?

We weren't thrilled with the trend because Eversource Energy's ROCE has reduced by 22% over the last five years, while the business employed 49% more capital. However, some of the increase in capital employed could be attributed to the recent capital raising that's been completed prior to their latest reporting period, so keep that in mind when looking at the ROCE decrease. Eversource Energy probably hasn't received a full year of earnings yet from the new funds it raised, so these figures should be taken with a grain of salt. Also, we found that by looking at the company's latest EBIT, the figure is within 10% of the previous year's EBIT so you can basically assign the ROCE drop primarily to that capital raise.

The Key Takeaway

In summary, Eversource Energy is reinvesting funds back into the business for growth but unfortunately it looks like sales haven't increased much just yet. Since the stock has gained an impressive 76% over the last five years, investors must think there's better things to come. Ultimately, if the underlying trends persist, we wouldn't hold our breath on it being a multi-bagger going forward.

On a final note, we found 2 warning signs for Eversource Energy (1 is a bit concerning) you should be aware of.

If you want to search for solid companies with great earnings, check out this free list of companies with good balance sheets and impressive returns on equity.

If you decide to trade Eversource Energy, use the lowest-cost* platform that is rated #1 Overall by Barron’s, Interactive Brokers. Trade stocks, options, futures, forex, bonds and funds on 135 markets, all from a single integrated account. Promoted

Valuation is complex, but we're here to simplify it.

Discover if Eversource Energy might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About NYSE:ES

Eversource Energy

A public utility holding company, engages in the energy delivery business.

Undervalued established dividend payer.

Similar Companies

Market Insights

Advertisement

Weekly Picks

DA

davidlsander on Ubisoft Entertainment ·

Is Ubisoft the Market’s Biggest Pricing Error? Why Forensic Value Points to €33 Per Share

Fair Value:€33.888.1% undervalued

52 followersusers have followed this narrative

3 commentsusers have commented on this narrative

23 likesusers have liked this narrative

TO

Tokyo on LVMH Moët Hennessy - Louis Vuitton Société Européenne ·

EU#4 - Turning Heritage into the World’s Strongest Luxury Empire

Fair Value:€750.0428.5% undervalued

5 followersusers have followed this narrative

1 commentusers have commented on this narrative

9 likesusers have liked this narrative

WE

WealthAP on Alphabet ·

The "Easy Money" Is Gone: Why Alphabet Is Now a "Show Me" Story

Fair Value:US$386.4316.5% undervalued

66 followersusers have followed this narrative

1 commentusers have commented on this narrative

20 likesusers have liked this narrative

Recently Updated Narratives

PI

PittTheYounger on Delta Air Lines ·

Delta loses shine after warning of falling travel demand, but still industry leader

Fair Value:US$63.2119.2% overvalued

17 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

RA

Ravedigga on Defence Holdings ·

Project Ixian Accelerated Rollout will Drive Valuation Expansion to £0.0150.

Fair Value:UK£0.0156.7% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

TO

Tokyo on Siemens ·

EU#5 - From Industrial Giant to the Digital Operating System of the Real World

Fair Value:€319.521.6% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

OO

OOO97 on Neo Performance Materials ·

Undervalued Key Player in Magnets/Rare Earth

Fair Value:CA$25.3322.3% undervalued

76 followersusers have followed this narrative

0 commentsusers have commented on this narrative

19 likesusers have liked this narrative

DA

davidlsander on Ubisoft Entertainment ·

Is Ubisoft the Market’s Biggest Pricing Error? Why Forensic Value Points to €33 Per Share

Fair Value:€33.888.1% undervalued

52 followersusers have followed this narrative

3 commentsusers have commented on this narrative

23 likesusers have liked this narrative

BL

BlackJesus on Adobe ·

The Strategic Revaluation of Adobe: A Critical Analysis of Market Sentiment

Fair Value:US$46041.7% undervalued

34 followersusers have followed this narrative

2 commentsusers have commented on this narrative

22 likesusers have liked this narrative

Trending Discussion

KA

Kalibrator on Ubisoft Entertainment ·

As a gamer, I would not touch this company now. They are hated by the community and have been releasing major flops on their AAA games during the last 5 years (for good reasons). It is true that the valuation is ridiculously low compared to what the licenses are worth, but if the trend continues the value of those will also decline. Management needs to almost make a 180° turnaround to get things right. I agree that a take-private deal before it is too late might be the best option for an investor entering today. We might also see a split sales of the different studios. It is a very risky play, but potentially with high reward.

1

|0