ALLETE (ALE) shares have quietly moved higher in the past month, with the stock gaining 6% and returning nearly 10% over the past year. Investors seem to be weighing stable utility performance in comparison to broader market dynamics as they evaluate the company's outlook.

ALLETE’s recent momentum builds on a solid stretch, with a 6% share price return over the past month adding to a steady gain for shareholders. The company’s 1-year total shareholder return is just under 10%, while its three- and five-year returns have been even more robust. This points to a business that has rewarded patient investors as market sentiment grows more positive.

But with ALLETE’s recent gains and another year of positive returns, is the share price still a bargain for value-seeking investors? Or has the market already factored in the company’s future growth potential?

Advertisement

Price-to-Earnings of 21.3x: Is it justified?

ALLETE is currently valued at a price-to-earnings (P/E) ratio of 21.3x, matching the US Electric Utilities industry average. However, compared to peers and its estimated 'fair' multiple, investors might question if the current level is sustainable.

The price-to-earnings ratio measures how much investors are willing to pay for each dollar of annual earnings. For utilities, the P/E can reflect expectations about stability and growth. Comparative P/E analysis is vital to avoid overpaying for slow-growth sectors.

At 21.3x, ALLETE trades right in line with the rest of the industry. This suggests the market sees its prospects as average within the sector. Its ratio also closely matches the estimated fair price-to-earnings ratio of 21.8x, indicating there may be little room for further upside unless growth outperforms expectations. This 'fair' level is a data-driven benchmark for where the market could possibly re-rate the stock.

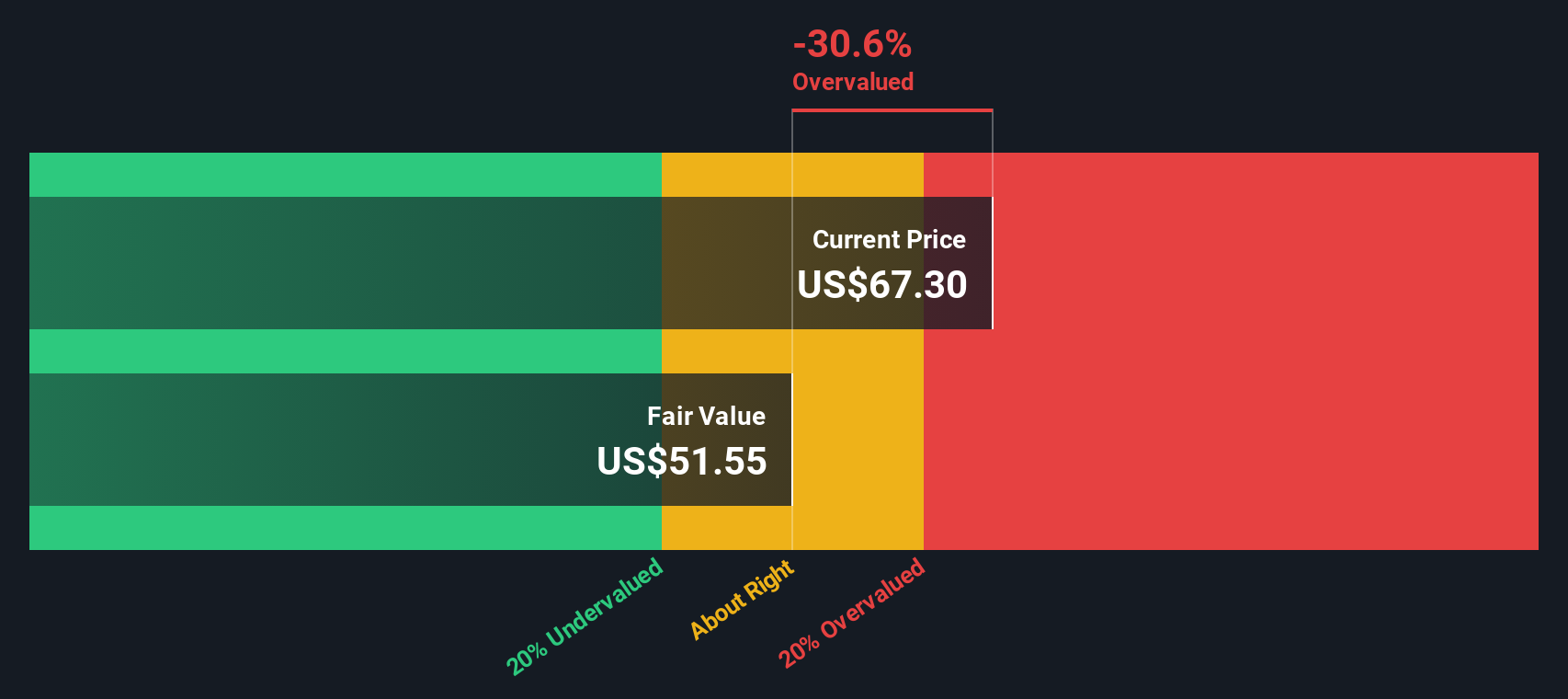

While traditional valuation compares ALLETE’s share price to earnings, our SWS DCF model looks at the company’s future cash flows to estimate true worth. On this basis, ALLETE’s current price of $67.37 sits well above our fair value estimate of $51.55, suggesting it may be overvalued. Could this be a caution flag, or does the market know something the model does not?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out ALLETE for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own ALLETE Narrative

Keep in mind, you can always dig into the numbers yourself and pull together your own perspective on ALLETE’s future in just minutes. Do it your way

Stay on the frontier of technology as you browse these 26 quantum computing stocks and explore companies transforming industries through quantum computing breakthroughs.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency • Be alerted to new Warning Signs or Risks via email or mobile • Track the Fair Value of your stocks