AES (AES) shares have seen subtle movement lately, with the energy company drawing attention from investors reviewing current performance trends. Over the past month, AES stock has advanced by 9%, providing a fresh angle for those tracking utility sector shifts.

After a somewhat challenging year, AES has recently picked up momentum with an 8.9% 1-month share price return and a year-to-date gain of 11.5%. Even so, total shareholder return remains negative over the past 12 months. This reflects the impact of broader market uncertainties as well as company-specific developments. The recent share price climb hints that the market may be warming to AES’s outlook. This suggests investors are re-evaluating its long-term value and risk profile.

With recent gains and a modest uptick in fundamentals, the key question now is whether AES stock is undervalued at current levels or if investors have already factored in the company’s outlook, which could leave limited room for upside.

Advertisement

Most Popular Narrative: 0.6% Overvalued

AES’s current share price sits slightly above what the most-followed narrative considers fair, creating a tight valuation gap that demands a closer look at the details behind this call.

AES's leading, long-term pipeline of renewables and energy storage projects, backed by robust, multi-year Power Purchase Agreements (PPAs) with data center and corporate customers, positions the company to capitalize on rapidly rising electricity demand from AI/data centers. This supports accelerating revenue growth and increasing visibility on future cash flows.

What’s really fueling that price target? Behind the scenes: aggressive earnings projections, margin trends, and a future profit multiple that diverges from industry averages. The narrative’s math depends on factors the market may not be expecting. Break down the full argument and see which growth assumptions are creating this slim valuation cushion.

However, ongoing reliance on government incentives, along with the possibility of supply chain disruptions, could quickly challenge the case for steady profit growth.

Another View: Discounted Cash Flow Paints a Different Picture

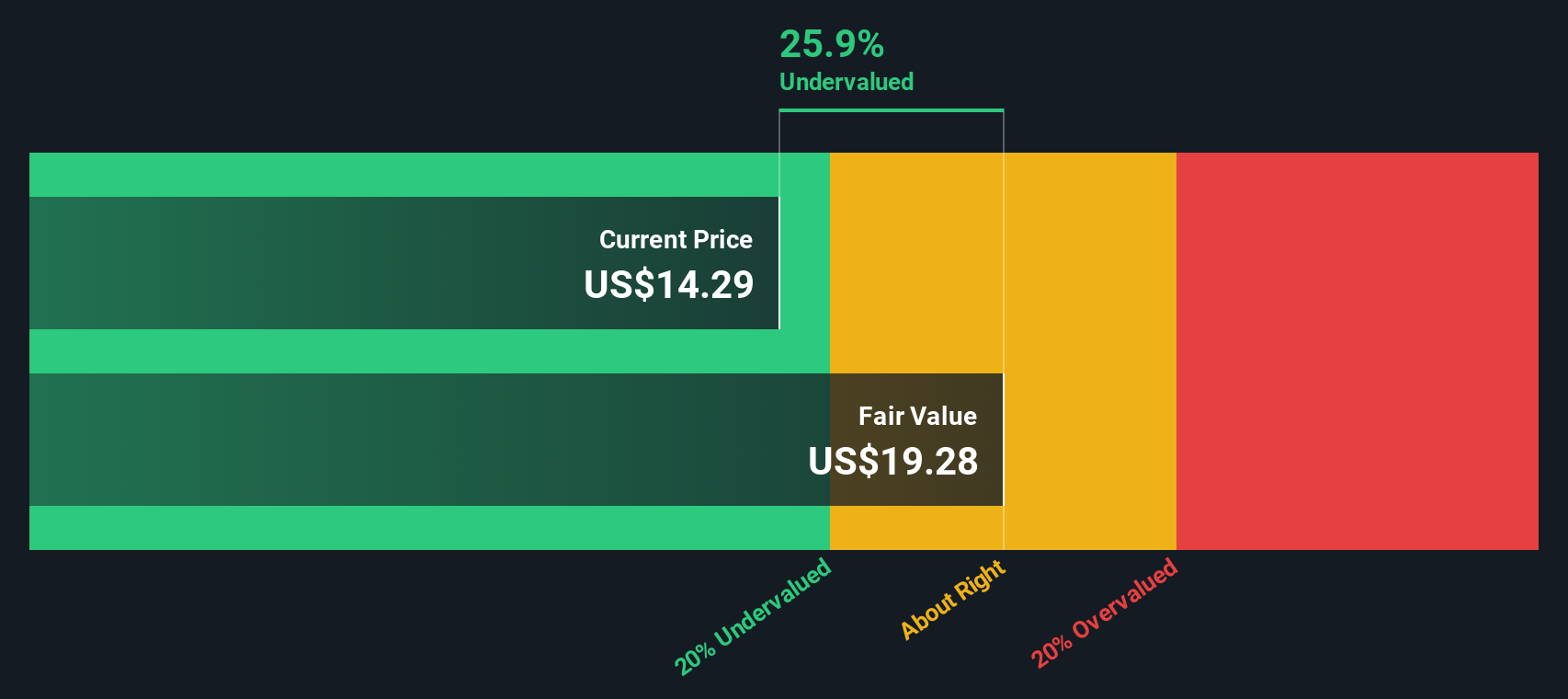

While the consensus price target approach suggests AES is trading near fair value, our DCF model points to a different conclusion. The SWS DCF analysis calculates AES’s fair value at $19.28, around 24.5% above the current share price. This hints the stock may be meaningfully undervalued. Which model should guide your next move?

Smart investors don’t stop at just one stock. Expand your horizons with handpicked opportunities and let your money work harder with ideas others might overlook.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency • Be alerted to new Warning Signs or Risks via email or mobile • Track the Fair Value of your stocks